The year ended with financial markets firing on all cylinders and this carried on through the first week of January as, one by one, risks faded into the background on investors’ list of priorities. Indeed, in spite of the continued denial of Donald Trump, Joe Biden was confirmed as the winner of the 2020 presidential election, and will also carry with him a majority in the House and the Senate. A deal was reached at the very last minute on Brexit, an issue that has been omnipresent since 2016. And, finally, several vaccines burst onto the scene towards year-end and countries started their vaccination drives in December. In the meantime, fiscal and monetary stimulus continued to churn slowly but surely in the background, with additional measures announced in December. The ECB added an extra EUR 500 billion to its bond-buying programme, underlining once again that it is now the ultimate buyer of last resort and that it can continue to do more in order to support financial stability. In the US, though fiscal stimulus has been slow in its formulation in the midst of political discord, a much-needed $900 billion package was announced, with the hope that the new administration would do more to support the economy. These events helped prolong the market rally that we had witnessed in the second half of the year. Credit spread markets (including IG and HY) had an excellent month of December, ending the year firmly in positive territory. Emerging market debt also had a very strong month both on the hard as well as local currency front as FX as well as duration contributed to the positive returns. On the developed sovereign front, core yields saw an uptick as a result of better macroeconomic data and slightly improved inflation data.

Overall, we expect the current trend, in terms of macroeconomic data, to continue. The vaccine drive in the US, Europe and across the globe should continue and hence be supportive of the global recovery. We expect more fiscal stimulus in the US while the Federal Reserve should remain accommodative. Europe has already provided a strong fiscal and monetary stimulus but the vaccine drive is shaping up to be slower than expected. Furthermore, within the continent, countries seem to be operating at a different pace – not just in terms of vaccination – and the Next Generation EU programme still needs to be ratified. However, it is important to note that the current market sentiment does not appear to adequately price in some of the inherent risk that has to be borne in mind. In spite of the vaccines (which do not prevent transmission of COVID), lockdowns continue and, if the pace of vaccination does not pick up, this could continue. Furthermore, though the Democrats do seem to be in firm control of the House of Representatives in the US, populism doesn’t appear to be a phenomenon of the past and could be an impediment to the overall policy of the new government. Though the Brexit deal has been signed, the overall impact is still not fully known. As a result, we believe that, in spite of an overall positive view on markets, we are going to continue to exercise caution and remain active. Finally, as fixed income investors, the issue of valuations remains key here. Even though markets are boosted by positive news and strong fundamentals, it is clear that the compression of spreads and yields (already at record lows) has its limits and will place a cap on returns in Fixed Income markets.

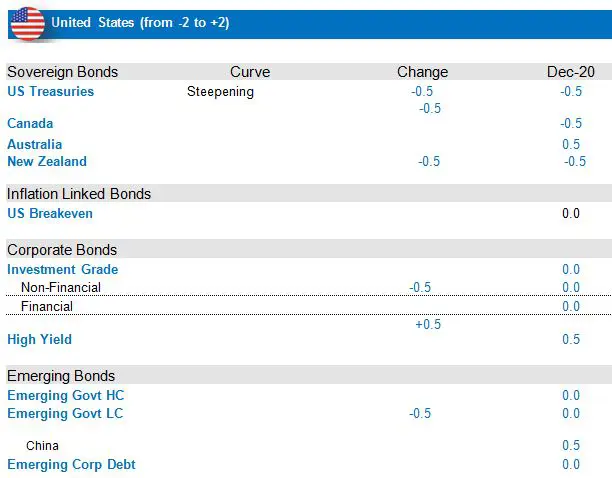

Negative stance on US rates and neutral on European Rates

The return of growth and inflation are welcome in the US, and could continue on the back of the additional fiscal stimulus that is more likely to be voted, as the House of Representatives is firmly in the hands of the Democrats. Joe Biden’s agenda will be focused on additional fiscal stimulus and should hence provide vital and much-needed support. There is little reason to think that the Federal Reserve will not pursue its low-rate policy and bond-purchase programme. In this context, we expect US rates to continue to move upwards. This could lead to an upward movement of a curve that has already steepened on the back of recent Fed policy (to tolerate inflation at target levels for a longer period of time). This rise in rates, however, has not only been capped by the QE programmes (that include $100 billion/month of purchases, with a possible extension in duration), but also by the potential increase in the number of COVID cases and continued social distancing across the states. That said, there is notably more technical upward pressure on rates from the large excess supply than in the past 10 years. However, as long as the FED maintains its asset purchase programme, a massive sell-off seems unlikely. In summary, given the context, we hold a negative view on US rates, though we are managing our short positions tactically.

