Over the past year, our in-house models have been indicating a downturn in the activity cycle across every country in the G10 region, pointing in some cases towards a recession. Clearly, this prediction is now reality, though the pace – accelerated by the contagion of the coronavirus over the entire month of March – has been extremely abrupt. Indeed, what was specifically a “Chinese” and South-East Asia issue to begin with has landed in all developed countries, with Europe feeling the full impact and the US turning into the epicentre of the virus. It has led to partial or complete shutdowns in most countries, thereby exacerbating the activity slowdown and very likely paving the way to a global recession. Alongside this unfortunate turn of events, oil prices experienced a sharp decline (from $60 to $20 per barrel for the WTI) on the back of disagreements over supply cuts within the OPEC+ members, mainly between Russia and Saudi Arabia (which are key members). This, unfortunately, put additional pressure on high yield and emerging markets, which include substantial oil-producing companies and oil-exporting countries.

Market reaction was as expected, with risk assets posting double-digit negative returns, as both spreads and yields reached multi-year highs in credit and emerging debt markets. Policy reaction was extremely significant (and synchronized, though uncoordinated) as both fiscal and monetary support emerged from nearly all major countries, reaching at times historic magnitudes. Noteworthy was the Federal Reserve’s decision to not only take rates to 0%, but also open the door to the purchase of corporate bonds, ETFs and even fallen angels. The ECB added EUR 750 billion in purchases, and could end up owning 40% of the eligible market, while also signalling that Greek bonds were now eligible for their QE programmes. For a market that has been claiming time and again that central banks were running out of ammunition and that they were unable to do more, this was indeed considered a surprise and a rally was witnessed in the first half of April. As to how sustainable this short-term performance is, that would really depend on how the virus is being contained and progress made in terms of de-confinement. Indeed, what separates the current crisis from previous crises (namely 2008 and 2002) is that, in the past, fiscal and monetary packages were meant to push the population to go out and consume in order to “jump-start” the economy. In the present case, however, consumers are being asked to stay at home, and businesses have suspended activities and are unlikely to bounce back in such conditions. This also adds a bit of a ripple in terms of valuations, which have now turned quite interesting on risk assets and even, in many cases, attractive. Indeed, dispersion and dislocations appear to have emerged in many of the segments that have suffered indiscriminately and with, at times, a lesser fundamental basis. However, in spite of these levels of yields and spreads, one has to recognize that, in such an unprecedented situation, relative attractiveness is difficult to assess, especially when we consider that calling a bottom depends on the evolution of the contagion.

Positive stance on US rates, Neutral on European Rates

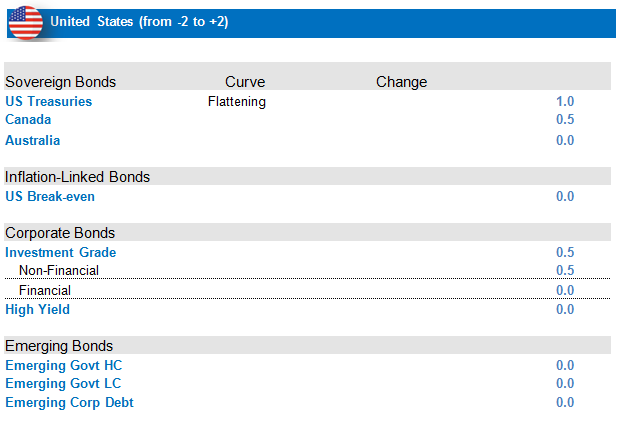

With the coronavirus wreaking havoc on global markets, US rates are the main beneficiaries, thanks to their safe-haven status. While rates are at historic lows, the strong intervention of the Federal Reserve, which includes $500 billion in US Treasury purchases, should put a firm ceiling on any uptick in yields. Furthermore, the extremely weak activity cycle, the soon-to-be record levels of unemployment and very low inflation all point to the potential for a decline in yields.

