In May, the recovery was well underway, with economic indicators, notably the PMI, still at high levels and the vaccination campaigns helping investors believe in the current and future reopenings. The markets were a little nervous at the beginning of the month due to inflation fears but the messages issued by the FED and the ECB seemed to convince investors. These two forces, monetary support and more vaccination, have been driving volatility lower over the FX, bond and equity asset classes and adding to the positive tone. Although supply constraints in the labour market and product chains will be the main causes of concern over the coming weeks and months, prospects of renewed budgetary support are making people optimistic about future growth.

Peace of mind

The world economy is improving and the manufacturing sector remains quite strong, with a global manufacturing PMI at 56. It also remains remarkably lean on inventories, with the inventory-to-sales ratio just catching up on future PMI output. Even Brazil reported a solid manufacturing PMI gain. Due to this strong manufacturing demand, the bottlenecks in the supply-chains have remained. However, commodity prices, notably raw materials prices, have slightly decreased.

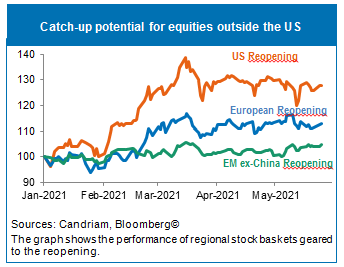

If investors are globally confident in achieving the vaccination campaign, there is an asymmetry between the most and the least populous countries. The Covax is the beginning of an answer and may benefit more from the help provided by the G7. At least Europe is benefiting from the reopening hopes, showing that the sequential move (depending on the vaccination pace) among countries globally is alive. European stocks have been the best performers in recent weeks due to the equity rotation toward cyclicals and value. Moreover, there is a growing confidence in Europe, owing to implementation of the NGEU, and as the German elections should not be a brake on European integration.

Some central banks (Canada, New Zealand, the UK, Norway) began to tighten their monetary policies but the main ones - the FED, the ECB and the BOJ - changed neither their minds nor their communication. They kept real yields low, whereas nominal bond yields have been moving in tight ranges, e.g., the 10-Year US Treasury Notes moved between 1.70% and 1.55%. Even the Italian 10Y yield reverted to its end-April level after climbing over 30bp. Some indicators in the US, such as that showing the very high spread between jobs plentiful minus jobs hard-to-get, are already pointing to a stronger labour market. When this materializes in the employment report, we may see higher real yields and nominal yields.

Our credo

The economic recovery should continue over the next year with continued fiscal support and prudent central banks. For the time being, the pandemic seems manageable, too, as the virus mutations are for the time being addressed by the vaccines. We believe that this context is positive for equities vs bonds. In the same way, the sequential current equity rotation may continue, helping non-US equities, which could benefit from new inflows.

Risks to the scenario

The main risk may be the supply-side constraints that have been persisting, i.e., not only the production chains but the labour market shortages, too. Many companies have warned about the difficulties they are experiencing hiring and building their inventories to meet the demand. That could bring more inflation without higher growth if it lasts too long and margins may tighten. In such an environment, markets could be more volatile. Another risk is a virus mutation that needs time to be faced. It could derail the reopening and induce an equity correction. Geopolitical tensions, too, linger. For the time being, they are not disruptive, as the oppositions are less outspoken, even if they are there.

Our current multi-asset strategy

We remain positive equity vs. bonds and, in our equity allocation, are keeping our strategy geared towards reflation trades that reflect the latest positive evolution in the economy. That includes being overweight European and Japanese equities, with a preference for small and mid-caps, an overweight in emerging equities and an increasing interest in Latin America (a laggard in the aftermath of the peak of the crisis), and overweights in US small and mid-caps and global banks (a sector that usually benefits from the increase in rates).

On the fixed-income side, we remain underweight government bonds. We also remain long commodities, which should still benefit from the catch-up in demand.