On the other hand, other rates on the dollar bloc offer opportunities, as we hold a positive view (on a currency-hedged basis) on Australia on the back of an accommodative central bank where QE is being deployed and rates are at slightly more attractive levels than in other core markets. Our previously positive exposure to New Zealand rates has been reduced to negative on the back of some positive economic data, a tapering of monetary support in the form of scalebacks in central bank asset purchases and a less attractive carry. Lastly, we took profit on the longs we had implemented on the short-end of the Canadian curve as the outlook has become more negative.

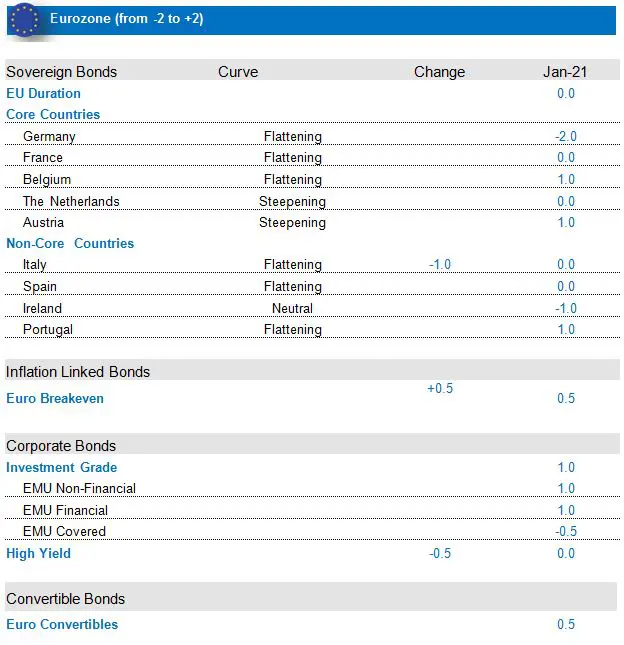

In Europe, new lockdown measures have been re-introduced in the face of a rising number of corona cases, and the latest wave of the pandemic remains substantial, further pressuring the economy. In spite of the announcements, the ongoing significant concerns on distribution and on the willingness of the population to take the vaccine are a significant driver of the relatively weaker growth and inflation picture versus the US. An acceleration in growth can nevertheless be expected in the second half of the year, thanks to an improving health situation and investments under the ERF. The budgetary cycle is less supportive, with budget deficits likely to remain large across Eurozone countries. Monetary policy, on the other hand, driven by the APP and PEPP, remains exceptionally accommodative, and the recent increases and extensions of these bond-buying programmes will continue to offset the weakness in fundamentals. Furthermore, technicals are also quite strong, as net flows for Euro sovereigns will remain negative, thanks to lower funding pressure. For core markets, fair-value indicators continue to point to their expensiveness. Investor positioning remains a negative driver, being still close to multi-year highs. In this context, we continue to hold a negative view on core rates while managing the position very tactically, taking into account the weak valuations. While economic risks weigh more heavily on non-core countries, the outcome for the European Recovery Fund, with sizeable grants, should clearly be positive for non-core countries (but awaiting final validation, as Hungary and Poland still oppose). In this context, we continue to favour non-core sovereigns, in which yield levels are relatively more attractive. Hence we prefer exposure to Portugal and, to a lesser extent, Spain, whereas we are tactically neutral on Italy, in light of potential political uncertainty. Lastly, we have initiated a tactical long on Eurozone Breakeven, where we expect a rise in Eurozone inflation over the short term, driven by supportive short-term inflation dynamics (among others, the German VAT cut reversal and the new EMU HICP weights).

