As economic uncertainties intensify in the United States, European fiscal policies are emerging as a beacon of hope. We are navigating a perceived “risk-off” environment by reallocating equity positions away from the US, favouring European markets and diversifying across global equities. Simultaneously, the rising risk premium is driving a shift towards sovereign bonds in both the US and Europe. Our investment convictions underscore the growing concerns about a potential “Trumpcession”, juxtaposed against Europe’s efforts to stimulate economic growth, notably via massive defence and infrastructure spending in Germany.

As a consequence, we have reduced our stance on global equities to neutral, adopting a balanced approach across sectors and regions ex-US, while shifting towards an underweight on US equities. Regarding fixed income, we prefer duration exposure in core Europe (Germany) due to expectations of continued low growth and disinflation trends in 2025. Conversely, we are no longer short on US duration, anticipating that downside risks on growth outweigh upside risks on inflation in the coming months. Additionally, we rebalance the Euro/US dollar pair and remain buyers of the Japanese yen.

Risk-off sentiment and the US market

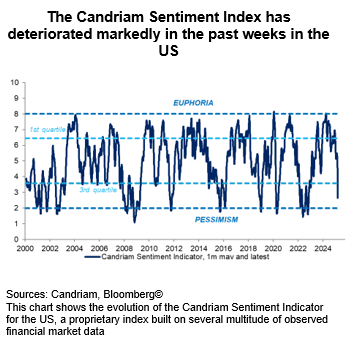

The current market climate calls for a more cautious approach, emphasising geographical diversification to mitigate market volatility. A “risk-off” sentiment has taken hold, leading investors to reduce their exposure to US equities.

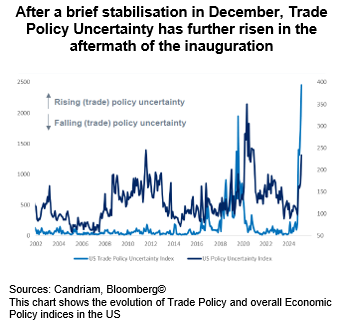

With Donald Trump’s return to the political arena, there are fears of tariff escalations, potential trade wars and, ultimately, fiscal tightening that could stifle economic momentum. US tariff actions on Canada and Mexico carry significant economic implications, especially given the integrated North American supply chain. Many market participants have been forced to reconsider initial expectations, where Trump tariffs were seen as mere negotiation tactics.

The sharp rise in trade policy uncertainty under Trump’s second term is unprecedented, surpassing levels seen in his first term. This uncertainty is impacting investment decisions, inventory management and broader economic forecasts, leading to downward revisions in US growth expectations and therefore nurturing a negative feedback loop.

Perhaps more troubling is the erratic nature of policy implementation, making risk assessment and pricing exceedingly difficult. Taken together, several factors have compounded into more bearish conditions exceeding the sum of their individual parts, negatively impacting both business and consumer confidence and escalating “Trumpcession” concerns. In a nutshell, this sharply deteriorating environment has been provoked by multiple factors:

- A US economic slowdown: GDP growth in the US is projected to decelerate, with indicators suggesting a slowdown from close to 3% in 2024 towards 2% in 2025. Rising trade tensions, economic uncertainty and tighter financial conditions are already weighing on confidence and incoming economic releases. This slowdown translates into a downward trend in economic surprises, which have turned from positive to negative at the end of February, mirroring the movement from last spring.

- Trade war risks: After imposing aggressive US import tariffs on China, Mexico and Canada, followed by “reciprocal” tariffs on the rest of the world, global trade flows could suffer, reducing corporate earnings and economic growth.

- Fiscal austerity: Current budget discussions in the US suggest potential spending cuts that could disproportionately affect lower-income households, reducing consumption and economic activity.

To hedge against these risks, we are shifting capital towards Europe and emerging markets, where valuations appear more attractive and fiscal stimulus policies are gaining traction.

European fiscal stimulus – a contrasting narrative

While the US economy grapples with policy uncertainty, Europe is embracing a more proactive fiscal stance. Recent initiatives indicate a commitment to supporting growth and position Europe as a more stable investment destination, reinforcing the shift away from US equities:

- Loosening of fiscal constraints: The European Commission has indicated greater flexibility in fiscal rules, allowing higher deficit spending to drive growth.

- Defence and industrial investments: The majority of European fiscal easing is likely to be channelled towards increased defence spending and incentives for manufacturing, which is contributing to a more optimistic growth outlook.

