The economy is showing signs of muddling through. Data points are weak but strong consumer data in the US and accommodative central bank policies are keeping risk appetite at healthy levels. The uncertainties, so often discussed throughout the year, remain, but the general sentiment seems to be “Hope for the best!”.

November was another strong month for equities. Earnings were no worse than expected and macro fears receded. The Nasdaq Biotech was among the best-performing indices, returning a little more than 11%. The other developed market equity indices posted performances between 1.5% and 4%. Emerging Market equity returns were more challenging. The South African JSE Top 40 Index and the Hang Seng declined by close to 2%. Sector-wise, Information Technology and Healthcare led the way.

Long-term sovereign yields stabilised during the month, with the US 10-year Treasuries finishing the month 0.02% higher, at 1.82%.

Commodity markets were dispersed in November. Soft commodities saw futures prices appreciate, with coffee leading the pack (+16.40%). Industrial metals remained relatively muted, while Precious metals declined a little more than 3%.

The HFRX Global Hedge Fund EUR climbed +0.68% during the month.

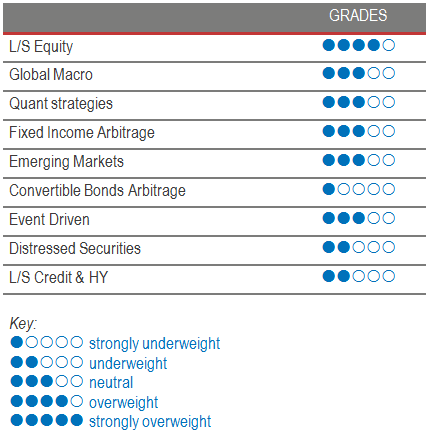

Long short equity

November was a strong month for most Long Short Equity strategies. Healthy equity markets have been a positive factor for managers. However, according to Prime Brokerage data, managers are generating alpha on both their long and short portfolios. We are currently on track for one of the best years, in terms of alpha, since 2014. Market Neutral Long Short Equity strategies, on the other hand, are having difficulties calibrating their portfolios to strong upward markets, and to sector and style rotations. The current environment is not easy, due to economic uncertainty and rapid sentiment changes. However, strong dislocations always create opportunities for either long or short investments. American equities in the healthcare sector are a good example of this. It would be a mistake to shun the sector as a whole because of politically driven volatility. Good managers will benefit from the current situation to build a balanced portfolio of long and short investment opportunities. This strategy offers a wide range of levers that can be used to benefit from industry restructurings and sector dispersion from a long or short perspective.

Global Macro

Performance among managers was dispersed during the month. On average, strategies with a focus on developed markets outperformed other subsets of the strategy, due to healthy equity market trends. Asia and Latin America remain choppy markets but seem to be gathering some consensus among investors as an investment opportunity for 2020. With developed market rates pointing to the bottom, EM high-yielding assets are again starting to become somewhat desirable. In this environment, we would tend to favour discretionary opportunistic managers that stay on the sidelines looking for asset price dislocations. These managers can use their analytical skill and experience to generate profits from a few strong opportunities worldwide.

Quant strategies

November was, on average, rather muted for CTAs, with the gains made on equities being balanced by losses on fixed income and commodities. The environment remains challenging for statiscal arbitrage strategies, due to unwinding factors. However, despite the factor reversal, the correlation between momentum, low volatility and quality versus value factors remains at extreme levels. Further reversal periods are to be expected.

Fixed Income Arbitrage

Last month, central banks making it clear that they would pause their dovish interest rate policy triggered a strong reversal both in the US and on European rate markets. Our managers were able to capture the spike in volatility, posting strong returns. However, this month has been more muted, in terms of interest rate volatility: managers have posted lower but positive returns. It is worth highlighting the positive convexity of the strategy, which has reacted very well to this sudden change in direction, with strong gains being made in US basis trading as well as in the JPY relative value sector.

Emerging markets

Emerging Markets are recovering from previous losses and benefiting from improving investor sentiment on a relative value analysis. The big picture still presents high levels of uncertainty, however, in a sluggish growth environment, EM assets remain interesting opportunities for investors hungry for yield. Furthermore, declining US rates are kicking down the road the problem of EM dollarized debt economies. Argentina is closely followed as a future indicator of EM investment attractiveness. It has not been an easy environment for EM strategies. Nevertheless, there are strong dislocation-generating opportunities for seasoned opportunistic managers.

Risk arbitrage - Event-driven

2019 has been an average year for Event Driven strategies, specially when compared to more directional strategies. Pure merger arbitrage strategy performances have been rather muted. Economic and political uncertainty had a negative impact on the volume of announced mergers & acquisitions. Nonetheless, the sustained level of large deals (over $20 billion) in 2019 is keeping it on track to be a solid year in terms of deals. We are optimistic about the opportunities for Risk Arbitrage due to a supportive business environment with benign financing conditions and the willingness of corporate management teams to fight for sources of business growth. Also, spreads for large deals are currently at interesting levels, due to an increasingly complex approval process, specifically in the US. It is also interesting to note that the increase in shareholder activism challenging announced deals is also helping to keep spreads wider. Finally, in countries like Japan, some managers are pointing out that corporate governance initiatives have led to several significant cross-shareholder unwinds over the past few months.

Distressed

Distressed strategies have not performed well this year. Performances were impacted not only by idiosyncratic situations like the bankruptcy of PG&E but also by the investors’ reluctance to bid for complex situations during times of high uncertainty. The 2019 recovery was accompanied at the same time by deteriorating sponsorship in the more complicated parts of the credit spectrum. CCC bonds in the US are now trading above a 1000bp spread. Should corporate bond default rates begin to rise over the next 2 years, a repricing of credit risk across the whole of the credit spectrum could well materialise. Managers are raising cash levels to keep dry powder, waiting to reload the portfolio with new issues hitting the distressed market. We are closely monitoring distressed managers, due to the potential of high expected returns, but remain broadly on the sidelines.

Long short credit & High Yield

Despite some more volatility, spreads – supported by the chase for yield – are still heading in the same direction. Hence we remain underweight, as there is limited-to-no-comfort in being short the credit market, where there is strong demand and the negative cost of carry is quite expensive.