Technicals, rates, geopolitics, China – anything new in the EM credit markets? Well, yes. Fundamentals are rather surprising. And the rising importance of Environmental, Social, and Governance factors to issuers has been a breath of fresh air.

EM Corporate Credit Landscape

The global economic environment for 2022 will present a challenge for EM corporate credit investors. Rising consumer prices, supply bottlenecks, and commodity prices set the scene for rising rates. The relative calm provided by developed market vaccine rollouts has recently been shaken by the new Omicron variant - a stark reminder that the pandemic is not yet over. Investors must be prepared for potential Covid-19 tail risks, with effects to linger for years.

The Green Scene

Overall, we expect Technicals to remain favourable. Issuance, which had been growing strongly for several years, should plateau at $500bn in new deals in 2022, with around $100bn in net new financing after repayments of coupons and redemptions. Investor demand for EM Corporates as a stand-alone asset class is likely to grow, while the absolute level of issuance is sufficient to provide strong diversification opportunities.

Sustainability bonds should account for almost a fifth of new issuance, about half of which is expected in green bonds. This could attract a new group of investors to the asset class.

Valuation Scenario

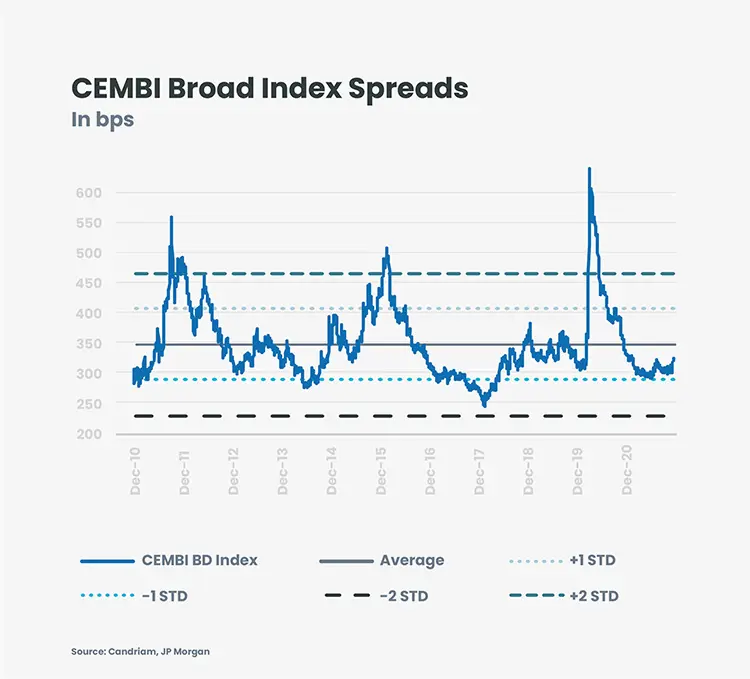

Our core scenario is for a 3%-6% return over 12 months (in dollar terms). The realised absolute return will heavily depend on the path of US Treasury yields. We are assuming global EM corporate default rates of 3-4% in 2022, for a CEMBI BD Index 'fair value' of roughly 250bps, implying around 60-70bps of best-case spread-tightening potential, mostly in the-lower rated segment. While today's spreads may be below historic averages, they appear to be pricing in the credit improvements of recent quarters.

What Doesn't Sink You Makes You Stronger

Fundamentally, Emerging Market corporations pass the health check with flying colours. Whilst base effects have contributed to strong year-over-year comparisons, we are impressed with the proactive balance sheet and liquidity management we witnessed. In many instances, EM corporate issuers have already returned to 2019 EBITDA levels, with expanding EBITDA margins. Net leverage improved from an average of around 2.3x to 1.7x in 2021, with interest coverage up. Cash liquidity is at very comfortable levels across most sectors.

