It was a month rich in major events that will shape our lives for years to come. Although the election of a new president in the United States is very important, we can agree that the positive news announced by Pfizer-BioNTech and Moderna will have an even bigger impact on our lives going forward.

It was a month rich in major events that will shape our lives for years to come. Although the election of a new president in the United States is very important, we can agree that the positive news announced by Pfizer-BioNTech and Moderna will have an even bigger impact on our lives going forward.

Although there are still many unknowns regarding the vaccine – such as long-term safety features, eventual side effects or the duration of the immunity – the market reacted very positively to this announcement, leading equity markets to one of their best monthly performances ever. Equity indices representing Southern European markets, small-cap companies and Emerging Markets outperformed Technology and large-cap indices. At a sector level, cyclicals had their shining moment.

Fixed income asset returns were dispersed as credit issues from businesses suffering from social distancing measures and with lower quality ratings benefited from the strong spread compression. Commodities also had a strong month, with a big majority of listed futures increasing by a double-digit percentage. WTI oil increased +27% but remains down -26% since the start of the year.

The HFRX Global Hedge Fund EUR returned +2.72% during the month.

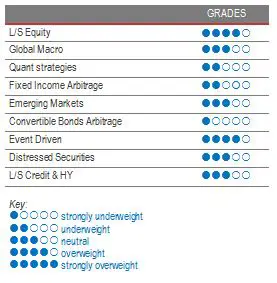

Long Short Equity

November was a very strong month for most long-short equity strategies in terms of absolute return but, due to the strong equity market performance, it was a very poor one in terms of alpha generation. Directional and fundamental long-short strategies delivered, on average, very good results during the month but nothing close to the returns generated by value-style funds, which returned, on average, high double-digit figures. Although value long-short funds will be happy to top the charts for once, they are still, on average, in negative territory for the year. Market-neutral funds and systematic strategies lagged the universe, affected, as they were, by negative alpha generation on their short books. Long-short equity as a strategy is very rich and diverse, in terms of styles, and possesses several tools to face varied market environments.

Global Macro

Global macro indices, although overall positive, captured limited market upside. Global macro commodity indices, on average, declined during November. Their significant commodity books were negatively affected by their short oil positions, which rallied strongly after the vaccine-news release. Short equity indices and short Emerging Market currencies were also performance detractors. Long equities seems to be a consensual trade for 2021 but most managers are well aware that it is usually the time to worry when everyone is on the same trade. Prime broker surveys indicate that risk deployment is low for the moment and funds have a low propensity to take risk going into year-end. In this sentiment-driven environment, we continue to favour discretionary opportunistic fund managers who can draw on their analytical skills and experience to generate profits from selective opportunities worldwide. The stabilisation of the market and increased visibility in macro-economic data should lead to better performances from systematic strategies with expected lower realized volatility levels than the more concentrated discretionary managers.

Quant strategies

Performances were dispersed for quantitative strategies. Trend models performed well, with managers generating positive returns from long positions in equity indices and Emerging Market currencies, and long futures contracts in metals and soft commodities. Statistical arbitrage strategies had difficulties dealing with two strong style rotations during the month. Early November, after the US elections, they saw one of the strongest value-to-growth rotations. Then, following the vaccines announcement, there was one of the strongest rotations from growth to value assets in recent history. Performances from multi-strategy funds were dispersed, with their aggregate performance depending on the speed of trading and the type of model with the highest allocations. 2020 was definitely not a good vintage for quants. Throughout the year, models had difficulties dealing with the violent and rapid increase in market volatility and asset correlations.

Fixed Income Arbitrage

Since March 2020, and its historical level of dislocation, volatility across G3 interest rates has collapsed on the back of clear central bank rhetoric in favour of stability to fight the economic slowdown triggered by the pandemic. Hence there have been fewer opportunities in that field over the last three months. However, the “low-rate environment” offers a very compelling opportunity if US growth accelerates and, with the help of the vaccine, the situation normalizes.

Emerging markets

India and Latin America – benefiting from the risk-on environment and from “the buying the lagers trade” – were strong performers in November. Emerging Market debt denominated in dollars or in local currencies have recovered this year’s losses and are at all-time highs for dollar-denominated issues and 1% below pre-COVID levels for local currency-denominated debt. Emerging Market debt denominated in local currency has returned around 5% since the end of September 2020, with 80% of the return coming from currency appreciation of currencies said to be oversold, like the Mexican peso, the South African rand and the Russian rouble. The value of the US dollar is always an important topic in Emerging Market investing. Some analysts believe that low Treasury rates and more political stability in the US will push investors to seek higher yields in Emerging Markets, putting a downward slant on dollar cross-exchange rates. The macro outlook remains extremely foggy for Emerging Markets, however. Fundamental managers are stressing that, in a zero-rate world, Emerging Markets is the only alternative to invest in yielding fixed income. Considering the fragility of fundamentals, they usually adopt a very selective approach. Caution is required, due to the higher sensitivity of the asset class to investor flows and liquidity.

Risk arbitrage – Event-driven

November was a very strong month for Event-Driven strategies. Merger arbitrage strategies benefited from spread-tightening in several pre-COVID deals like Taubman/Simon Property and Transat/Air Canada. Merger deal activity remained solid during the month, a state of affairs expected to continue into the near future. The activity is driven by the need for restructuring in stressed sectors like energy and travel, the willingness for consolidation in healthcare, financials and telecom, and the need to adapt to today’s new reality by externally acquiring technologies that would take too much time or money to develop as, for example, in the semiconductor space. One of the most significant deals announced during the month was the agreement for an all-stock merger between S&P Global and HIS Markit. Another strong driver of performance for Event-Driven was the special situations book. These are usually long investments with a strong value tilt that have benefited from the positive news on vaccines. As we progress towards a healthcare solution for this crisis, Event-Driven will have many opportunities to deploy capital as corporations adapt and restructure to this new reality.

Distressed

Stressed and distressed strategies, benefiting from a strong spread compression of the riskier issues and from the price recovery of assets related to the businesses most exposed to social distancing measures, performed well during the month. The market seems to have priced in a “the-sanitary-crisis-is-over” moment. However, over the year, the opportunity-set in distressed had more to deal with from distressed sellers than from distressed assets. Complex and less liquid instruments sold off and are yet to recover to pre-crisis levels. Effective defaults will probably be below the default expectations estimated during 2Q but we are still far from a return to normality. While the UK and the US are starting to distribute the first rounds of vaccines to their populations, other regions, like Europe, seem to be ready to do so only by the end of 2020. We favour experienced and diversified strategies to avoid having to face extreme volatility swings. It is not going to be easy but this is the environment and opportunity-set these managers have been waiting for over the last decade.

Long short credit & High yield

Credit spreads for Investment-Grade and High-Yield markets reached extreme levels unseen since the crisis of 2008. The market was also highly affected by the lack of liquidity, prompting the ECB and the Fed to step up their IG debt-purchasing programmes. The Fed also decided to include high yield in its buying programmes to smooth the high amount of investment-grade fallen angels downgraded to high yield. Investment-grade and quality high-yield spreads in the US and Europe are now close to pre-COVID levels. News relating to the high level of efficiency for the Pfizer/BioNTech and Moderna vaccines pushed credit spreads even lower, leading to an outperformance of riskier issues. Nonetheless, there is still a wide dispersion across sector spreads relative to their pre-COVID levels. Although beta trading is behind us, we think that long-short credit offers interesting opportunities on both long and short to capture fundamental inconsistencies triggered by this year’s strong dislocations.