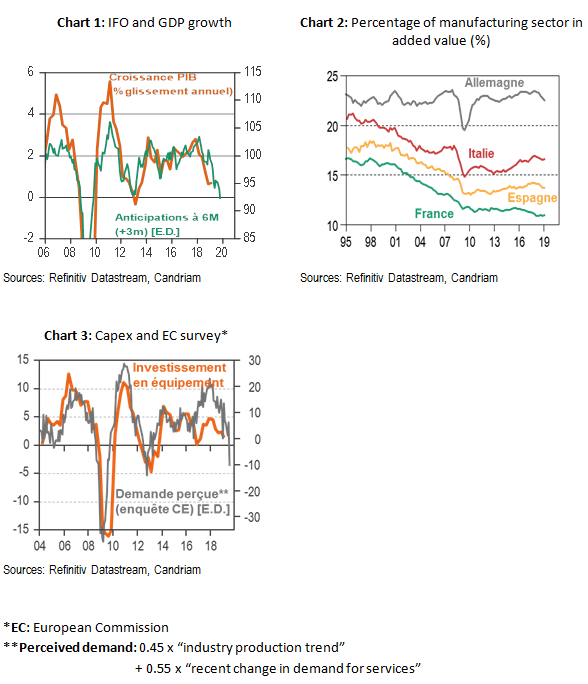

Although a number of exceptional factors weighed on the manufacturing sector in H2 2018, many observers had hoped to see activity pick up again in spring 2019. Unfortunately, it was not to be (chart 1). The slowdown in global trade, from China in particular, and recently the UK’s pre-Brexit spending spree (initial Brexit date: 29 March) further slowed German exports and consequently German industry. The Manufacturing PMI has thus fallen from 56.9 to 43.2 in just one year. Furthermore, due to low rainfall and the recent heat wave, traffic on the Rhine is under threat again, which is liable to affect the chemicals sector in the third quarter. Given the manufacturing sector’s substantial weight in the German economy (chart 2), further contraction of industrial output can only exacerbate the slowdown in GDP growth. The risk is that we may see business investment come to a halt (recent indicators have actually pointed to a troubling drop in perceived demand by corporates - chart 3). Meanwhile, despite a persistently low unemployment rate, German consumer sentiment is waning.

For the time being, economic stagnation is more likely than a recession. The wage mass increase provides strong support for consumption. From a more general standpoint, growth is still on a good track in the services sector, with the PMI at 54.5 in July. Even so, German growth is in peril, and a more expansionist fiscal policy would be very welcome indeed. This was the message sent loud and clear by the bond market: with the 10-year under -0.5% and the 30-year at zero, it’s time for Germany to use the leeway at its disposal to fund greener - but also more inclusive - growth!