European equities: In the tariffs turmoil

Since the last committee on March 11th, European markets have fallen sharply, due to Donald Trump’s announcements regarding US tariffs on April 2nd.

Since the last committee on March 11th, European markets have fallen sharply, due to Donald Trump’s announcements regarding US tariffs on April 2nd.

This has reversed the gains recorded since the start of the year, as European equities landed 6% below their level at the end of 2024 (as of April 7th). However, this is still a clear outperformance vs. US equities, notably fuelled by several positive European initiatives, such as the ReArm Europe programme and the stimulus plan unveiled by Germany’s likely incoming chancellor Friedrich Merz.

Defensive sectors have played their part

There was no clear performance dispersion between Large Caps and Small & Mid-caps. Value stocks fell slightly less than Growth stocks, although it was also a double-digit decline. Defensive sectors were more resilient than cyclical ones. Among defensive sectors, Utilities remained flat, which was the best performance across all sectors. The decline was relatively limited for Consumer Staples, and more pronounced for Energy and Healthcare. Within cyclical sectors, Consumer Discretionary was the worst performer, followed by Materials, Industrials and Financials. Real Estate resisted better, given the downward trend of European long-term rates.

IT stocks also decreased significantly, while Communication Services limited the damage, thanks to the resilience of the Telecom segment.

Earnings expectations & valuations

Given the tougher environment, revisions have become mostly negative on average. Only two sectors (out of eleven) have seen a majority of positive revisions (Financials and Communication Services).

However, the extent of the negative revisions was quite limited, as the earnings growth expected for 2025 remains solid (+6.2% vs 6.9% one month ago). Consensus expects this EPS growth to be driven by Real Estate, Healthcare, Consumer Discretionary and IT (with double-digit growth for each). Energy is the only sector with a negative EPS growth expected in 2025.

Since the last committee, European valuation multiples have remained stable with 12-month forward P/E of 14.4x, which remains well below US multiples (21.0x), despite their recent decrease. IT and Industrials remain the most expensive sectors (P/E of 26.2x and 20.1x, respectively) while Energy and Financials are still the cheapest (P/E of 8.9x and 10.3x, respectively).

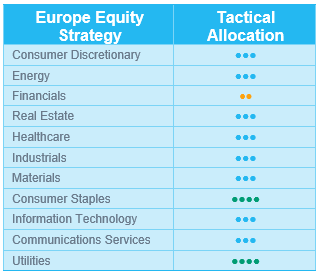

Selected recent Committee decisions

We have downgraded Healthcare (and Pharma sub-sector) to Neutral from +1 :

- Profit-taking on some large European pharma companies which have outperformed YTD.

- Approaching April 2nd and the announcement of tariffs and other regulations on Healthcare, we have preferred to be more neutral seeing a worse-case scenario is not discounted.

We have downgraded Insurance sub-sector to Neutral from +1 :

- Profit-taking after the strong outperformance YTD (around 10%): we are not comfortable with valuations of the largest insurance names (Allianz, Zurich Insurance, Munich Re, AXA). These four companies constitute over 60% of the weight in the MSCI Europe Insurance sector.

- We should not go Underweight given the strong momentum.

We have upgraded Utilities to +1 from Neutral :

- Upside potential from the new €500bn infrastructure plan for the names exposed to Germany.

- Limited tariffs impact.

- Attractive valuation (5-20% upside potential depending on the names).

- Positive technical analysis on heavyweights.

We have downgraded Financials (and Banks sub-sector) to -1 from Neutral :

- After an outperformance YTD, the sector is fully valued and relatively expensive amongst cyclical sectors.

- The sector is over-owned.

- Good trends on “Net Interest Income” could reverse in a scenario of global economic slowdown.

US equities: “America First” sends US equities south

US equity markets have experienced a significant sell-off in recent weeks, following Donald Trump’s import tariff announcements, which shocked investors. Policy uncertainty surged, the VIX Index spiked, and long-term interest rates fell, as markets grew increasingly concerned that US trade policy could trigger a global economic recession.

Low dispersion in a volatile market

US equities have undergone a significant correction in recent weeks, as investors grapple with the implications of Donald Trump’s trade policy. Markets are now trading more than 10% below their levels at the start of the year. Interestingly, performance dispersion across investment styles and sectors remained relatively limited during the sell-off.