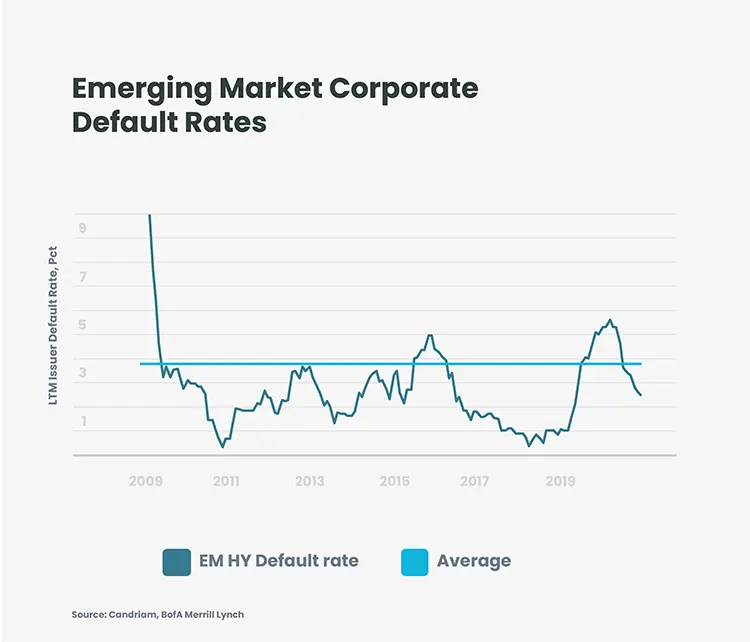

Improving credit trends are visible in declining default rates. Default rates spiked during the peak of the Covid-19 outbreak in 2020, breaching the 5% level for the first time since the commodity slump in 2015-2016 and only for the second time since the Great Financial Crisis of 2007-2008. Since the depths of the financial market downturn caused by the Covid-19 outbreak at the end of 1Q 2020, we have witnessed a sharp improvement in defaults as the pandemic progressed, economies re-opened and vaccines were rolled out. While we expect default rates to rise again in early 2022, we expect events to be concentrated in the Chinese real estate sector where elevated uncertainty together with a number of high profile defaults will have knock-on effects. Some weaker-rated Chinese developers have heavy maturities in Q1 2022, and are likely to face funding difficulties.

Issuers Recognizing Sustainability

For ESG-focused investors the landscape is changing dramatically. While the specifics of European SFDR regulations primarily concern European asset managers, the topic is gathering pace across financial intermediaries and EM Corporate issuers. Encouragingly, we are witnessing greater transparency from Investor Relations departments, more active dialogue and more serious discussions. This progress is leading to a significant increase in sustainability-linked bonds, while a new investor base is being attracted by these opportunities.

Elections Calendar

The elections calendar is a frequent source of volatility in Emerging Markets, and 2022 looks to be a big year. Two presidential elections are scheduled in May, in Colombia and the Philippines. The most important will be the Brazilian elections in October. It is highly likely that the ebb and flow of the political cycle in these large EM economies will drive corporate sector spreads around the elections dates as investors weigh-up the candidates and the impacts of their manifestos.

Macro Trends

The Federal Reserve taper, the path of core yields, and the pace of their adjustment will have a meaningful impact on returns. Commodities are at relatively high levels aiding the balance sheet health of commodity-oriented issuers.

Geopolitics will be a further important return driver as Chinese territorial ambitions collide with US Asia-Pacific interests, whilst Russia-Ukraine tensions are heating up.

Spreads on China Property sector bonds have now reached extremely attractive levels. The sector now accounts for 22bps, or 7%, of the benchmark CEMBI Broad Diversified spread with an index weight of only 1.6%.

Where are the Surprises?

It should be no surprise if the Chinese property sector, geo-political tensions, elections, and the path of US interest rates keep analysts busy this year.

Yet, despite the pandemic, surprisingly strong credit metrics and technicals combine for an attractive outlook for Emerging Market Corporate Bonds. The expected issuance of sustainability-linked bonds, which are new even to mature markets, is a pleasant surprise which should attract a new group of investors. Something to look forward to!

Having said that, 2022 will be a challenging year for investors who wish to diversify their portfolios in EM credit. Selectivity and ESG integration might be the watchwords in implementing these strategies.