Diversify Your Portfolio Through the Commodity

As Donald Trump returns to White House, his policy agenda could send ripples through the global oil market. His trade wars and immigration stance are expected to fuel inflation, while his commitment to deregulation and to increasing US oil production pose new challenges for oil prices. The interplay among these policies and broader geopolitical and economic factors could redefine the energy landscape. Despite challenges, the oil and gas sector is adapting effectively to a shifting landscape, balancing operational efficiency with financial discipline to navigate heightened uncertainty. What does this mean for investors?

Tensions Amid Slower Oil Demand Growth in 2025

Global oil demand is expected to grow slightly in 2025, increasing by around 1 million barrels per day to 103.8 mbd, according to the International Energy Agency (IEA). This slower growth reflects weaker economic conditions, the waning of post-pandemic recovery, and the shift toward cleaner energy. Demand from China, a key driver of growth in recent years, is also expected to level off.

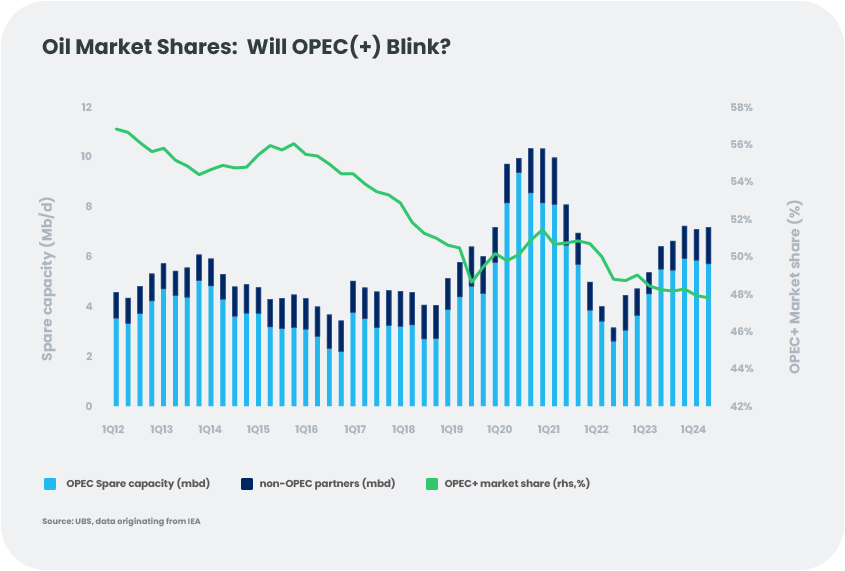

Meanwhile, on the supply side, OPEC+ will have to deal with non-OPEC members [1] who are expected to increase their output by 1.5 mbd, driven by offshore projects. To maintain market equilibrium, OPEC+ may need to cut its annual crude production by 0.6 mbd, in contrast to its hope to restore 2.2 mbd of previous voluntary cuts. In early December 2024, OPEC adjusted to the rapid return of Libyan production and other pressures by postponing this 2.2 mbd restoration, along with other changes.[2] We remain sceptical, as we see room for OPEC+ to raise production in 2025. Balancing supply and demand will require careful coordination among OPEC+ members. A lot will also depend on Saudi Arabia, the largest producer among OPEC+, which might decide to repeat its 2015 strategy of prioritizing market share over price stability. This decision comes as global oil demand is expected to peak by the end of the decade and decline further by 2035.[3] However, such a move would strain Saudi Arabia’s budget—requiring oil prices around $93 per barrel to fund its investments—and could weaken its influence within OPEC+. Plenty to this story to hold our interest!

Risks in 2025: Balancing Fundamentals, Politics, and Risk

In 2025, oil prices face both downside and upside risks, influenced by geopolitical, economic, and policy factors.

US Policies Under Trump: A potential Trump presidency could impose new and higher tariffs, reduce corporate taxes, and roll back regulations, especially environmental regulations. His trade wars and immigration stance are expected to fuel inflation, while his commitment to deregulation and increasing US oil production poses new challenges for oil prices.

Inflation could rise due to tariffs or restrictive immigration policies. For example, our economists estimate that tariffs on products from Canada, Mexico and China could add 1% to US inflation. To offset such pressures, Trump could push for lower oil prices, ideally around $40 per barrel. However, this price level is unsustainable for US shale, which needs $70 per barrel to maintain growth. Another complication is Trump’s focus on Iran and Venezuela. Secondary sanctions could create upward pressure on global prices.

Middle East Tensions: Geopolitical risks in the Middle East remain a potential upside for oil prices. While conflicts between Israel and Iran have yet to impact oil flows or infrastructure significantly, any escalation could change this dynamic. Alternatively, Trump might prioritize easing tensions, given his history with the Abraham Accords and interest in fostering deals in the region.

Overall, we expect Brent crude prices to average around $70 per barrel in 2025 -- slightly above current market expectations but below the cost of many new oil projects. Depending on how these risks unfold, prices could range between $50 and $80 per barrel, a broad range because of the many risks.

Energy Sector Outlook: Navigating Volatility and Adapting Strategies

Equity Outlook:

The oil and gas sector faces earnings pressure due to global overcapacity, but downside risks appear limited. Companies are adapting by cutting capital investments and adjusting share buyback programs. Recent declines in share prices have improved the sector’s relative value, with integrated oil companies pricing in Brent crude at $60-65 per barrel -- ie, below the forward price curve. Meanwhile, the liquid national gas market is expected to remain tight until new projects come online in 2026, benefiting gas-focused companies and improving the resilience of the sector, despite near-term risks to earnings momentum. Therefore, considering the already negative sentiment, we are neutral on the equities in the energy sector.

