Political uncertainties on both sides of the Atlantic have given low visibility to financial markets. We could expect investors to act with caution. Yet, combined with the massive liquidity support given by central banks and the falling real interest rates, it is growth sectors that have strongly outperformed. Until last week. The ever-widening gap between perceived winners and losers in the current sanitary crisis has narrowed – at least momentarily. Are the conditions met to have a rotation? The evolution of the Covid-19 epidemic and uncertainties around US elections will be key to tipping the scales. In the meantime, investors will need to mind the gap.

Winners vs. losers

Growth stocks have had a very good run, especially this year. The pandemic has boosted the revenues – and profits – of all the companies that facilitate life during a pandemic: Google, Apple, Facebook, Amazon and Microsoft have led US equities and led to their increasing – yet maybe not sustainable – concentration in the US market.

The significant decrease in real rates to an all-time low this summer has also been a powerful support for “growth” stocks.

Their leadership was called into question last week when the sector lost several percent in just one day. The widening gap between winners and losers might have encountered its first resistance.

Should we expect a rotation from growth/momentum to value stocks? Or was the market just washing out the excess momentum?

Today, there is no consensus. We can find arguments for or against a possible rotation in:

- the economic momentum: V-shaped rebound doomed to slow down given the pace of economic surprises;

- Covid-19: near-term exploitable vaccine vs. 2nd wave;

- US election uncertainty: Biden vs. Trump, i.e. higher spending vs. lower taxes;

- interest rate direction: modest steepening of the curve in the US vs. real rates means that the rate should stay lower for longer;

- the direction of the US dollar: usually a safe haven vs. upcoming longer-term vulnerability.

The only message that was loud and clear coming from the equity market was that momentum had reached an excess and that investors had chosen to take their profit. It is, however, too early to rule out a rotation.

Recovery vs stalling momentum

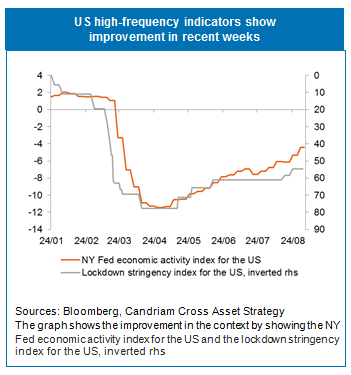

High-frequency data on Covid-19 trends, mobility, the job market, services, consumer comfort, etc. are holding up well so far and hint at a broadening of the economic recovery. While it is on track, momentum could stall towards the end of the year. Positive economic surprises have hit historical highs but, as expectations rise, there will be fewer of them in the last quarter of the year.

High-frequency data on Covid-19 trends, mobility, the job market, services, consumer comfort, etc. are holding up well so far and hint at a broadening of the economic recovery. While it is on track, momentum could stall towards the end of the year. Positive economic surprises have hit historical highs but, as expectations rise, there will be fewer of them in the last quarter of the year.

As a consequence, a flatter rebound into year-end and 2021 is expected from here on out.

There will also be less support for risky assets from real rates, which have stopped decreasing as we await further central bank guidance, in particular on implementation. But, hypothetically, a new US fiscal stimulus package could give the momentum a second wind.

What could tip the scales?

Looking forward, it seems reasonable to anticipate that market drivers will be:

- the evolution of the pandemic;

- the upcoming US presidential elections.

Those will be driving forces to tip the scales.

The evolution of the pandemic will very much depend on the availability and exploitability of a vaccine. In its absence, a new wave of infections in economically vital countries leading to the renewal of lockdowns would have negative consequences.

As far as the elections are concerned, financial markets are used to some volatility in those years but we are in an unusual context between the pandemic and persisting social unrest in the US. Too much volatility would jeopardize the continuity in the recovery, and the three upcoming presidential election debates, the elections, the possible contestation of results and the subsequent inauguration are potential triggers of above-average volatility.

Once the election dust settles, there will be a macroeconomic alignment on expansionary policy: higher spending (Biden) vs. lower taxes (Trump) in a context of an accommodative Fed but post-election congressional deadlock is still a risk.

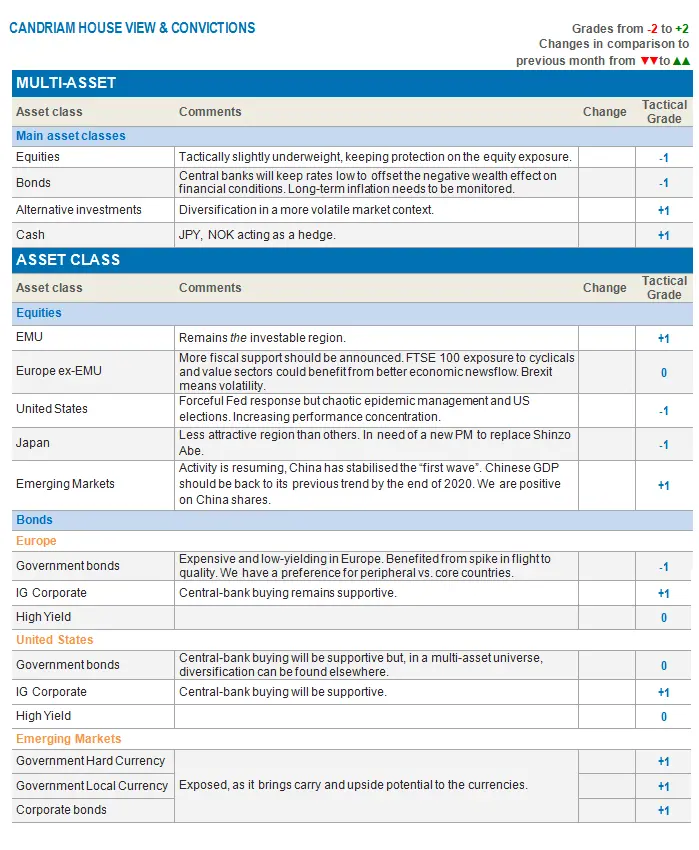

Our current multi-asset strategy

Our overall equity exposure has stayed slightly cautious, due to the obvious risks, and we are continuing to protect European and US equities via options and portfolio hedges (gold and JPY).

To benefit from the ongoing economic recovery, we are restricting our exposure to a structural reduction of the euro zone risk premium: long EMU vs US equities. We also remain neutral UK equities, as, even though these could benefit from better control of the epidemic, the Brexit situation is increasingly weighing on them.

We are keeping Chinese A-Share equities and remain overweight on emerging equities but underweight Japan.

Our bond allocation has stayed stable and remains positive on credit Investment Grade (Europe and US) and emerging debt (preferably hard currency).

We are also maintaining a short duration bias, an underweight exposure to government bonds in Europe (on core countries) and an overweight in peripheral European bonds.

Our currency allocation is short USD vs. EUR, short USD vs JPY and long NOK vs EUR.