The situation is very different among the different regions in the world. Even if activity is resuming in China (but with quarantine at the borders), other Asian countries such as Japan and even South Korea seem to be encountering new difficulties. In Europe, where the peak of the pandemic is around these weeks, the exit strategy is currently being discussed. In the US, the diagnostic is more complex, with each individual state responsible for its own confinement measures. The big debate concerns how long it will take to see the peak. Central banks and governments have been very proactive in giving guarantees, but time will be against growth perspectives if the confinement lasts too long. A positive shock would be the discovery of any antiviral therapy.

Equities vs. bonds

Financial markets are currently assessing the duration of the economic freeze that the confinement implies. Hope is beginning to emerge in China, Austria and Italy, with the authorities inclined to let people start to act more freely, notably to go to work. But no one knows how long it will take for the world economy to recover its entire capacity. Some emerging countries, and even the US, are currently in the eye of the storm, so it is difficult to really measure the economic and social impacts of this pandemic. The longer the situation persists, the higher the costs will be. One ray of hope is coming from the proactivity with which central banks have addressed the economic situation. –far faster than in 2008. Some problems remain, notably on short-term funding, but the financial authorities are well aware of the risks. The governments were very quick, too, to adopt measures to help individuals and companies to get through this situation. However, it is true that, to make money available for economic actors, it is, in general, taking more time than initially thought. Moreover, it seems that, in Europe, for instance, it will be necessary to add more stimuli and to find a higher level of coordination and solidarity to recover more rapidly from this crisis. A possible agreement on oil production cuts would also be positive in this context. It has already been partly anticipated in the oil price rebound. The oil price war was one of the factors to have worsened the investment climate and increased the risk on the credit side.

In a medium-term perspective, volatility is here to stay. We have increased our equity exposure gradually in recent weeks, but refrain from adding to current levels. Patience remains the key word, since we will not directly have a “V”-shape recovery. We remain ready to act more positively if these uncertainties begin to evaporate.

From a long-term perspective, equity markets still offer value and represent upside potential. Ultimately, strong central bank and government policy responses will outlast the virus.

Equities

US, Europe and Japan

On the assumption that:

- the coronavirus is a temporary shock,

- the peak of the epidemic is behind us in China, and that

- the peak of the epidemic is ahead of us, in Q2, in the US, Europe and Japan,

we have revised down our economic scenarios for the coming two years.

The monetary and fiscal policy responses initiated by central banks and governments to mitigate the financial short-term risk will hopefully be coordinated and adequate. Some risks have already made the headlines. They are being closely monitored.

In the US, the Fed continues to be highly creative, adopting a series of measures to alleviate the US Dollar shortages around the world, including the setting-up of swap lines with not only developed-country but also emerging-country central banks . The many new instruments introduced have facilitated companies’ access to credit and improved market conditions.

In Germany, Chancellor Merkel has already stated that the government will spend any amount necessary to contain the virus in Germany. Italy, meanwhile, is preparing another fiscal plan that will double the current stimulus. However, in Europe, there is no widespread consensus on a framework for these rescue plans.

In Japan, the government announced an emergency stimulus package of nearly 20% of GDP designed to address corporate and household woes. It will notably defer social security and tax payments, and provide cash payments for households and small and medium-sized companies. The country’s economy is suffering from an important decline in tourism and Japan will now not host the Summer Olympic Games until 2021.

Our asset allocation has been impacted by the processing of new forecasts on

- economic growth,

- (and therefore, to some extent, also) earnings (approx. 50% of earnings growth can be explained by GDP growth), and

- calculations of expected returns.

Price earnings have increased since last month and are now closer to their historical medians. The equity risk premium is increasing – more so in the US than in the euro zone.

The lockdown in China and some European countries is, or will be, loosened. An exit strategy is now been discussed in some countries. Economic and financial measures are supporting equity markets. However, there is still a lack of visibility on the epidemic outbreak in the US and the funding of fiscal measures in Europe.

We are slightly underweight equities, Europe ex-EMU and the US, and neutral on the other regions.

Emerging markets: China

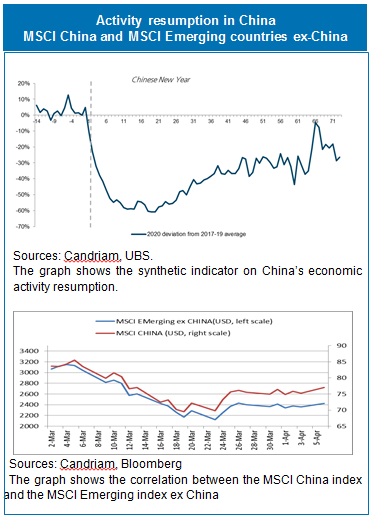

The MSCI China took a different path to Chinese recovery activity in March. Like the other equity indexes (SPX, MSCI emerging ex-China), it went down until March 23rd and then – just like the others – recovered.

For sure, the path to activity resumption in China is being closely monitored. And those indicators, which include the daily coal consumption and daily transport-related data –proxies for the availability of labour, transportation and materials, i.e. capacity utilisation – are growing. But, at the same time, Covid-19 is more present in other emerging countries outside South America.

We are currently neutral Emerging market equities.

Bonds and hedges

Beyond equities, bond yields are far less volatile than before March 10th. Sovereign bond yields are being kept under pressure by central bank decisions. The credit market has stabilized somewhat, notably the investment grade component. The oil price recovery, too, has helped. We will monitor any new central bank initiative that could alleviate the burden on the corporate bonds markets.

Looking forward, the sharp decrease in yields implies that this “natural” hedge in a balanced portfolio will be less effective.

We are therefore diversifying our hedges into other asset classes, such as gold and the Japanese Yen. We are neutral on the EURUSD cross in a diversified fund.

We are monitoring the emerging market debt asset class, which is vulnerable to a credit and liquidity crunch in the current situation. Events of the next few months will depend on the evolution of several variables, including financial market and central bank actions. We are therefore adopting a cautious yet opportunistic stance on the asset class.