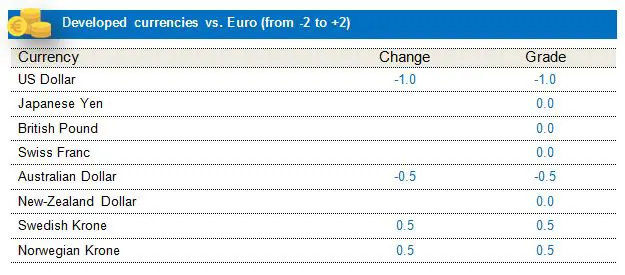

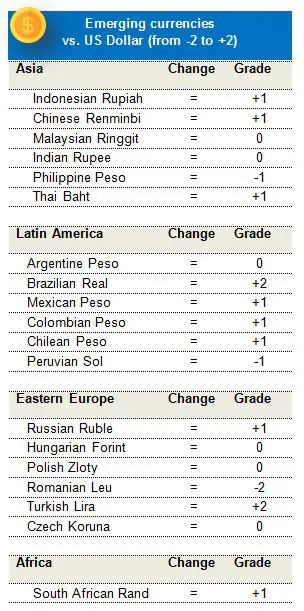

Developed Market Currencies: Short position on USD

Our proprietary framework continues to point towards a negative view on the US dollar, on the back of rising twin deficits. The Fed’s rate cuts, QE programme and dovish stance also point to a weaker dollar.

Credit: Favouring European credit markets, overweight convertibles

The improvement of medium-term prospects, thanks to the vaccine drives and ample monetary support, have weighed on the balance of risks. However, it is important to note that there seems to be a certain level of complacency in the markets, which seem to be pricing in all the good news, leaving aside the potential pain for now. Indeed, the resurgence of COVID and negative developments on vaccines (as an example) could once again hurt issuers and deal set-backs to their balance sheets. In this context, being highly selective is key. Through our in-house, bottom-up analysis of issuers, we continue to target highly liquid assets of high-quality companies with strong internal credit ratings and low leverage, as balance-sheet repair will represent a major challenge for corporates in 2021. Demand for spread products will stay strong, while supply will remain negative on a net basis, favouring compression trades, especially in the High Yield segment. The default rate could peak in Q1 2021 and decrease thereafter, as progressive herd immunity is achieved through vaccination programmes. This will, in turn, support the more cyclically exposed sectors.

Euro IG: While maintaining our favourable view on the European credit investment-grade asset class, we continue to closely monitor idiosyncratic risks and exercise a high level of selectivity. Balance sheets are on the mend while downgrades and rating drifts bottom, with rating agencies in wait-and-see mode. The ECB’s direct and increased purchases are providing an important backstop and, as a result, technicals are receiving strong support. Valuations remain a source of concern, though, within the asset class, where we are spotting relative-value opportunities across ratings and sectors.

Euro HY: The asset class should be supported by a relatively attractive carry in a low-yield environment, and supply is not an issue, as companies are relying more on bank loans than on capital markets. However, performance has already been quite strong and yields and spreads have compressed significantly, close to pre-crisis levels. In this context, as we believe that some profit-taking might be in order, we are moving to neutral on the asset class, particularly in the absence of a sharp macro improvement in the Eurozone.

Finally, we think EUR Convertibles should benefit from positive dynamics such as the coordinated action from the EU Next Generation Recovery Fund, positive surprises / better visibility from quarterly results, less political noise than in the US and some economic recovery.

EMD: Towards a more positive view

The near-term outlook for emerging market hard currency debt has shifted to more positive as the uncertainty around US elections was cleared and rollout of vaccinations has started globally. Health risks remain elevated around the discoveries of new and more contagious virus variants in South Africa and the UK that are forcing re-introductions of tightening measures. We find ourselves amidst a challenging second pandemic wave that is straining health systems’ resources and has required stricter lockdowns and mobility restrictions. Risk markets have ignored health risks so far as vaccine distribution is accelerating and fourth quarter data was stronger than expected in the developed world suggesting a high level of adaptation and likely more limited impact from mobility restrictions on activity relative to the first half of 2020. We would like to confirm that the vaccine rollout proceeds successfully and that the second pandemic wave peaks before adding risk further to align with our constructive asset class view.

