In July, markets consolidated their strong 1H 2019 performance. US equities – boosted by decent earnings reports and anticipations of the Fed’s interest rate cut – took the lead. As the market was already pricing in the Fed rate cut and as a revival of trade tensions could not be excluded, we already decided to reduce our equity exposure in July. Already at the beginning of August, markets started on a false note as the Fed appeared not dovish enough – hiking rates by 25 bps and stating that it was not the start of a new easing cycle – and Donald Trump announced new tariffs on Chinese goods. However, as long as a recession remains out of sight, investors will continue to be pushed towards risky assets, enough, for us, to justify buying the dips.

Equities vs bonds

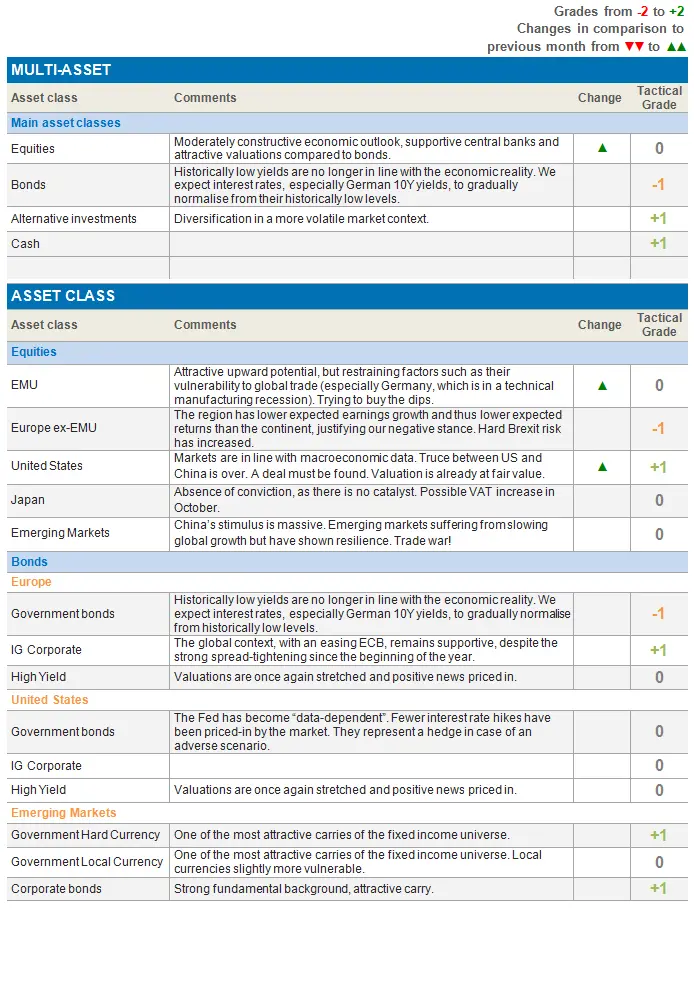

From a long-term perspective, we are still moderately constructive equities and cautious bonds. While we expect slightly higher bond yields in both the US and Germany towards the end of the year, equities still have moderate upside potential.

- We still have a moderately constructive economic scenario.

- Central banks have become more accommodative this summer. Lower interest rates and new stimulus measures should result in improving credit and equity-market confidence.

- Earnings are currently not supportive of equity-market performance. Despite decent earnings publications in the US, the European earnings season appears rather weak.

- Equity-market valuations remain, nevertheless interesting, especially when compared to bonds.

Developed economies should be able to absorb the new round of trade tensions, barring a significant rise in financial stress.

Taking into account our ability to avoid a recession and our being in a fast, difficult-to-predict market, we decided to start buying some equity exposure at lower levels.

Buying the dips is conditioned by a conviction that we are not at the end of the cycle and that a recession is not around the corner. The political risks could rapidly recede (as was the case in June). The impact on economic data will be longer-lasting.

