Alternative Investments, Fixed Income, Private Debt, Private Assets, Real Estate, Research Paper

Real Estate Private Debt: Time to Act?

Has commercial real estate reached its inflection point?

When companies borrow money, we generally think of them borrowing from a bank or issuing bonds which are traded in public markets. In its simplest form, private debt means that investors make loans directly to the corporate borrowers, bypassing the banks and the public bond markets. Most of these private borrowers do not issue public equity; their ownership is held privately by the founders, senior employees, and possibly private equity investors.

Investors say[1] their top reasons for including private debt in their portfolio are diversification, reducing portfolio volatility, a reliable income stream, and risk-adjusted return. (The same recent survey lists their greatest concern, by far, as interest rates.)

The cash flows for private debt are more predictable than for many other alternative investment types such as private equity or commodities, as the loans typically make specified, periodic interest payments and the principal is returned on a specific pre-agreed date, as for any other debt. No need for the founders to decide when they wish to sell, as is usually the case for cashing our private equity investments.

It has historically been easier for banks to lend to larger, better-known borrowers. These types of corporate borrowers are typically listed on the equity markets, publish standardised financial statements, are likely to carry debt ratings from the major credit-rating agencies, and often have long operating histories, all of which comfort the bankers and the bank regulators. Compared to large borrowers, more work is required to analyse the creditworthiness of small- and mid-sized enterprises (SMEs), which are likely to be young, growing companies, and often do not yet issue public debt or equity.

Since the Great Financial Crisis, regulators have required banks to hold increasingly large amounts of capital as a proportion of the loans they make. This reduces the profitability to banks for all lending, and even more so when lending to SMEs. Let’s not forget that during the days when interest rates were barely above zero, and during the era of ‘lower-for-longer’ rates, banks could ill afford to make these types of loans.

In contrast to banks, the return can be greater for investors who lend directly, especially when their loan investments are part of a more diversified set of investment types. And direct investors can manage their risks through the support of specialist managers who are experienced at analysing individual SMEs and their ability to meet interest payments and pay back their loans. Candriam’s partner Kartesia is one such specialist.

There are many instances in which firms could tap, but do not wish to use, either the public markets or banks. One reason may be that they do not wish to produce publicly-available financials. Another may be that they wish to keep their ownership closely held and not to dilute the interest of the founders and early equity investors. Also, they may wish to have more customised conditions than are typical either with banks or public debt markets. These can be tailored to be in the interest of both borrow and lender, as fewer parties are involved.

Corporations can borrow from banks or by issuing public bonds in a number of ways, ranging from the most secure to the lenders through a of less-senior and higher-rate portions of their balance sheet and capital structure. For example, corporate secured debt in which manufacturing assets are pledged as collateral like a mortgage; senior unsecured debt, the most similar to a vanilla bank loan, down through subordinated or mezzanine debt which would be paid later in event of a default but pay commensurately higher interest rates. Corporates which borrow directly offer the same sorts of debt to private invests. These different types can also be packaged together, in blends of senior and subordinated/mezzanine debt, or even including some equity within a package of debt investments.

With the new ELTIF[2] investment framework in Europe, long-term investments are now available to individual investors. To qualify, investors must be able to invest a portion[3] of their savings in illiquid assets and understand that the investment will be for a number of years, in return for a steady expected income of a lump sum at the end.

