As the world economy continues to recover; since the vaccine announcement in early November, investors are positioning themselves for a re-opening of the economy and progressively rotating out of Work From Home-related investment themes. Inflation was expected to increase once social distancing measures had eased, due to strong consumer savings reserves in the US, accommodative central banks, additional liquidity injections into the economy and limited inventory and capacity for commodities, goods and services. However, the speed of the 10-year US Treasuries upward move surprised the market, leading to a significant sell-off of growth-oriented investments.

Equity markets – driven by the post-COVID narrative – performed well during the month. Indeed, small and mid-cap, cyclicals and value indices – led by economic recovery expectations and a pick-up in long-term interest rates – have outperformed the star indices of 2020. Sovereign debt yields remain very low but the 30bp increase in long-term Developed Market sovereign issues in just one month was enough to send shock waves across the financial planet. Commodities had a strong month, with prospects of limited offer and approaching higher demand.

The HFRX Global Hedge Fund EUR returned +1.48% during the month.

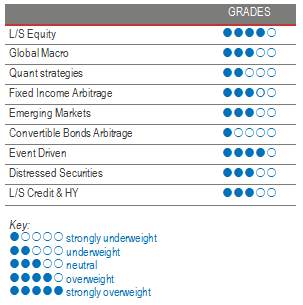

February was a strong month for Long Short Equity strategies. After starting 2021 with one of the poorest months in terms of alpha generation – partly due to the strong deleveraging that took place during the second half of January – Long Short Equity managers recovered those losses during in early February. Selection effect was the main performance contributor. Although most strategy styles made money during the month, fundamental stock-pickers strict on stock valuations were the stars, significantly outperforming core indices. The rise in long-term rates triggered an acceleration of the rotation from growth into value stocks. We cannot say if, after a decade of value-style underperformance, this recent move is temporary or the beginning of a new market phase. However, we can say that the steepening of the yield curve will make stock-picking of winners and losers more relevant and will make it much more difficult to default to the typical growth playbook that has worked so well over the past 10 years. During February, hedge funds were sellers of momentum and unprofitable/expensive technology in favour of industrials, energy, materials and financials. Long Short Equity remains an interesting investment opportunity for 2021. During last year’s market rebound, intra-sector correlations and cross-sector dispersion were high, generating many relative-value opportunities. Furthermore, managers can deploy capital into long and short investments across industries undergoing major reshuffling, like media, retail, mobility and energy. Long Short Equity as a strategy is very rich and diverse in terms of thematics and styles, and possesses several tools to face different market environments.

Global Macro

Global Macro managers’ performance was dispersed during the month but skewed towards a positive average return across the board. Some were surprised by the speed of the upward move on long-term US Treasuries and lost money on spread trades on the US yield curve, long Emerging Markets fixed income positions and short USD currency trades. Among the biggest winning trades, managers made money on long equity indices, relative-value trades on equity baskets or from being long commodities. We continue to favour discretionary opportunistic managers who can draw on their analytical skills and experience to generate profits from selective opportunities worldwide.

Quant strategies

Multi-Strategy Quants and Trend Followers did well during the month. While the latter benefited from the sell-off in bonds to make money shorting fixed income, the move up on sovereign issue yields triggered a rotation from high-growth equities to cyclicals that seems to have affected Statistical Arbitrage Equity funds. This category of funds was among the worst performers of the month, continuing a difficult performance cycle in which their models are having difficulties predicting equity moves based on stock patterns and correlations. Although February was better, in terms of performance, quantitative strategies remained on a rough path. Considering quantitative funds draw their edge from analysing huge volumes of past data points to define the strategy’s current positioning, it is understandable that they are having difficulties dealing with a totally unchartered economic environment. Short-term trend followers are a small subset of funds that managed to benefit from the different market phases, making money on the strong up-and-down market moves. Sophisticated multi-strategy quantitative funds also benefited from increased market volatility levels to generate interesting returns. Nonetheless, investors are, overall, disappointed with quantitative fund performances, as most algorithms are having difficulties dealing with the violent and rapid increase in market volatility and asset correlations.