Our January global market assessment update acknowledged favourable financial conditions with ample global liquidity, supportive developed market central bank policies and constructive view on commodities (Oil, Industrial and Precious Metals and Agricultural products). We expect that oil prices (Brent) will move up towards a $50-$60 range as the supply overhang has cleared and global demand accelerates towards the mid of 2021. Commodity prices traditionally exhibit high correlation with global demand recoveries and should perform well in 2021 overall which in turn should benefit EM commodity exporters. We expect that in the medium term, the weakness of the US Dollar is well established due to the sizeable twin deficits the US have accumulated and to the near doubling of the Fed's balance sheet in 2020. Strong or stable commodity prices and a weak US Dollar have traditionally been supportive for emerging market hard currency debt and emerging currency performance as the majority of emerging countries are commodity exporters. Uncertainty around the de-rating of the emerging country universe and the resolution of specific liquidity and solvency issues in some emerging countries remain, but these are going to be addressed on a case by case basis and are unlikely to impact the overall performance of emerging market debt.

We also noted a broadening Chinese and EM economic growth recovery and extended stabilisation of asset class flows. After the US election cycle cleared the path for the US Congress’s approval of a $900bn stimulus package in December, we are now somewhat more concerned about a potentially faster paced US growth versus the rest of the world over 2021 which may create headwinds to the performance of growth sensitive emerging currencies and equity markets. We also acknowledged that emerging and US inflation seems to have bottomed which poses downward risks to rates performance globally. We upgraded our EM external sector balances score further as we noted overwhelming evidence of positive current account and trade balance trends across the emerging country universe.

Emerging market hard currency debt valuations are somewhat extended versus asset class fundamentals, but still appear attractive on relative basis versus these of developed markets and considering that the high yield versus investment grade asset class spread differential still offers value. Emerging hard currency debt offers a spread over US Treasuries of 352 bps, or in line with its 5-year average of 360 bps. The high yield versus investment grade spread over US Treasuries differential is at 443 bps, or 61 bps wider relative its 5-year average of 368 bps. The medium term case for emerging market debt is supported by relative valuations in the high yield segment, bottoming of fundamentals, abundant global liquidity and supportive technical factors that are likely attract inflows into the asset class in 2021.

Concerns over emerging debt sustainability have been partially resolved as primary markets accommodated a record $230bn of gross emerging debt supply over 2020. Next year’s asset class technical conditions remain constructive as the expected $180bn of gross and $55bn of net sovereign supply is lower than the expected asset class inflows of $65-75bn.

We scored the asset class technical conditions at a small negative for the moment as sovereign positioning is at an uncomfortably high level and gross supply is seasonally high during the first quarter of the year, and despite our constructive expectation for asset class inflows.

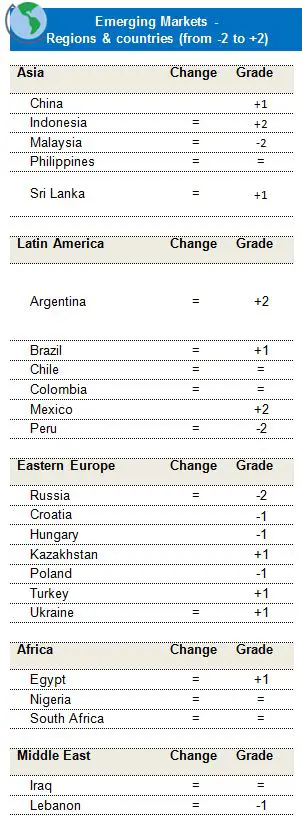

China: We hold a positive view on Chinese sovereign bonds, where real yields are quite attractive and the economic recovery appears remarkable. Following the inclusion of these asset classes in the index, it has been supported by strong flows from foreign investors.