- Germany’s €500bn infrastructure fund: Confirming this spectacular change of mindset regarding strict fiscal austerity, Germany has proposed a 10-year infrastructure package focused on railways, digital infrastructure and energy networks. This is expected to stimulate economic activity by close to one point of GDP p.a. from 2026 and create a more favourable environment for long-term investors, including via mid-cap stocks.

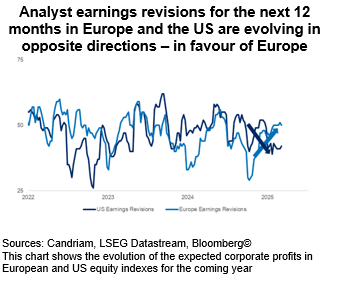

- European earnings improvement: As a consequence, corporate earnings expectations in Europe are being revised upward, contrasting with downward revisions in the US. This fundamental strength underpins the outperformance of European equities year-to-date.

It is worth bearing in mind that although Europe has so far been less affected by US tariff policy, potential future tariffs –possibly starting on 2 April – could create new risks. This is an important fundamental driver which prevents us from becoming more optimistic on European equities.

Across the pond, we note that the US stock market, which had enjoyed an extended rally driven by mega-cap technology firms, is facing some headwinds as corporate earnings have come under pressure. Trump’s “Drill, Baby, Drill” approach is leading to an oversupply of oil, driving down global oil prices. While this is certainly reducing inflationary fears, it is also reducing earnings growth in the energy sector, as OPEC countries have committed to restoring output.

As a consequence, we have reduced our stance on global equities to neutral, adopting a balanced approach across sectors and regions ex-US, while shifting towards an underweight on US equities.

While reducing US exposure, maintaining diversified equity exposure is crucial in 2025. More uncertain in the short-term, global equities still present long-term growth opportunities and we are allocating capital across different regions and sectors: we maintain an overall neutral view on Emerging Markets and Japan. In particular China, despite ongoing geopolitical risks, continues to be a key player in global markets. The country’s commitment to fiscal support and industrial capacity expansion offers selective investment opportunities.

Upgrading bonds – increasing US duration, staying Long in Europe

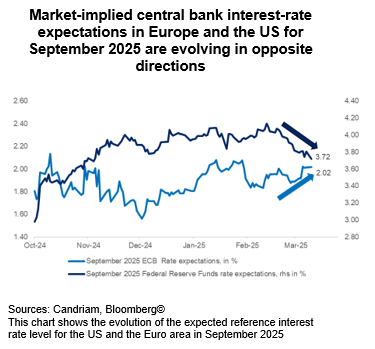

The factors underpinning downward revisions in economic and profit growth are also visible on interest-rate markets, as monetary policy expectations have been pushed in opposite directions by US growth fears and by European fiscal spending hopes. Regarding Germany, the increase in defence funding is likely to be merely a technical hiccup in terms of absorbing additional issuance, rather than a fundamental problem for the country’s AAA status.

As economic uncertainty rises, so does the appeal of high-quality bonds. With risk premiums widening, investors are rebalancing portfolios to include longer-duration bonds in both the US and Europe. We hold the following convictions:

- Positive European bonds: With fiscal stimulus supporting growth and inflation remaining relatively contained, long European duration remains attractive. German real yields have risen, reflecting confidence in fiscal plans, while European bond spreads remain relatively stable. In this context, we maintain a long duration stance via German Bunds.

- Neutral US bond market: Despite near-term economic uncertainty, the Federal Reserve is expected to maintain a cautious stance on interest rates for the time being. This provides an opportunity to extend duration in US Treasuries, capitalising on higher yields while mitigating potential equity market risks. Contrary to market expectations, which have shifted significantly since the end of 2024, our Fed policy expectations remain anchored around two rate cuts in 2025, followed by two additional cuts in 2026.

- Downgrade High Yield bonds to underweight: In line with an overall more cautious investment environment, we have downgraded European and US High Yield bonds to underweight. Spreads remain below historical levels as credit technicals and fundamentals remain strong. High Yield credit appears to be the weakest link in a multi-asset portfolio, as an improvement in the environment would have little impact on spreads while a deterioration could lead to a widening. Clearly, convexity has been priced out as policy uncertainty is rising and hurting sentiment.

To sum up, in this evolving economic landscape, a proactive and flexible investment strategy remains crucial. A more cautious approach necessitates reducing US equity exposure while maintaining a diversified portfolio. In particular, European fiscal stimulus provides a counterbalance to US uncertainties, reinforcing the case for rebalancing towards European markets. In the fixed income markets, the rise in risk premiums supports an allocation shift towards long-duration bonds in the US and Europe, while reducing High Yield. As Trumpcession fears grow, investors must navigate these dynamics carefully, seeking stability in a volatile world.