Below their relatively calm surface, the equity markets remained rather turbulent, driven by investors rotating out of defensives and into cyclical sectors. The US remains path for a firm economic recovery. Joe Biden is pushing ahead with his infrastructure plan and Jay Powell has reiterated that monetary policy will remain accommodating. These “show me the money” policies are driving inflation outlook and US long term rates upwards. The steepening of the Treasuries yield curve contributed towards the rotation out of growth stocks and into cyclicals and value stocks.

Equity markets returned strong overall performances. European equity indices benefited from a higher level of exposure to cyclicals and value stocks and outperformed, posting high single-digit returns. Chinese and Hong Kong equities were among the worst performers. The unwinding of a family office holding massive positions in Chinese equities contributed towards triggering significant deleveraging among these securities.

Sovereign issues and corporate investment grade underperformed lower quality credit issues which are more sensitive to yield curve moves. Longer-dated US Treasuries rose by around 30 bps during period. The US dollar appreciated vs most global currencies.

The HFRX Global Hedge Fund EUR index returned -0.18% during the month.

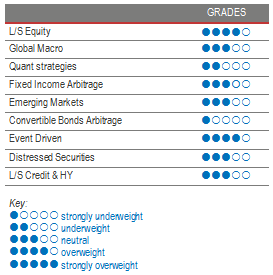

Long Short Equity

Diversified long short equity indices were positive during the month but performances were dispersed across the different styles and sector specific themes. Market rotation from growth stock into value stocks had a negative impact on strategies with a strong style bias. Growth oriented managers underperformed on their long books, while funds with exposure to cyclicals and value stocks were impacted by their short book. This was particularly true for managers running low net exposure. On the other hand, strategies that are very strict on securities valuations and fundamentals outperformed, as their short positions among overvalued growth stocks proved highly profitable. Contrary to early this year, the deleveraging triggered by the unwinding of the Archegos family office impacted only a small subset of securities and had an otherwise positive impact on hedge fund performances, since these funds were mainly short of the securities being sold in the market. Alpha generation has been a challenge during the first quarter due to relatively low intra-sector dispersion and strong inter-sector rotations. We believe the situation will improve going forward with the market presenting medium-term price distortion within overcrowded or overlooked sectors, but also through long-term opportunities within sectors and industries undergoing structural changes. We cannot say whether, after a decade of value stocks underperforming, this recent move is temporary or the beginning of a new market phase. However, we can say that the steepening of the yield curve will make stock-picking among winners and losers more relevant and will make it much more difficult to default to the typical growth playbook that has worked so well over the past ten years. Long short equity as a strategy is very rich and diverse in terms of themes and styles, and possesses several tools to face different market environments.

Global Macro

March was a challenging month for global macro managers. Discretionary managers did not manage to balance losses in foreign exchange and interest rates with gains in equities. As always, moves in the US yield curve have important repercussions on emerging markets. Managers held receiving positions in Brazilian rates as yields moved up. Long positions in Turkish lira also weighed heavily on global macro funds. We continue to favour discretionary opportunistic managers who can draw on their analytical skills and experience to generate profits from selective opportunities worldwide.

Quant strategies

March was a decent month for quantitative strategies. While trend models tended to be flat to slightly negative, equity statistical arbitrage models contributed significantly positively to returns. The returns achieved by quantitative strategies during the first quarter of 2021 have significantly improved on 2020 performances. Sophisticated multi-strategy funds remain better positioned to navigate through different market environments and post steady returns as they are less dependent on a specific model. Overall, investors remain relatively disappointed with quantitative fund performances as many algorithms, which draw their edge from analysing huge volumes of past data points, in order to define the strategy’s current positioning, have difficulties dealing with the brutal and rapid increase in market volatility and asset correlations.

Fixed Income Arbitrage

Since December, the yield curve has steepened driven by increasing US-fuelled by inflationary fears. More recently the expiry of the temporary exclusion of Treasuries from the Supplementary Leverage Ratio (SLR) calculation has triggered a sharp tightening of swap spreads due to net bonds sellers, despite cheap financing. Inexpensive funding means that US bonds are cheaper than futures, increasing the opportunity set for the strategy. In Europe, the low level of issuance has had the reverse effect (bonds are more expensive than futures) while swap spreads also widened. These recent changes, in terms of overall positioning from long duration to short, fuelled by inflation fears gaining momentum, have clearly improved the ecosystem of the strategy.

Emerging markets

It was a difficult month for fundamental investors in emerging markets, as the repricing of US rates brought forward the risk of taper tantrum. This may lead to a more cautious approach from managers seeking to avoid higher levels of volatility in their portfolios. The level of the US dollar, which is an important gauge for emerging markets, is currently determined by two opposing forces: a rise in interest rates and increasingly higher fiscal deficits. With a significant part of the global bond market in negative-yield territory, emerging markets are an appealing investing ground for investors seeking decent fixed-income assets. Although EM fundamental managers believe that their investment universe is an interesting option in a zero-rate world, they usually adopt a highly selective approach given the fragility of fundamentals. Caution is required, due to the higher sensitivity of the asset class to investor flows and liquidity.

Risk arbitrage – Event-driven

The volume of merger deals remains healthy and, as current deal spreads are still attractive, some managers are reducing the amount of capital allocated to special situation investments, which are more sensitive to market trends, and increasing their allocations to merger deals. This allows managers to target an attractive return (while remaining relatively immune to equity-market beta) and to increase the resilience of their strategies. Merger-deal activity is expected to continue in the near future. Interest rates, although rising, remain low in absolute terms, corporations have cut costs and issued debt and equity not only to face the crisis, but also to be ready to snap up strategic assets. The activity is driven by the need to restructure in stressed sectors like energy and travel, along with consolidation appetite in healthcare, financials and telecoms, and the need to adapt to today’s new reality by bolting-on technologies that would take too much time or money to develop, like in the semiconductor space.

Distressed

Stressed and distressed strategies had a good start to the year, as lower quality credit issues have outperformed sovereign and investment grade issues. As the prospect of the economy reopening improves, distressed assets are benefiting from the most recent wave of asset repricing. It is interesting to note that, during 2020, many distressed managers had above-average portfolio turnover levels. As the market dropped at the end of the first quarter, all assets crashed, irrespective of their quality. The most successful managers were able to provide liquidity by buying discounted quality assets, which, as the year progressed, they then sold at a profit to move into more stressed assets. As these assets have repriced significantly with the vaccine rollout news, some are starting to take profits and buying more valuable parts of the distressed market that will be able to succeed with the reopening of the economy. This is the current situation at the beginning of 2021. We favour experienced and diversified strategies to avoid having to face extreme volatility swings. Although it is not going to be easy, this is the environment and opportunity-set that these managers have been anticipating for the last decade.

Long short credit & High yield

Credit spreads for investment-grade and high-yield markets reached extreme levels unseen since the crisis of 2008. The market was also highly affected by the lack of liquidity, prompting the ECB and the Fed to step up their IG debt-purchasing programmes. The Fed also decided to include high yield in its repurchase programmes in order to mitigate the high number of downgrades in investment-grade fallen angels to a high yield rating. Investment-grade and quality high-yield spreads in the US and Europe are now close to pre-COVID levels. News relating to the high level of efficiency of the Pfizer/ BioNTech and Moderna vaccines narrowed credit spreads even further, causing riskier issues to outperform. Although the beta trade is behind us, we think that long short credit offers interesting opportunities on both the long and the short side to capture the fundamental inconsistencies triggered by strong market distortion this year.