A Trump hurricane

Keypoints

- As expected, ’Liberation Day‘ has brought a raft of new tariffs.

- The policy/ sentiment shock is now likely to derail the US economy .

- We turn more defensive and downgrade equities across the board.

Since his return to the White House, Trump has announced a series of country or sectoral tariff increases. If we combine all the measures announced before 2 April (20% on China, 25% on Canada and Mexico with exemption for goods that comply with the USMCA[1], 25% on steel and aluminum and 25% on automobiles and parts), the average tariff rate on US imports was on course to reach 11%[2] from 2.5% end of 2024. Put in perspective, this would already have brought the average tariff rate of US imports back to the level of the early 1940s.

US Liberation Day

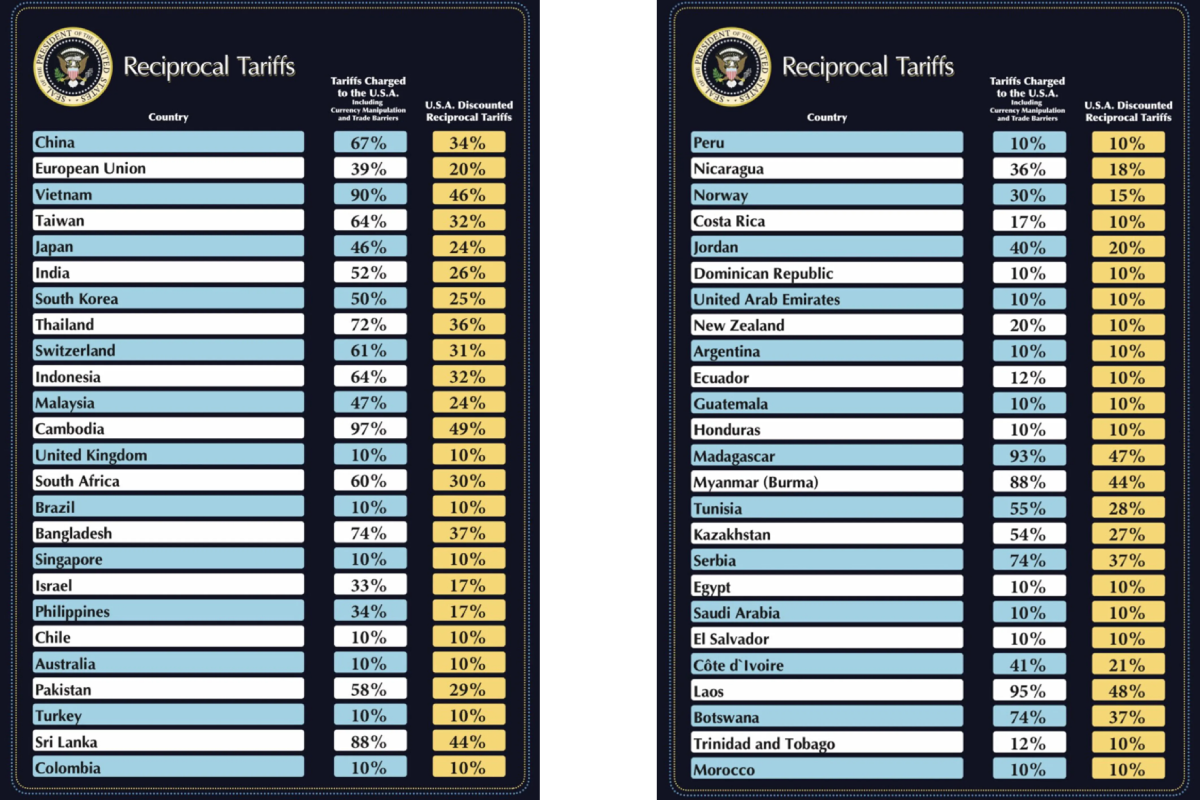

On 2 April, D. Trump announced sweeping new tariffs: a 10% minimum baseline tax will apply on imports from all countries while countries running trade surplus with the US will face much higher “reciprocal tariffs”: the EU for example will be charged 20%, Japan 24%, South Korea 25%, China 34%... Cambodia 49%! Note that in the case of China, those tariffs apply on top of the previous “fentanyl-related” 20%. While some tariffs might come down in the future, the direction taken by the Trump’s Administration is clear: the average tariff rate on US imports is now likely to be significantly above 15%[3] by year end the more so since the language in the executive order suggests that additional sectors tariffs are forthcoming.

Source: US President Donald Trump via Truth Social

A US policy / sentiment shock is now our main scenario

Over the past few weeks, there have been more and more signs that the US Administration was serious about raising tariffs. Whether or not tariffs are part of a broader agenda[4], Trump views them not only as a negotiating tool, but also as a means of correcting trade imbalances, re-industrializing the US and raising fiscal revenue. Peter Navarro, a close White House aide, recently claimed that President Trump's new tariffs would generate more than $6 trillion in federal revenue over the next decade, implying not only high, but permanent tariffs. Trump and some of his advisors may also see tariffs as a tool to shore up support among his political base, as the tariff war waged during Trump 1.0 appears to have been a political success for the Republican party.[5]

This aggressive tariff policy is likely to crimp growth and, combined with a “tough” immigration policy as well as the DOGE (Department of Government Efficiency) policy, will bring more uncertainty. Although the US economy began the year on a solid footing, higher inflation and falling stock-markets are likely to dampen consumption, while lingering uncertainty will prompt companies to be cautious both in terms of new investment and hiring plans.