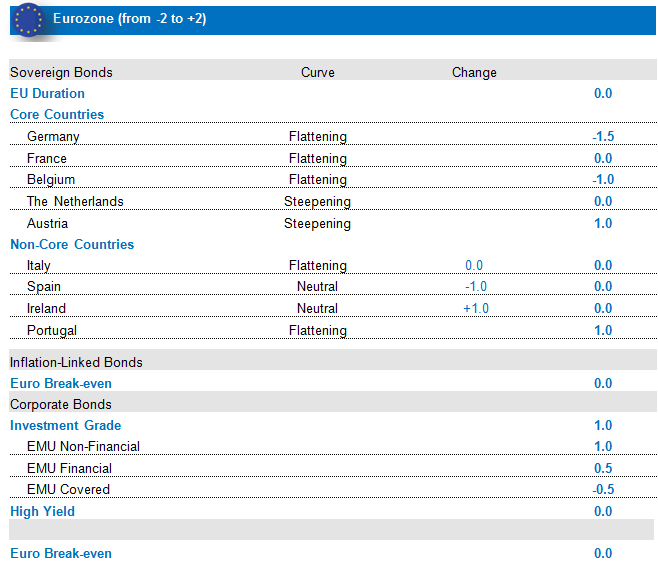

European non-core markets have continued to receive support from the ECB’s quantitative easing in recent months – support that sky-rocketed in amplitude in March. Indeed, the ECB at first announced an increase of its APP by €120bn. at its March meeting and, a week later, announced the deployment of its PEPP (Pandemic Emergency Purchase Programme), which includes an increase of EUR 750 billion in sovereign and corporate bond buying, which now includes Greek sovereigns. In spite of a possible increase in issuance, net supply should be negative as a result of this purchase programme, which is a source of support for yields in the short term. We continue to selectively favour Portugal among peripheral sovereigns while we have increased exposure to Ireland. Overall, we still feel that valuations on Euro sovereign rates remain relatively expensive and we aim to keep a neutral duration, which we do by holding a negative duration to German rates, favouring Austria and Luxemburg among core markets.

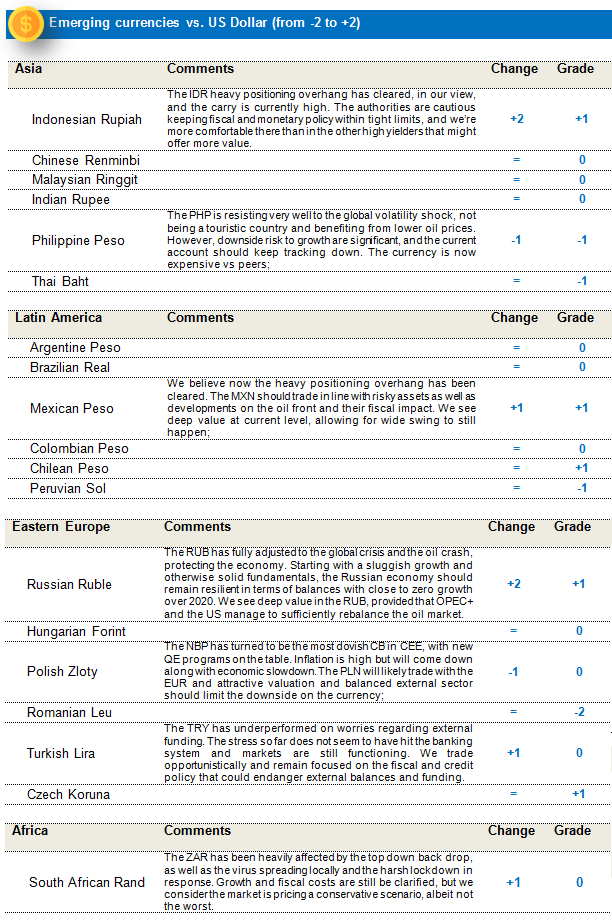

Developed Market Currencies: Neutral USD

Our proprietary framework continues to point towards a negative view on the US dollar. The Fed’s rate cuts, QE programme and dovish stance also point towards a weaker dollar. The dollar, however, does appear to have regained its safe-haven status following the mid-March rally (amidst a dash for cash by investors seeking shelter from the fallout of the coronavirus), after it suffered considerably during the early portion of the sell-off. In this context, we prefer to have a neutral position on the US Dollar and we continue to tactically manage the position.