As expected, defensive sectors such as Consumer Staples, Utilities, and Healthcare outperformed the broader market, but the difference with the broader market was rather limited given the increased volatility. In contrast, Information Technology and Communication Services faced sharp declines, while Materials and Energy also dropped amid mounting fears of a global economic slowdown.

Valuations compressed, but…

Following the sharp market correction, valuations have declined considerably. Just a few weeks ago, the S&P 500 was trading at 21 times forward earnings. Investors now pay less than 19 times expected earnings. As a result, the index has fallen below its 5-year average valuation, although it still trades above the 10-year average.

That said, valuation alone isn’t a compelling reason to rush back into US equities. Expected earnings growth over the next twelve months remains close to 12%, a figure that appears overly optimistic given the current environment. Further negative earnings revisions cannot be ruled out. The largest contributions to expected earnings growth come from the Information Technology, Communication Services, and Healthcare sectors. In the case of Healthcare, the comparison base is low, making growth easier to achieve. For IT and Communication Services, however, the bar is higher, and delivering upside surprises may prove more difficult.

Against this backdrop, President Trump holds the key to future market direction.

Comfortable with a balanced approach

In today’s rapidly evolving market environment, it is difficult to hold strong convictions. As a result, we believe a balanced approach is warranted. At this stage, we see no reason to make dramatic shifts in our sector allocation:

- Household & Personal Products: We maintain the overweight we adopted since the beginning of March. The subsector is driven by its defensive profile, coupled with companies that typically enjoy pricing power, and high consumer loyalty, and therefore continues to appeal. Valuations remain attractive. However, stock selection is key within the space.

- Industrials: We also maintain our positive view on Industrials. The sector held up well during the recent market turmoil and stands to benefit from ongoing reshoring trends in the wake of the US-China trade conflict instigated by President Trump.

- Healthcare: Our positive rating on Healthcare, upgraded in early February, has been rewarding. The sector continues to offer a favourable earnings outlook and appealing valuations. While the threat of pharmaceutical tariffs still looms, Healthcare does not appear to be a top priority for the Trump administration. This is evidenced by recent decisions to increase Medicare reimbursements. Moreover, biopharmaceutical companies - with their high gross margins - are relatively well-positioned to absorb potential tariff impacts.

- Information technology: For now, we believe it is too early to re-engage in US technology. While valuations have become more attractive, the sector remains vulnerable to potential downward earnings revisions.

- Real Estate: Finally, we upgraded Real Estate from underweight to neutral. With interest rates trending lower, the sector is less likely to underperform in a “hard Trump” scenario.

Emerging equities: Standout performance from China

March 2025 was a dynamic month for Emerging Markets (+0.4% in USD), characterised by volatility but ultimately positive absolute returns, outperforming Developed Markets (-4.6%). The Fed was on a critical position evaluating rate cuts, while uncertainties lingered for the fragile negotiations on the Ukraine war.

China (+2.0%) remained a focal point for investors, with its equity market continuing to rise, particularly in sectors linked to AI and semiconductors, as well as EVs. Although the government maintained a disciplined approach to economic stimulus, investor confidence improved further, keeping the uptrend intact.

India (+9.2%) was among the best performers in March. The central bank was reactive with effective measures such as liquidity injection. Most of the sectors delivered positive performance, benefiting from the coming-back of foreign inflows.

The LatAm (+4.3%) recovery continued, with Brazil and Mexico benefiting from strong commodity prices and renewed optimism around political and economic reforms. Emerging Europe continued to benefit from geopolitical optimism for a ceasefire in Ukraine and investments that would reignite growth in the region. Several countries rose strongly, including Czech Republic (+14.7%), Greece (+10%), and Poland (+7.3%). Turkey (-6.7%), however, was impacted by renewed political instability.

Regarding commodities, Crude increased by +2%, and metals saw a further increase with gold up by 9.3% and copper up by 11.5%. US 10Y yields finished the month at 4.23%.

Outlook and drivers

In 2025, geopolitics are more important than ever, re-shaping the global economy. The Trump administration’s worldwide tariffs solidified its stance on protectionism. Despite the potential space for negotiations, the act strains US relations with both allies and rivals.

The Chinese market is peaking, as the previous catalysts are priced in. The market already holds high expectations for China’s tech initiatives (AI, autonomous driving, robotics); stimulus and earning results are in line with expectations. Meanwhile, China announced a significant escalation in its trade policy, imposing a 34% tariff on all US imports, prompting a more cautious stance on China in the short term. We remain vigilant about China potentially stimulating its market to counteract these pressures. We also expect to see more collaboration between China and trade partners outside the US. But the economic and equity outlook could remain under stress for some time.

