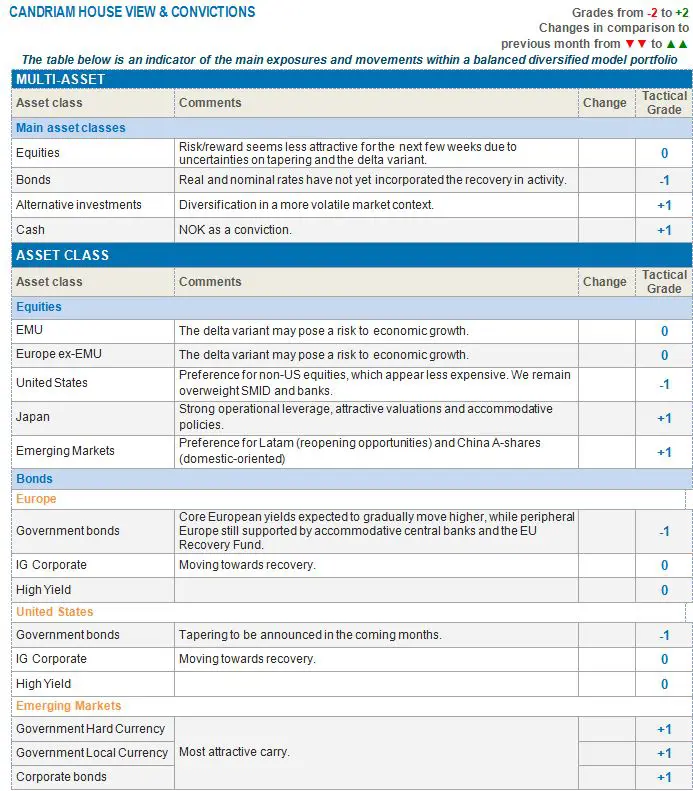

In July, the still-positive economic indicators bode well for a continuation of the economic recovery, even at a slower rate. The service sector is benefiting from the vaccination campaigns in the developed countries, while the manufacturing sector continues to thrive. Even if supply-side constraints, due to the strength of the rebound and the specificity of the crisis, continue to weigh on the economy, investors have chosen to focus on the strong company earnings and, helped by the bond yield decrease, to be optimistic about stocks, fast becoming the growth sector.

A more divided world

The situation around the world is very diverse. Early on, vaccination progress was focused on the developed countries, more precisely the US and Europe, rather than the emerging countries, which have come very late to the programme. This could threaten a complete reopening, should new variants emerge. Moreover, there are some idiosyncratic contexts, as is the case in China. Indeed, the Chinese government has chosen to apply strict regulatory measures to tech companies, even while proceeding with a general monetary easing. This is weighing somewhat on the emerging markets.

The situation around the world is very diverse. Early on, vaccination progress was focused on the developed countries, more precisely the US and Europe, rather than the emerging countries, which have come very late to the programme. This could threaten a complete reopening, should new variants emerge. Moreover, there are some idiosyncratic contexts, as is the case in China. Indeed, the Chinese government has chosen to apply strict regulatory measures to tech companies, even while proceeding with a general monetary easing. This is weighing somewhat on the emerging markets.

This environment, a mix of uncertainty about COVID-19 amid support from the main central banks, induced some cautiousness among investors. Such caution, driven by lower real yields, led, too, however, to lower nominal bond yields. The financial institutions, along with central banks such as the ECB, the BOJ and the FED, continued to buy bonds, reducing the term premium.

The economic recovery has benefited companies showing very strong earnings. As growth remains on track, helped by cautious central banks and more fiscal support for the coming years, the context remains quite positive for stocks.

Our credo

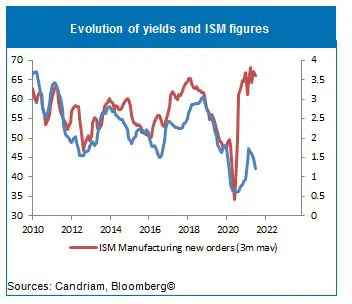

The downward move of nominal and real bond yields in recent months does not, in our view, reflect the growth path expected over the coming years. ISM figures currently show a large discrepancy between the economic situation and long-term yields.

Moreover, the Fed could slightly reduce its bond purchases, as the labour market is improving. The term premium could therefore increase. Inflation, too, seems anchored at higher levels than anticipated. This being the case, we believe that long-term rates should move higher, notably in the US, where Biden’s plans have not yet been implemented. In the same way, the fiscal plan in Europe, with the NGEU, will be unveiled over the next few years. Therefore, if history is any guide, in this environment, the value sector, comprising European and Japanese stocks, should outperform US stocks.

We remain alert about the societal changes, green and equitable, which will have a durable impact on markets, moving investors’ choices and company margins, depending on their abilities to adjust.

Risks to the scenario

The diffusion of the variants needs to be closely watched. Even if the new vaccines seem to be efficient versus the existing ones, it could affect the reopening, or at least the nature of the next few months’ growth. It would push long-term yields lower. Another risk involves supply-side constraints lasting longer than anticipated. This would mean a more durable inflation and a squeeze on company margins. Investors could be less confident about a “goldilocks” scenario: transitory inflation and solid and durable growth.

Our current multi-asset strategy

As market liquidity is usually poor during the summer season, there could be some volatility. We are therefore hedging the global equity portfolio risk by buying some protection on European equities to be neutral equities vs. bonds. On the fixed-income side, we remain underweight government bonds, due to the current low-yield levels.

However, as regards the longer term, we continue to believe in a broad recovery, i.e., higher inflation and higher yields, which should benefit the value sector. In that environment, we remain positive on European, Japanese and small-cap equities, as well as on some emerging markets, Chinese A-shares (domestic-oriented) and Latin America stocks.