Credit Outlook:

US high-yield energy industry bonds face a slightly higher risk profile in 2025 compared to 2024, although company fundamentals. Firms are maintaining low leverage, solid coverage ratios, high credit ratings, and strong liquidity, with minimal reliance on Reserve-Based Lending Facilities. If oil prices were to fall further, the sector could experience a valuation reset, however, we would not expect a significant increase in defaults.

Conclusion: Diversify Into the Real Thing

The oil market in 2025 will continue to be shaped by a complex mix of supply-demand dynamics, geopolitical tensions, and policy choices. Overcapacity, coupled with the Trump administration’s push to keep energy prices low, casts doubt on the effectiveness of OPEC+’s price-defence strategy. However, the high-cost structure of US shale oil acts as a natural floor, limiting how far prices can fall.

The outlook for the oil equity, and credit sectors remains subdued, but the environment highlights the value of commodities as portfolio diversifiers. Even with expectations of weaker oil prices, a long position in oil could serve as a hedge against geopolitical risks, offering some protection.

[1][ OPEC (Organisation of Petroleum Exporting Countries) currently includes 12 member countries (Founder Members, and Full Members): Iran, Iraq, Kuwait, Saudi Arabia, Venezuela, Libya, the United Arab Emirates, Algeria, Nigeria, Gabon, Equatorial Guinea, and Congo. Since 2016, OPEC+ includes ten so-called ‘non-members’, as shown in the Figure, namely Azerbaijan, Bahrain, Brunei, Kazakhstan, Malaysia, Mexico, Oman, Russia, South Sudan, and Sudan.

[2] IEA Oil Market Report, November 2024.

[3] IEA Oil 2024 Analysis and forecast to 2030.

-

Outlook 2025, Nadège Dufossé

Outlook 2025, Nadège DufosséAsset Allocation in 2025: Between Optimism and Uncertainties

Global growth progresses in line with expectations, but the economic landscape remains fragmented. While activity is strong in the United States, the Eurozone is struggling to move forward, and China is penalised by weak consumption. Geopolitical tensions and the rise of political uncertainty in several countries risk exacerbating these divergences in 2025. -

Outlook 2025, Steeve Brument, Bertrand Dardenne

Outlook 2025, Steeve Brument, Bertrand DardenneM&A: Triple Trends for 2025?

As we head into 2025, the stars seem to be aligning for a revival of mergers and acquisitions, creating a fertile environment for investors seeking new opportunities. Merger arbitrage strategies attempt to capitalize on M&A activity by using a structured approach returns. -

Outlook 2025, Alix Chosson, Tanguy Cornet

Outlook 2025, Alix Chosson, Tanguy Cornet2025: the swan song for global climate action?

2024 concluded as another annus horribilis for climate action, with COP29 blowing “hot air”, reinforced geopolitical tensions overshadowing the climate crisis, and the re-election of Donald Trump in the U.S. We only have a couple of years left before spending the totality of the +1.5°C carbon budget. How will the recent political changes and global geopolitical tensions impact the transition? -

Outlook 2025, Christopher Mey, Paulo Salazar

Outlook 2025, Christopher Mey, Paulo SalazarIs China ready for another Trump fight?

With Donald Trump returning to the White House in 2025, his second term is likely to see a resurgence of tariffs and export restrictions among other things, raising concerns about China's ability to withstand a resurgence of 'America First' policies. -

Outlook 2025, Thibaut Dorlet, Nicolas Rutsaert, Nicolas Cleris

Outlook 2025, Thibaut Dorlet, Nicolas Rutsaert, Nicolas ClerisDiversify Your Portfolio Through the Commodity

As Donald Trump returns to White House, his policy agenda could send ripples through the global oil market. His trade wars and immigration stance are expected to fuel inflation, while his commitment to deregulation and to increasing US oil production pose new challenges for oil prices. -

Johan Van der Biest, Vincent Compiègne, Alfred Sandeman, Outlook 2025

Johan Van der Biest, Vincent Compiègne, Alfred Sandeman, Outlook 2025Hello ChatGPT: Will AI continue to surprise the world?

If investors are expected to be early in detecting future trends, then our community certainly thinks AI is the future. Will the surprises continue? To help train ChatGPT’s response, we analyse the tangible revenue that has emerged so far, and consider the ‘sweet spot’, the ‘runners-up’ and the ‘too early’. -

Christian Solé, Thomas Madesclaire, Lucia Meloni, Outlook 2025

Christian Solé, Thomas Madesclaire, Lucia Meloni, Outlook 2025The 2025 European Banking Puzzle: Risks, Rewards, and Regulation

Conflicting or competing regulatory regimes on both sides of the Atlantic, a changing rates environment with central banks in easing mode, and consolidation are the new trends to watch in the European banking sector as we head into 2025. Select carefully and keep an eye on the emissions. -

Lucie Hamadache, Christian Solé, Rémi Savage, Outlook 2025

Lucie Hamadache, Christian Solé, Rémi Savage, Outlook 2025A New Dawn for European Real Estate? Navigating a Path to Recovery

While easing interest rate pressure may bring some relief to the European property market, some challenges remain, making selectivity crucial in navigating today's uncertain environment.