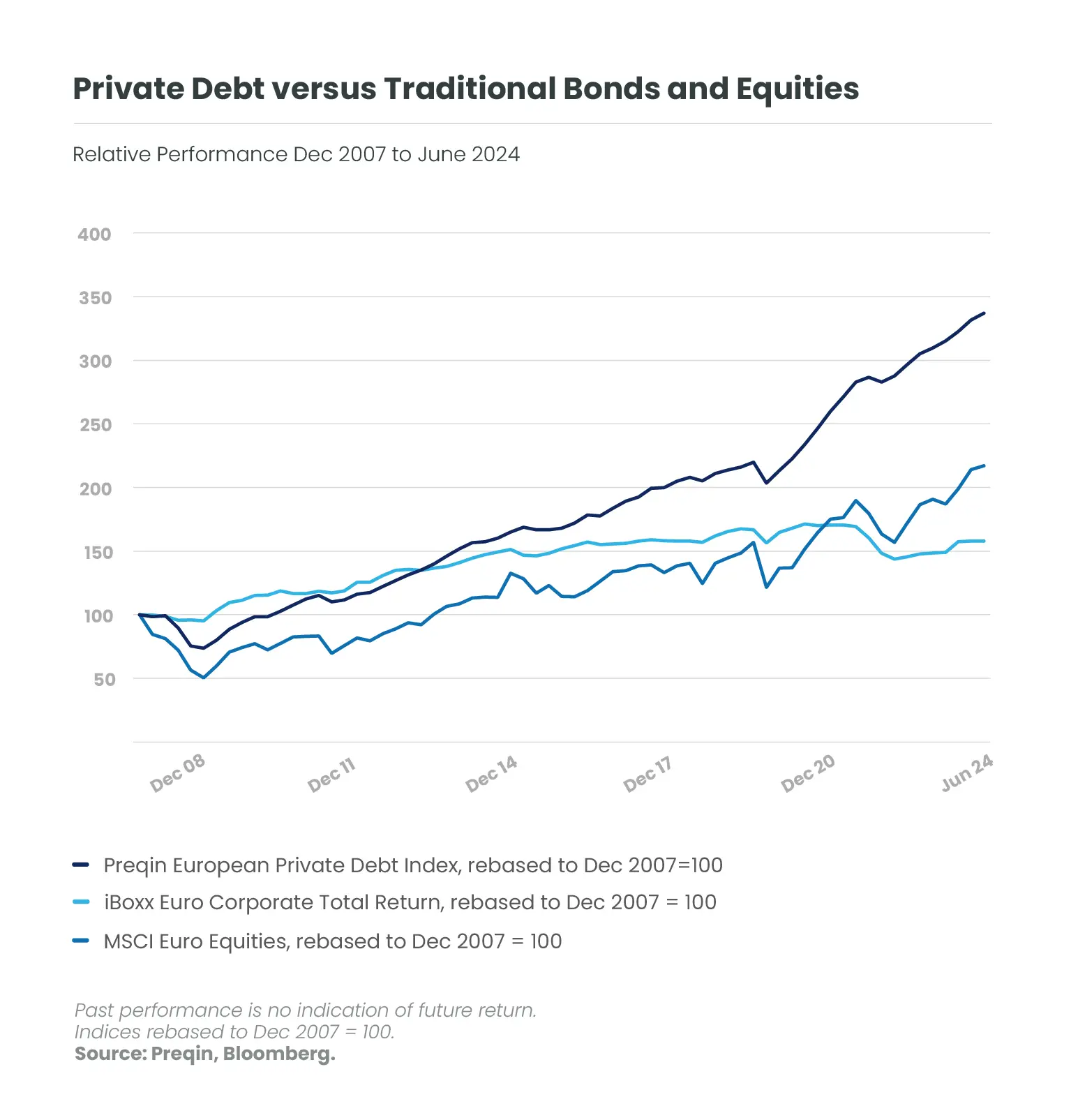

Private debt is a much younger market in Europe than in the US. Today the European private debt market exceeds EUR 400 billion, but it came into being as a noteworthy category only since the European debt crisis of 2009,[4] and the stricter capital costs for banks.

It can be argued that the spectacular growth[5] in European private debt was, as so often, because of the small base. True enough. But another reason was that in its infancy, overall levels of interest rates were low. As absolute rates normalize at a somewhat higher level, fixed income of any type is a more attractive asset class. With higher rates, interest rates on private loans are higher, too, making them potentially more interesting to investors than five years ago.

Private lending inherently offers higher interest than most publicly-traded debt. Their smaller sizes and shorter histories command a bit more return. Because this loan is in place until the initially agreed-upon due date, and is an illiquid investment, investors demand, and receive, an ‘illiquidity premium’, as well.

Investors who are new to this category should note that it can be considered an ‘alternative’ investment. Traditional or core investments such as public equities and bonds can be easily liquidated in normal markets, while investors are expected to hold any position in private debt for a specified period of years.

We will offer more insight into private debt in future articles. Stay tuned!

[1] Prequin Investor Survey, November 2024

[2] ELTIF = European Long-term Investment Fund, ELTIF

[3] Less than 10%.

[4] Prequin, 2024, Year in Review, Figure 2.3.

[5] From EUR49.5 billion in 2010, to EUR 427 billion in 2023, according to Preqion.

Get information faster with a single click