Are Central Bank objectives compatible with financial stability in an environment of stronger inflation? Following recent strategic changes in monetary policies and bold post-pandemic responses, policy makers are also balancing inequalities stemming from Quantitative Easing and their role in the fight against climate change.

An Unstable Equilibrium?

Global Inflation remains elevated due to supply chain bottlenecks and labor shortages. As price pressures continue unabated, bond markets have become more hawkish and have already tested the reaction functions of developed central banks. Notably, Australia removed the yield cap it had maintained on 3-year bonds.

The US Fed – Average Inflation Target, and Full Employment

The US Federal Reserve has a dual mandate, specifically price stability and full employment. A year ago, the Fed also adopted a flexible 2% average inflation target (FAIT), which must be consistent with a fully-participating labour market. Therefore the Fed can accept an inflation overshoot as long as full employment has not been reached. In its latest communications, the Fed recognized that inflation is running above its 2% target, but has described the excess as transitory, with a level closer to 2.2% by the end of 2022. As the US economy pursues its recovery, the central Bank has announced a normalization policy of reducing its $120 billion monthly asset purchases by $15 billion in November and December, with the aim of halting bond purchases towards the end of the second quarter of 2022. Based on the FOMC’s 'Dot Plot', rate hikes should arrive after tapering ends, as the US economy is still far from full employment (labor force participation has failed to pick up, in part due to early retirement programs).

Result? Following a 6.2% YoY rise in consumer prices in November, investors now seem to be pricing in interest rate increases from the Fed both sooner and more aggressively than the Bank is currently communicating. Our view is that the Fed could proceed with two rate hikes during the second half of 2022. It remains to be seen how the Fed will manage its oversized balance sheet. An active reduction of its balance sheet could take place before, during or after the initial rate hikes. For the moment this topic has been left unaddressed, but it will certainly be part of future policy decisions as it could complement the Fed’s toolbox on its journey towards policy normalisation.

The ECB – Symmetric Inflation Target, and Climate

In Europe, the ECB has adopted a symmetric inflation target and has reinforced its forward guidance. Further, the Bank will include climate factors in its monetary policy assessment. The ECB expects additional near-term inflation, declining during 2022 before falling below the 2% target in 2023. In terms of asset purchases, the € 1.875 billion PEPP Program will continue at a slower pace, ending in March 2022. This will be followed by a more flexible Asset Purchase Program.

Result? As in the US, expectations of higher European CPI around 4% have given rise to speculation of a potential rate hike in 2022. This option has been largely dismissed by Mrs. Lagarde during the ECB's most recent Monetary Policy Decision communication.

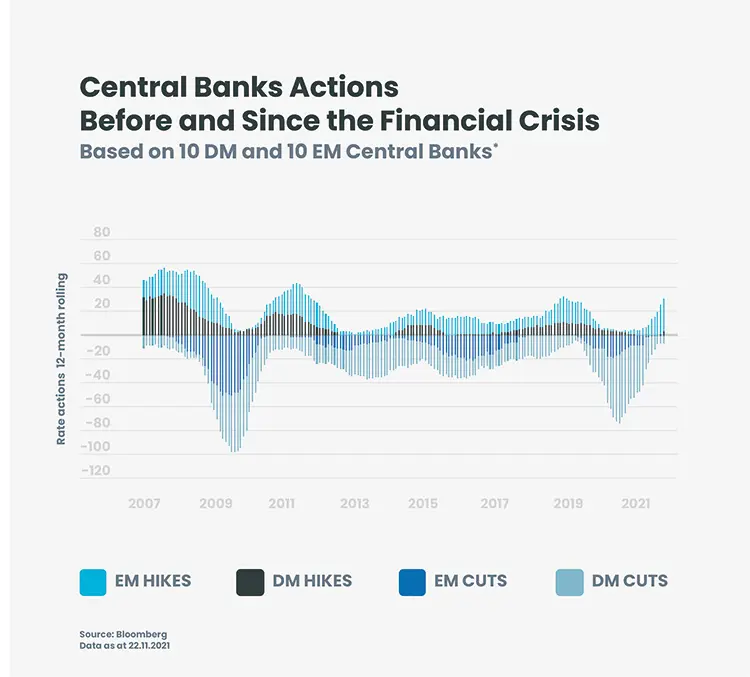

Emerging Markets Present a Contrast

This “patient approach” of DM Central Banks contrasts sharply with the recent actions of EM central banks. For example, Brazil has raised rates by 575bps since the beginning of 2021, notably with a hike of 150bps in October, its largest single-meeting move of the last 20 years.

Reactions Soon, Results Over Time

On the one hand, DM Central Banks run the risk of falling behind the curve, in which case they might need to act aggressively should inflation expectations become unanchored. Inflation now represents the main area of concern for companies, while consumers are feeling the impact of higher prices. Wage pressures also need to be closely monitored as they could create a feedback loop that could convert short-term inflation into a more permanent feature. On the other hand, an aggressive response to (potentially) transitory inflation could jeopardize the economic recovery and risks precipitating an abrupt slowdown, in a context of globally-higher government and consumer debt.

The drivers of the surge in prices – particularly supply chain bottlenecks -- should persist for a couple of months while the energy shock adds uncertainty to the growth trajectory. In this context, the new reaction functions of Central Banks will be put rapidly to the test. Only time will tell whether their patience will have been rewarded with resilient growth and financial stability.

* Central Banks – DM = US, EU, UK, Japan, Canada, Australia, New Zealand, Norway, Sweden, Switzerland EM = China, Mexico, Brazil, Indonesia, Turkey, Russia, South Africa, Czech Republic, Hungary, Poland.