We are therefore keeping some hedges in place in case of an adverse growth scenario. We decided to increase our position in gold and have kept our diversification towards the Japanese yen. Both asset classes have clearly demonstrated their safe-haven characteristics in recent months.

US equities remain our main conviction

We have increased our US equity overweight

US equities, under the shield of US president Trump and the Federal Reserve, remain our main conviction. Despite the market’s recent disappointment in the Fed’s communication, we are convinced that, if needed, the central bank will become more dovish. The 25 bps rate cut, instead of the 50 bps cut expected by markets, was in line with our expectations, given the current state of the US economy.

Earnings publications, in the meantime, are decent, with 76% of US companies presenting higher-than-expected earnings. Growth is, nevertheless, more or less flat, and companies’ guidance is leading to downward revisions for the second half of the year. A possible earnings disappointment in the coming month, however, could be offset by the announced stock buybacks.

Meanwhile, valuation, although slightly above average historical levels, is not excessive.

Emerging markets: back in the eye of the storm

In contrast to the decent economic context in developed markets, we have more doubts on emerging markets. In Asia, we see the uncertainty surrounding India’s shadow banking system, while China has little remaining monetary easing room.

Growth will without a doubt thus further decline and China continues to hold the key for emerging markets this year. Recent growth figures continued to show a growth decline and economic data remains mixed, despite the recent improvement in industrial production and exports. For the time being, we remain confident that China will be able to deliver at least 6% growth in 2019.

It is, nevertheless, difficult to have a strong conviction on the region, even though the new tariff increase of 10% on USD 300 billion worth of Chinese goods in September had been immediately priced in by markets. The region remains on our watch list, but we are staying neutral for now.

Euro zone: nominations and elections

Some political hurdles have been cleared, but threats remain

July was a busy month on the political side. Budget talks between the Italian government and the EU were constructive and several political nominations were officialised after several days of talks. The most important outcome was the nomination of Christine Lagarde to take over from Mario Draghi as new ECB President at the start of November. Christine Lagarde was one of the most dovish candidates to have expressed her vocal support of Draghi’s accommodative monetary policy.

After Christine Lagarde’s nomination, the ECB’s Governing Council emitted further signals that a new stimulus package was coming in September, pushing interest rates into deeper negative territory. A new round of asset purchases seems to be underway, while a tiering system is also being discussed to limit the negative impact on the financial sector.

These positive political changes have, nevertheless, been offset by the ongoing deterioration in economic data. Investors continue to avoid EMU equities with accelerating negative outflows, as they see an improvement in economic momentum as a pre-condition of investing in the region. German economic data in particular remain weak, and markets are now waiting for leading indicators to bottom out, before coming back to this attractively valued equity region.

Negative on Europe ex-EMU

Outside the EMU, the UK is still facing tougher challenges.

From an economic perspective, the UK appeared quite resilient. However, economic growth had been artificially supported by strong inventory build-up. Inventories will now start to be a drag on the economy, while we also expect exports to be weak.

From a political perspective, Boris Johnson has been elected (new) Prime Minister. His recent statements have been very clear: “We will leave the European Union on October 31 whether there is any agreement in place or not.” His majority is, nevertheless, limited and a possible confidence vote on September 3 might lead to increasing uncertainty and possibly new elections.

We are thus keeping a cautious view on Europe ex-EMU, especially the UK.

Bonds and currencies

In terms of bonds and currencies, providing the global economy avoids a recession, the macro-financial backdrop will favour carry. The highest carry can be found in emerging debt in hard currency.

We also remain invested in investment grade bonds. The global context, with an easing ECB, remains supportive, despite the strong spread-tightening since the beginning of the year. Carry-to-risk is interesting and the low-yield environment supports credit. We favour EUR credit.

In the currency universe, we remain long Yen, short USD, and are opting for a short GBP going forward.

We have further increased our gold exposure, as a hedge, based on the improving technical outlook and upward potential.