Of course, gauging the size of the shock to the US economy is challenging: negotiation could help mitigate tariff hikes, while retaliatory measures could exacerbate the impact of announced tariffs. We now believe that our adverse scenario of policy and sentiment shocks derailing the expansion has become more probable than that of a ’soft landing‘: a recession by the end of 2025 looks increasingly likely and inflation is set to be pushed upwards by 2%[6]. In this scenario, the US Federal Reserve would not be preemptive and would wait for more clarity (magnitude of tariffs pass-through to inflation, offsetting fiscal support…) and material signs of the slowdown before easing further: we expect three more cuts from the Fed in 2025.

What impact on the Euro Area?

Before the return of Trump at the White House, growth was on track to hover around 1%[7] in 2025 in the Euro Area. Since then, the European reaction triggered by the US threats to pull away America’s security blanket for Europe has led many to revise their growth scenario upwards. We cautioned[8] about market optimism on the short term expected economic support resulting from ReArm Europe Plan / Readiness 2030 and Germany’s U-turn in fiscal policy in a recent note: over a one year horizon, we expect the new measures announced by European leaders to only mitigate the negative consequences of the forthcoming trade war with the United States. Moreover, in the short run, significant execution risks associated with the German infrastructure investment plan, in particular, are real: “shovel ready” infrastructure projects are unlikely to be numerous enough to immediately offset the shock from higher tariffs.

As in the US, rising uncertainty could also lead European businesses to postpone their investment and hiring plans. What’s more, Europe is a very open area and quite sensitive to world growth. Hence, a ”soft patch“ in the coming quarters is more likely than a scenario where growth is increasing at its 1% trend pace.

Whether Europe attempts to negotiate or threatens to use its new bazooka (the Anti-Coercion Instrument or ACI) remains an open question. In any case, with inflation having receded, the ECB is well-positioned to respond to the shock. We expect the central bank to cut rates by at least another 50 basis points, but it could very well cut rates below 2% if necessary.

More defensive

President Trump’s latest tariff announcement was more aggressive than anticipated by markets. This escalation is contributing to a more fragile global economic backdrop. Recession risks are clearly rising. While there may be room for negotiation and potential easing of announced tariffs, retaliatory actions from trading partners could further amplify downside risks.

We had already adopted a more cautious asset allocation stance in recent weeks considering mounting global uncertainties, particularly in the United States, and limited visibility on short-term market direction. The persistence of a high level of uncertainty, along with the deterioration of our economic scenario—not only in the US but also globally—makes us even more cautious regarding risky assets globally.

We have again reduced our exposure to US equities., Our concerns about growth are likely to result in further downward revisions to corporate earnings, while US price-to-earnings ratios remain elevated compared to their historical averages and to other regions. In addition, we now also downgrade the Eurozone, Emerging Markets and Japan to underweight. While the search for greater international diversification could generate positive flows, ongoing trade tensions and rising external vulnerabilities are likely to drive equity indices lower, pricing a higher risk of recession.

Our positioning reflects a preference for defensive equity profiles, favoring companies with stable cash flows and lower sensitivity to macroeconomic shocks. In Europe, we remain constructive on the Utilities and Consumer Staples sectors, while we remain cautious on Cyclicals.

Prefer European duration and add some hedges

On the fixed income side, we remain long duration on European sovereign bonds, particularly the Bund, supported by a dovish monetary policy stance. That said, the current environment is challenging for multi-asset portfolios. Rising inflation expectations are likely to cap any further decline in yields, reducing the effectiveness of sovereign bonds as a hedge against a deterioration in the economic outlook. "Stagflation" represents one of the most adverse scenarios for diversified portfolios, offering few places to hide.

Our view on credit remains cautious: we are neutral on investment grade but maintain an underweight stance on high yield, both in Europe and the US. Spreads have only widened moderately so far and should continue to widen as weaker corporate fundamentals are gradually priced in.

Finally, we continue to see value in alternative assets—notably precious metals such as gold and silver, which remain effective hedges in an environment of heightened volatility and trade uncertainty. In currencies, we had a positive view on the Japanese yen, which we saw as a likely beneficiary of increased risk aversion. However, we expect the tariffs announced on Japan yesterday to weigh on the Japanese economy and could challenge our constructive stance on the currency.

Some alternative strategies may help protect a multi-asset portfolio—particularly equity market neutral strategies, which could benefit from increased volatility and dispersion without being exposed to directional market risk.

[1] In 2020, the USMCA, or United States-Mexico-Canada Agreement, replaced the 1992 NAFTA, or North American Free Trade Agreement

[2] Source: Candriam

[3] If all current tariffs proposals were to be maintained, our calculations suggest the average tariff rate would shoot up to 23%.

[4] See “A User’s Guide to Restructuring the Global Trading System”, S. Miran (November 2024).

[5] “[…] voters from regions whose industries were heavily exposed to Chinese import competition in prior decades rewarded President Trump the most for import tariff protection”, in D. Auto, A. Beck, D. Dorn, G. Hanson (2024) “Help for the Heartland? The Employment and Electoral Effects of the Trump Tariffs in the United States”, NBER working paper 32082.

[6] Source: Candriam

[7] Source: Candriam

[8] See “Update on ReArm Europe: Economic & Financial Consequences”.