Fixed Income Arbitrage

Since December, the yield curve has steepened and swap spreads – helped by higher US yields and the change in market dynamics – have widened. This latter makes US bonds cheaper than futures, increasing the opportunity set for the strategy. In Europe, the poor level of issuance has had the reverse effect (bonds are more expensive than futures) while swap spreads also widened. These recent changes, in terms of overall positioning from long duration to short, fuelled by inflation fear gaining momentum, have clearly improved the ecosystem of the strategy.

Emerging markets

It was a difficult month for fundamental investors in Emerging Markets, as the repricing of US rates brought forward the risk of taper tantrum. This may lead to a more cautious approach from managers to avoid higher levels of volatility in their portfolios. The level of the US dollar, which is an important metric for Emerging Markets, is currently determined by two opposing forces: a rise in interest rates and increasingly higher fiscal deficits. While this may lead to some short-term volatility, the fundamentals for Emerging Markets remain good, with the global economy recovering and with rising commodity prices that will help mitigate fiscal deficits from commodity-exporting nations. With a significant part of the global bond market in negative-yield territory, Emerging Markets are an appealing investing ground for investors seeking decent fixed income assets. However, the macro outlook remains foggy for EMs, which fundamental managers consider an interesting option in a zero-rate world. Considering the fragility of fundamentals, these managers usually adopt a very selective approach. Caution is required, due to the higher sensitivity of the asset class to investor flows and liquidity.

Risk arbitrage – Event-driven

Event Driven strategies had a good month of February, generating positive contributions from Merger Arbitrage and Special Situations. The volume of merger deals remains healthy and, as current deal spreads are still attractive, some managers are reducing the amount of capital allocated to Special Situation investments, which are more sensitive to the market direction, and increasing their allocations to merger deals. This allows managers to target an attractive return (while remaining relatively immune to equity-market beta) and to increase the resilience of their strategies. Merger-deal activity is expected to continue in the near future. Interest rates are low, corporations have cut costs and issued debt and equity not only to face the crisis, but also to be ready to snap up strategic assets. The activity is driven by the need to restructure in stressed sectors like energy and travel, the willingness for consolidation in healthcare, financials and telecom, and the need to adapt to today’s new reality by externally acquiring technologies that would take too much time or money to develop, like in the semiconductor space.

Distressed

Stressed and distressed strategies had a good start to the year. As prospects of the economy reopening improve, troubled assets are benefiting from the most recent wave of asset repricing. It is interesting to note that, during 2020, many distressed managers had above-average portfolio turnover levels. As the market dropped at the end of the 1st quarter, all assets – irrespective of their quality – crashed. The most successful managers were able to provide liquidity by buying discounted quality assets, which, as the year progressed, they sold at a profit to move into more stressed assets. As these assets have repriced significantly with the vaccine release news, some are starting to take profits and buying more valuable parts of the distressed market that will be able to rebound with the reopening of the economy. That is the current situation at the beginning of 2021. We favour experienced and diversified strategies to avoid having to face extreme volatility swings. It is not going to be easy but this is the environment and opportunity-set these managers have been waiting on for the last decade.

Long short credit & High yield

Credit spreads for investment-grade and high-yield markets reached extreme levels unseen since the crisis of 2008. The market was also highly affected by the lack of liquidity, prompting the ECB and the Fed to step up their IG debt-purchasing programmes. The Fed also decided to include high yield in its buying programmes to smooth the high amount of investment-grade fallen angels downgraded to high yield. Investment-grade and quality high-yield spreads in the US and Europe are now close to pre-COVID levels. News relating to the high level of efficiency of the Pfizer/ BioNTech and Moderna vaccines pushed credit spreads even lower, leading to an outperformance of riskier issues. Although the beta trade is behind us, we think that long short credit offers interesting opportunities on both long and short to capture the fundamental inconsistencies triggered by this year’s strong dislocations.