Within AI, US chip leaders face mounting headwinds, with deteriorating outlooks compounded by broader market weakness. The sector is oversold but opportunities are starting to arise. Emerging Markets companies with significant US exposure have similarly struggled. In contrast, China’s AI ecosystem is advancing rapidly. DeepSeek has emerged as the world’s fastest-growing AI tool, surpassing OpenAI’s ChatGPT in monthly new site visits. With AI now an official priority in government spending, the sector is poised for accelerated growth in China.

Amid heightened market volatility, a reactive, selective, and flexible investment approach is essential. The portfolio leverages its strengths to dynamically adjust risk exposure, capitalize on macroeconomic shifts, and position itself in high-conviction structural themes for the long term.

POSITIONING UPDATE

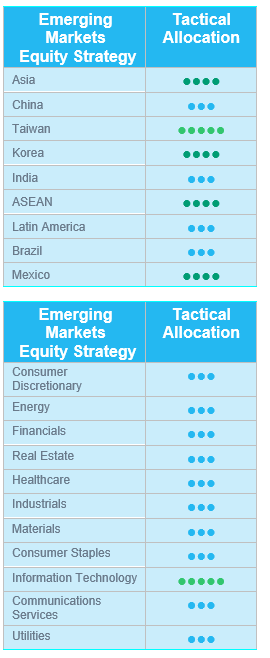

Visibility is limited due to ongoing volatility with growing tactical trading. We raised China’s rating from UW to Neutral for the reasonable valuations and the acceleration of regional partnerships outside the US. We raised Taiwan and Korea for a potential turning point following Trump’s new announcement on suspended tariffs. Consequently, we raised the OW Technology further, as both countries are heavily exposed to the sector. We also raised Energy and Materials from UW to Neutral, as global growth expectations can potentially find a bottoming point.

Regions

China raised to Neutral

China’s rating has been raised to Neutral from UW following a 15% market correction, which reversed prior gains and brought valuations back to more attractive levels (10x). While sentiment remains weak, expectations of stimulus, especially ahead of the upcoming Politburo meeting, are building. Early signs of policy support, including currency easing and state-backed market interventions, have also emerged. With much of the earlier rally unwound and bearish sentiment priced in, a Neutral rating is reasonable.

Taiwan raised from +1 to +2; Korea raised from UW to Neutral

Taiwan and Korea, both with heavy tech exposure, have been disproportionately impacted by Donald Trump’s trade initiatives, leading to significant volatility and oversold conditions. Recent signals of tariff relief from Trump mark a potential turning point, laying the groundwork for a strong rebound. Korean tech giants like Samsung Electronics and SK Hynix stand to benefit meaningfully, along with Korean auto OEMs, which are directly tied to tariff negotiations. Valuations across the region are compelling following broad deleveraging and position unwinds.

India remains Neutral

India remains a more defensive market. India’s $50bn trade deficit is not significant, and key export sectors like electronics, pharma, and textiles are relatively insulated (with pharma currently exempt). The government has maintained a more conciliatory tone toward the US, which may help ease tensions. Meanwhile, valuations still remain elevated at 21x versus a 20-year average of 17x.

Emerging Europe

Mostly financials in the region. Time to take profits after a strong rally this year.

LatAm Neutral

LatAm has not been significantly affected by US tariffs, making the region a possible short-term safe haven. Argentina has already secured a free trade agreement with the US, while Mexico has performed well and remains outside current tariff discussions. Weak commodity prices and LatAm’s high beta & high risk profile require caution.

Sectors

Consumer Discretionary & Communication Services: Neutral

Consumer Discretionary and Communication Services were downgraded to UW intra-month to reflect the possible aftermath of the escalating geopolitical pressure on China. A bottoming point can help improve the performance of related companies in the sectors such as Alibaba, Tencent, BYD, Meituan etc.

Technology upgraded from +1 to +2

The Technology sector is upgraded to reflect the relief of tariffs pressure on Taiwan and Korea. Both countries are heavily weighted in the sector, and work closely with the US chip leaders. Company examples include Samsung Electronics, Delta, and Quanta in Tech Hardware, and TSMC, Hynix, and Mediatek in Semiconductors.

Energy & Materials: Neutral

Both sectors faced the risks of global growth slowdown. The conjunction can rewind with the new bottoming signs.