In August, the investing environment was troubled, with the impact of the Delta variant and the new regulatory measures applied by the Chinese government disquieting investors, afraid of the consequences of the supply-side constraints (labour and product-line shortages) generated by these events. However, the markets, reacting calmly (volatility remained quite low), remain confident about underlying growth, which is currently fed by fiscal plans and the still-ample liquidity. In this context, commodity prices have been receding, the US Dollar has been really strong and yields were slightly up.

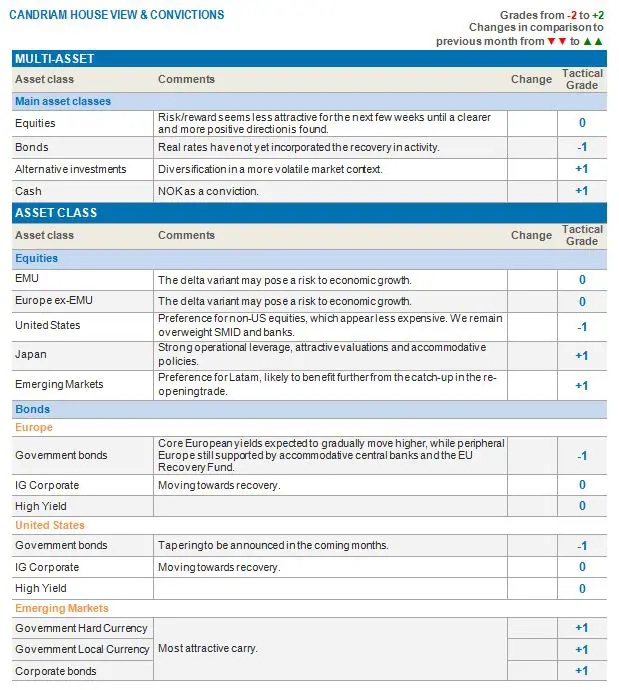

A sound context with some challenges

The economic indicators have been less buoyant in recent weeks. It is clear that the slowing Chinese economy is weighing on the world. In fact, although the regulatory measures recently impressed the financial markets, previous measures to cool the economy and the COVID-19-generated harbour lockdown are more damaging. Moreover, the US fiscal plan, strongly anticipated over the spring, has not yet been voted and there are many uncertainties about its magnitude. All these elements induced a globally weaker-than-expected Q3 in the US and in China. Furthermore, if vaccination progress has been quite sensible in the developed world, the same cannot always be said about the emerging countries.

The economic indicators have been less buoyant in recent weeks. It is clear that the slowing Chinese economy is weighing on the world. In fact, although the regulatory measures recently impressed the financial markets, previous measures to cool the economy and the COVID-19-generated harbour lockdown are more damaging. Moreover, the US fiscal plan, strongly anticipated over the spring, has not yet been voted and there are many uncertainties about its magnitude. All these elements induced a globally weaker-than-expected Q3 in the US and in China. Furthermore, if vaccination progress has been quite sensible in the developed world, the same cannot always be said about the emerging countries.

However, investors remain confident about the underlying strength of the world economy, as PMI levels are quite high, even if the momentum has been decelerating. Admittedly, although central banks have begun to express their willingness to reduce their monetary support, they will be very slow to move in that direction. They have constantly insisted on the transitory character of inflation and don’t see any interest-rate hike before 18 months, at least. That’s why volatility is quite low on FX and bond yields. Stock markets (notably in the US), big caps and growth stocks benefited from that context.

Risks to the scenario

One risk is that supply-side constraints could last longer than anticipated, notably on the labour market, threatening the consuming sector. Companies would be squeezed between higher inflation and lower sales. The diffusion of the variants needs to be closely watched, too. Even if the new vaccines seem to be efficient versus the current batch, it could affect the re-opening, or at least the nature of the coming months’ growth. This would push long-term yields lower and could dent investor confidence in a “goldilocks” scenario, transitory inflation, and solid and durable growth. Finally, central banks need to be very cautious about how they reduce their monetary support.

Our credo

We believe that the environment will remain challenging in the coming weeks but will be transitory.

On a very short-term view, the end of the quarter might bring some portfolio rebalancing, with stocks being sold after a very positive performance. September’s FOMC meeting will also add to uncertainties about the FED mantra. Not forgetting that the Chinese situation remains tricky.

Nevertheless, we remain confident about the structural component of growth, notably in Europe, as the fiscal plans and the German election may add to the momentum in the coming months. We may also see inflation anchored at a relatively high level. If this happens, we believe that long-term rates should move higher, notably in the US, where the Biden plans have yet to be implemented. Therefore, if history is any guide, in this environment, the Value sector, i.e., European and Japanese stocks, should outperform US stocks. We believe that the small-caps sectors - which have been lagging their peers - may catch up, as regards re-opening, in the coming months.