As 2019 draws to a close, growth in the US will be positive for the 10th year in a row, which is the longest continuous period of expansion recorded since the mid-19th century. Over the past few years, the unusual length of the cycle has regularly instilled fear of an imminent recession among many doomsayers. Their rationale is based on a simple premise, i.e. the longer the period of expansion continues, the higher the risk of it ending. This logic is flawed, however, as Janet Yellen highlighted a few years ago, when she stated that “expansions do not die of old age”.

This year, however, fears of a recession in the US have been fuelled not only by the risk of the cycle running out of steam, but also exacerbated by trade tensions, coupled with a slowdown in economic activity in China and the rest of the world, amid heightened geopolitical uncertainties. These persistent threats, combined with fresh risks arising and the exceptionally long cycle, are highly likely to revive fears of a recession during 2020.

Although traditional macroeconomic analysis pinpoints sources of instability, including widening imbalances and asset price bubbles, and also highlights potential shocks which could tip economies into recession, such as a trade war or restrictive monetary policies, it nonetheless provides no objective gauge of the risk of recession. To remedy this situation, Candriam’s economists and quantitative fund managers have developed a set of proprietary quantitative indicators.

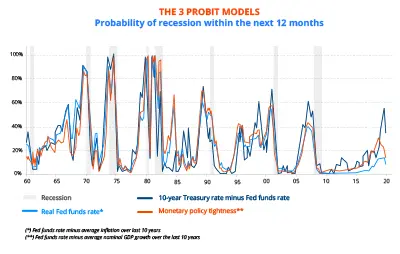

Originally, their construction drew on probit-type models. Probit models, which are derived from linear regression models, are used to assess binary variables. These types of model are used to estimate the probability of one of two different events occurring, in this case the probability of whether a recession will occur over a given timeframe or not. These models have nonetheless been proven to harbour a major default, as models with equivalent statistical properties over past periods can provide recession probability forecasts which differ greatly. The choice of predictor variables plays a key role and also strongly biases forecasts.

Estimations from three probit models based primarily on yield-curve steepness illustrate this inherent default. Whereas, in the past, the yield-curve slope, real short-term rates and monetary policy tightness also proved to be reliable indicators of an imminent recession in the US, signals over the past few years have diverged. Given the difficulty in selecting the “correct” model, i.e. choosing one of these predictor variables, which all adopt similar trends, there is a danger of making an erroneous assessment of the risk of a recession.

CHART 1: The 3 probit models

In order to remedy this difficulty, more sophisticated and more reliable methods can be used. Two key themes underpin the selected methods:

- Applying the “practice-makes-perfect” approach. In other words, there are no assumed certainties and applying these models to a broad variety of sample improves them and enhances their predictive ability.

- Adopting the “wisdom-of-crowds” or collective intelligence approach. A crowd’s diverse independent and aggregated opinions, as opposed to the discretionary choices of one single opinion, are collectively more intelligent than any of the component individual. Transposed onto our case study, the wisdom-of-crowds approach involves privileging aggregated information, provided by a multitude of models, over information from any one particular model. In other words, there is no point in seeking the best model from the past as there is no guarantee that it will remain superior in the future. It is therefore better to combine a widely diversified range of models in order to provide more reliable average information.

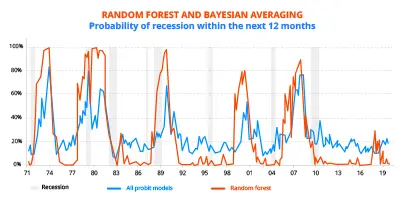

The following presentation outlines the results of the two models we have implemented. These models have been developed using a sample of around 100 economic and financial variables which may predict the onset of a recession within the next 12 months.

Method 1: Bayesian probit model averaging

This method is based on the estimates provided by several hundred thousand probit models combining up to four explanatory variables, of which only around 10,000 models are retained, as they are deemed sensible from an economic point of view. In the same way as a surgeon has to make a decision based on the interpretation of an x-ray on the eve of a delicate operation, the models are assessed taking into account uncertainties associated with new circumstances arising. In other words, each model is assessed in probabilistic terms. In applying Bayesian rules, the combination of models provides a recession probability founded on a rationale which also includes uncertainties.

Method 2: Random forest

The random forest method is based on a random collection of decision trees, which split variables into homogenous groups, selecting variables and their level successively, in order to classify events of interest more efficiently, in 2 groups of either: "increasing likelihood of recession within the next 12 months" or "increasing likelihood of recession within the next 12 months.

Unlike probit models, decision tress are non-parametric methods which take greater interaction complexity between variables into account. Their use has nonetheless traditionally been restricted, due to their instability. Any slight modification in data sample leads to highly different decision trees and therefore generates very different predictions.

The combination of the wisdom-of-crowds theme with progress in artificial intelligence, particularly machine learning since the early 2000s, has led to the emergence of an algorithm which remedies this issue, namely random forests. As its name would imply, this approach draws on the aggregate values of a multitude of decision trees (an entire forest) rather than a single tree structure, in order to reduce variance and bias within forecasts.

Variance is also reduced by implementing an algorithmic learning process across sub-periods (this is the “practice-makes-perfect” aspect) and reconciling predictions with observed reality outside of the learning periods.

CHART 2: Random forest and Bayesian averaging

These two methods are currently ascribing a relatively low probability of recession in the US within the next 12 months. The Bayesian averaging result predicting around a 20% probability has risen slightly since the end of 2017. The result provided by random forests is even clearer. After the probability of a recession ascribed by this method increased towards 20% from late 2017 to year-end 2018, it is now close to zero. The quantitative analysis that we have developed therefore substantiates the view held by our economists. Despite the current slowdown, the US economy is unlikely to tip into recession in 2020 (see our 2 December article on 2020 outlook).