Servaas Michielssens

PhD, CFA, Head of Healthcare, Thematic Global Equity

Biotech can be considered the innovation engine of the biopharma and drug sector, often sitting at the cutting edge of the next medical breakthrough. Over time, the distinction between pharmaceuticals and biotechnology has blurred, as pharmaceutical companies have acquired traditional biotech firms and their technologies. Today, most of the top 10 best-selling drugs globally are biotech-derived.

The biotech sector is characterized by high growth, innovation-driven developments, and structural support from demographic shifts. It also offers defensive commercial business investment opportunities, making it a compelling sector for long-term investors.

Despite its crucial role in healthcare innovation, biotech remains underrepresented in broad market indices. Traditional biotech companies make up less than 10% of the MSCI World Healthcare index and an even smaller proportion of the MSCI World index[1]. As a result, investors do not gain significant exposure to this sector through broader generalist US strategies.

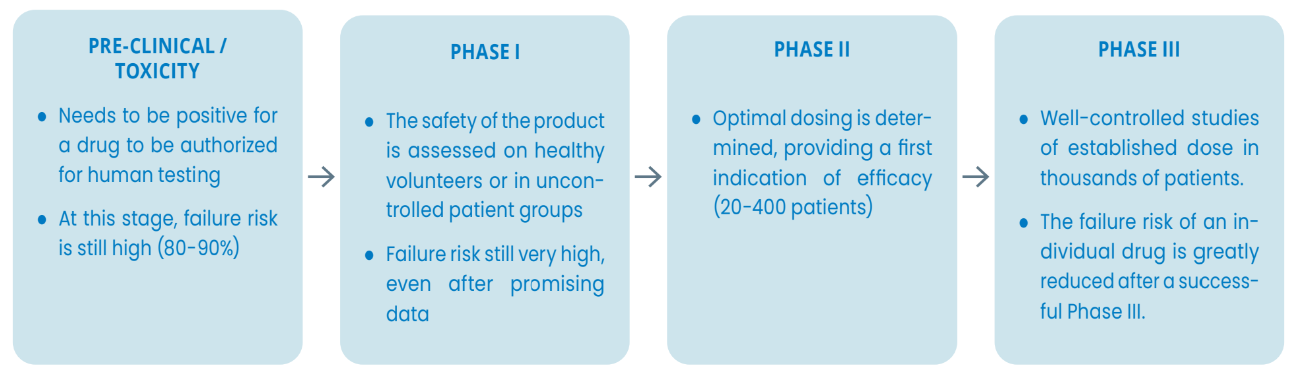

This underrepresentation, combined with the unique characteristics of the biotech industry, creates a compelling case for active stock selection. The sector's reliance on Research & Development (“R&D”) pipelines leads to significant dispersion in share prices, making biotech a stockpickers’ market. Over time, biotech share prices tend to correlate with revenue and sales growth. As such, we continue to focus on material commercial opportunities.

Beyond individual stock opportunities, the broader biopharma sector has demonstrated its value over the last 5-10 years, transforming the outlook for patients with various cancers and bringing Covid-19 vaccines to market in record time.

Looking ahead, we remain focused on breakthrough medical innovations that will impact patients across the multiple disease areas, including neurology and CNS (Central Nervous System), oncology, rare diseases, cardiometabolic conditions and more. At the same time, M&A activity continues to be a tailwind for equity performance in the biotechnology sector as large cap biotherapeutic companies continue to use this as a way to bolster R&D pipelines with quality innovation.

The ideal timing for investing in biotech varies with each investment opportunity. Early-stage drug development investments may offer yield significant returns but come with higher risk. Later-stage of development have a higher probability of success but often come with lower potential returns. Additionally, strong investment opportunities exist in companies with already-approved drugs where clinical launches are expected to exceed commercial expectations.

Moreover, how these companies preform within the macroeconomic environment varies, requiring careful consideration in portfolio composition. We aim to build a balanced portfolio of high-conviction, quality biotech companies.

To be a successful biotech investor, one must evaluate three critical factors: science, company management team, and valuation:

Mastering biotech investing requires deep scientific knowledge, financial expertise, and industry experience. At Candriam, our team brings nearly a century of combined expertise across scientific research, industry, and finance. Contrary to common intuition, the results of clinical trials are rarely straightforward or binary—they often require nuanced shades of interpretation. Analyzing this data demands a profound understanding of disease contexts, which our healthcare team has developed over many years.

Additionally, translating this knowledge into valuation is a craft that requires extensive experience. Our team comprises six professionals, including four PhD holders, five with scientific degrees, and two Chartered Financial Analysts (CFAs). This multidisciplinary expertise allows us to navigate the complexities of biotech investing with confidence, positioning us to capture the transformative potential of medical innovation.

Servaas Michielssens and Linden Thomson answer investors’ questions about a sector where depth of specialist knowledge is a prerequisite to consistent stock selection success.

[1] Source: Candriam

Risk of capital loss

There is no guarantee for investors relating to the capital invested in the sub-fund in question, and investors may not receive back the full amount invested.

Equity risk

Some strategies may be exposed to equity market risk through direct investment (through transferable securities and/or derivative products). These investments, which generate long or short exposure, may entail a risk of substantial losses. A variation in the equity market in the reverse direction to the positions can lead to the risk of losses and may cause the performance to fall.

The risks listed are not exhaustive, and further details on risks are available in regulatory documents.

Get information faster with a single click