Credit: Favourable View on Investment Grade, Neutral on High Yield

Although we are maintaining our favourable view on the European credit investment grade asset class, we continue to closely monitor idiosyncratic risks and exercise a high level of selectivity. Over the past month, European IG valuations have turned relatively attractive as yields practically tripled to 1.5% while spreads – at over 200 bps – are now at 2012 levels. The ECB’s strong QE programme has led the Bank to own 20% of the eligible IG universe, and, by year-end, it could own close to 40% of the eligible universe. With such an important backstop, technicals are receiving strong support. Based on these spread levels, default rates are estimated at approximately 4% – deemed excessive, as historical default rates on 5 years for the asset class have been at 0.9%. Furthermore, dislocations are present in the investment universe in terms of the maturity spectrum, as the variations in spreads show that the short-term EUR IG credit segment has seen more relative spread-widening than the longer term, though the shorter term is deemed safer.

However, we are paying special attention to the risk of downgrades (and fallen angels), which we feel are quite high on IG markets. We believe that not only has EUR IG credit suffered irrationally and indiscriminately as a result of the contagion of the virus, but that this is also due to the fact that investors have sold the higher-quality and safer assets in order to shore up liquidity. In this context, it is important to exercise selectivity and focus on defensive sectors (telcos, retailers) while maintaining caution towards cyclicals (Energy, Automobiles).

We apply this selectivity across all credit markets, though we are maintaining an overall neutral stance on European high yield, which is not directly benefiting from the central bank purchase programme. Furthermore, the oil price declines are weighing on more of the HY segment. We expect the drift to be negative, as downgrades will outpace upgrades (as they do in times of recession) and default will rise significantly to around 10% in the US. In this context, and despite favourable valuations (yields above 7%), we prefer to hold a neutral view on the asset class

Emerging Markets: Markets hit by headwinds of coronavirus global outbreak and the launch of an oil-price war.

In the medium term, we are retaining a constructive stance on EMD HC sovereigns and corporates and a more constructive stance on EM rates as we find pockets of value across EMD IG and HY sovereign and corporate segments. We are less constructive on EM currencies, as these are growth-sensitive assets that underperform in growth slowdowns that favour safe havens like US Treasuries and the US Dollar.

The main pillar of the view is based on a gradual global growth recovery in 3Q and 4Q after the 1H20 Covid-19 lockdowns. The depth of the activity decline is difficult to assess with any degree of certainty. Whether we are in the midst of a one- or a two-month lockdown, whether we are going to experience a second wave of lockdowns towards the end of the year on epidemic recurrence, and how well health systems and policymakers manage to deal with the spread of the pandemic and avoid permanent loss of productive capacity are all material unknowns.

While we acknowledge that further monetary and fiscal accommodation globally is likely and will attempt to mitigate the economic consequences of containment efforts, these actions are only softening the blow in the near term and are not likely to be sufficient to prevent technical recessions in either the DM or EM.

We expect the Fed to continue extending its efforts to mitigate the deflationary impact of the containment strategy. We expect Fed policy rates to remain around zero and QE/liquidity support for US Treasury, repo and money markets, ABS, MBS and US credit markets to remain in place until the US economy returns to normal activity, potentially in 4Q20. We do not rule out the Fed extending further liquidity support to US HY credit and specific companies in the worst-impacted sectors (e.g., Airlines). With their announced intention to do everything necessary to offset the pandemic’s impact next to a $2trn fiscal package passed by Congress, we would expect the Fed to manage to normalize global USD liquidity conditions as well as US Treasury and IG credit markets.

We also expect policymakers and central bankers across DM and EM to follow similar accommodative fiscal policies and, where possible, to revert to express QE and local bond buy-backs in order to mitigate the impact on the real economy and avert the excessive tightening of financial conditions.

Until global activity recovers, fiscal and monetary accommodations are unlikely to be inflationary, as the contraction of activity is unprecedented and deep. Lower oil/gas and industrial/agricultural commodity prices and a stronger US Dollar (benefiting from ‘flights to safety’ during recessionary periods) are likely to support the thesis of deflationary near-term dynamics.

China, in the process of exiting its two-month lockdown, is a test case for the rest of the world with respect to how quickly activity rebounds and whether there is a second round of epidemic spread as the population terminates social-distancing strategies. We do not expect growth in China to recover materially above 3% in 2020 (although a reversal-to-trend growth figure of 4-5% in the medium term is likely) since the lower external demand will detract from any recovery of domestic demand in 2Q and 3Q.

The oil-price outlook is quite uncertain and suppressed by both a higher oil supply and a sharp fall in demand as the global economy falters during the pandemic episode. OPEC is likely to meet in June, as scheduled, but is not, at this point, confident in a new deal on oil-production cuts being reached. We assume that oil will rebound from current depressed levels to an around $30-40 annual average.

We expect uncertainty and market volatility to remain elevated in the near term and until the pandemic risks start declining. We prefer to position as defensively as possible in the very near term and rotate from outperforming HY credits into underperforming IG credits.

In our medium-term base-case scenario, oil prices stabilize around $30-40, global growth declines to -1.5% in 2020, as most EM and DM enter technical recessions in 1H20, but a U-shape recovery occurs in 2H20, the EMD’s HY-to-IG spread tightens (as some of the sharp moves of oil exporters and vulnerable HY credits of early March are re-traced), as does the index EM spread (towards 350bps by year-end). In our base case, we do not expect Angola and Ecuador to enter ‘hard defaults’, as repayment schedules are relatively light, around $1.5-2bn each in 2020, and funding gaps can be sourced via as yet unannounced further fiscal tightening.

In EMD HC, we rotated from outperforming HY credits like Ivory Coast and Turkey into IG credits like India and Indonesia. We have also net-reduced exposure to Latam IG issuers like Chile, Colombia and Panama on concerns over pandemic containment. We scaled down exposure to the energy sector, with reductions concentrated in GCC.

Hard Currency

EMD HC (-1.0%) (-13.8%) recorded its worst month since October 2008 on a perfect storm of acceleration of the Covid-19 pandemic and OPEC's launch of an oil-price war (oil declined by 55%). Global equities entered bear-market territory on sharp growth revisions, confirming the end of the longest US expansion on record. DM policymakers extended extraordinary and unconventional monetary and fiscal support to relieve USD liquidity stress, normalize the functioning of key core-rate markets and mitigate the impact of containment efforts on households and businesses. EM central banks and governments followed by implementing a combination of rate cuts/local bond buyback programmes and counter-cyclical fiscal programmes. EM spreads widened by 253bps (to 626bps) while 10Y US Treasury yields declined by 48bps (to 0.67%), resulting in negative spread (-17%) and positive Treasury (3.8%) returns. IG (-8.1%) outperformed HY (-20.7%), with Lithuania (+1.2%) and Poland (0.4%) posting the highest, and Angola (-60.8%) and Ecuador (-59.3%) the lowest, returns.

EMD HC valuations have been restored and appear attractive relative to asset-class fundamentals on an absolute and on a relative basis. EMD HC now offers a yield of 7% and spread of 626bps, or the most attractive risk premiums since 2008. The HY-to-IG spread differential is, at 728bps, trading at its widest level ever. The medium-term case for EMD is supported by valuations, although the fundamental and technical/flow picture is complicated by near-term uncertainty with respect to the pandemic spread and impact on global growth, the timing of the economic re-start post-lockdowns, the EM downgrade and outflow risks. On a one-year horizon, we expect EMD HC to return around 23%, on an assumption of 10Y US Treasury yields at 1.25% and EM spreads at 350bps

We underperformed the index, with the largest detractors from performance the overweights (OW) in vulnerable oil-exporter credits like Angola, Ecuador, Pemex and Argentina. Underweights in IG credits (China, Philippines, Peru, Poland) also detracted from performance. In March, we initiated a rotation from outperforming HY credits (Ivory Coast, Turkey) into underperforming IG credits (India, Indonesia) while retaining exposure to distressed EM credits on expectations of higher recovery values. Our absolute (-46bps at 8.19yrs) and relative (-4bps at +1.06yrs) performances declined during the month.

We retain an overweight of HY versus IG. In HY, we reduced our exposure to Ivory Coast and Turkey, as these credits outperformed the correction in March.

In the Energy exporter space, we are net 8% and 0.71yr (spread duration) short vs the index, although energy exporters still contribute around 1/3rd of the overall beta DTS of the strategy. Our energy positioning is as follows: overweights in Azerbaijan and Kazakhstan, long-end Mexican Pemex and Brazilian Petrobras, small overweights in deeply distressed Angola, Ecuador and Iraq, neutral positions in Ghana and Nigeria, underweight in Gabon, full underweights in Russia, Oman and Saudi Arabia, and close to full underweight (-12%) in the remaining GCC bloc, with exposure concentrated in the higher-rated Abu Dhabi and Qatar.

We retain exposure to Argentina, whose assets trade is distressed around the mid-30s and below expected recovery values of around 60-70 cents on the US Dollar. In the IG space, we hold positions in Indonesia and Romania but remain underexposed to the most expensive parts of the IG universe like China, Malaysia, the Philippines and Peru.

We partially covered the mid-20s underweight in Lebanon just before the country officially defaulted on its $1.2bn March 9th debt maturity. We expect recovery values of around 35 as Lebanon will require deep haircuts to restore debt sustainability from its current public-debt-to-GDP level of 170%. As we expect a prolonged debt-restructuring process that may create opportunities for better entry points, we are staying on the sidelines for the moment.

In Brazil, Mexico and Turkey, we hold overweights in attractively priced corporate bonds versus underweights in sovereign bonds, for a total corporate exposure of 9.2%.

We hold single-name CDS protection positions in Mexico (5%, 0.20yr) against Pemex and a long CDX.EM (8%, 0.20yr) protection against further asset-class volatility. To hedge against further market stress, we have also installed a tactical 1.2yr 10Y US Treasury duration position that we see as a hedge to further deterioration in risk sentiment and flights to safety.

Local Currency

EMD LC saw a sharp 14% correction in March, mainly from FX (-12%) and rates (-3.3%), while carry added 0.9%. Throughout the month, cases of Covid-19 increased exponentially worldwide and the WHO declared a pandemic. While equity markets lost 20%, the fall in oil prices reached 55%, amplified by the ongoing price-war between Russia and Saudi. US Treasuries closed 60bps lower but – affected by serious liquidity disruptions – were selling off up to 60bps intra-month. High-beta FX led the sell-off, with the MXN (-19%) and the RUB and BRL (both -18%), underperforming, followed by the COP, the ZAR and the IDR. Asia outperformed the PHP (flat), the THB (-5%) and, generally, low beta, including CEE.

In the LC rates space, we saw more differentiation, with South Africa and Colombia underperforming on mounting fiscal concerns (+175bps and +130bps), and Turkey (+270bps) on external financing concerns. Other high-yielders retraced half the sell-off after a sharp mid-month rally (Russia +60bps, Brazil +28bps). Low-yielders on average closed wider, except Poland and the Czech Republic (-57bps and -13bps).

We outperformed the benchmark by 8bps on a net basis. Starting the month, we added to high-beta FX short to hedge our residual OW position, which was not proving easy to sell (Ukraine, Dominican Republic) and took profits after the Fed and ECB announced unlimited QE. Mid-month, we added to duration in US Treasuries and high-yielders (Brazil, South Africa, Russia), later taking some profits. We remain cautious in the medium term, as the lockdown measures take their toll on growth and fiscal balances.

At month-end, the USD long position of the fund stood at 16% (+10bps), with the beta unchanged at 0.96. The absolute duration of the fund is now 7yrs (+1yr) and relative duration 1.8yrs (+1.2yrs