The downturn in the activity cycle continued right up until year-end, with every country in the G10 region now in either ‘downturn’ or ‘recession’ territory. This trend has been perfectly in line with the recent IMF forecast which downgraded global growth. The US is certainly a participant in the trend and recent data prints such as the ISM manufacturing have seen decline, though the risk of recession appears to have receded. While markets point towards an un-inverted yield curve, the Feds intervention on repo markets could also be a reason for the phenomenon. In the euro zone, the business cycle continues to decelerate and the probability of downturn is now above 50%, while in Japan, the cycle is grinding lower. The UK economy doesn’t appear to be improving and is still in a recessionary phase though uncertainty over Brexit has cleared up with the UK now having left the EU, though a new trade deal does seem to encounter speed bumps. All-in-all, the weakness in the global activity cycle, confirmed by our in-house models (since the beginning of 2019), is present though the probability of an all-out recession has receded. In spite of historic efforts of central banks, inflation levels still remain stubbornly low. The US inflation cycle has dipped below average into disinflation territory. The euro zone, which was somewhat of an outlier during the past months, has seen its indicator nose-dive and doesn’t show any signs of bottoming out. Unsurprisingly, under these conditions, central banks across the globe have continued to maintain their dovish stance, to the delight of investors. What is also worrying is that 2019 was marked by extraordinary activity from central banks that collectively took a dovish stance, lowered rates and bought assets. In spite of this, (and almost 6 months after), we still do not see inflation levels moving. Central banks on their side continue to be prudent and ready to act and EM central banks certainly have ammunition to deploy in the face of weak data. The retracement of geopolitical threats (trade war, Brexit, and Iran) appears to have been replaced by the coronavirus crisis, which has sent ripples across markets. China has been the main victim as GDP contraction is very likely to be seen, and we can expect further intervention (post the two central bank rate cuts) in the form of fiscal stimulus in order to boost the faltering economic growth. Developed markets will also be impacted by the virus as a result of supply chain disruptions. While the full impact is yet to be assessed, we believe core bond markets are likely to benefit from the outbreak and credit markets are likely to be subjected to increased volatility in the wake of the contagion, highlighting the importance of being selective.

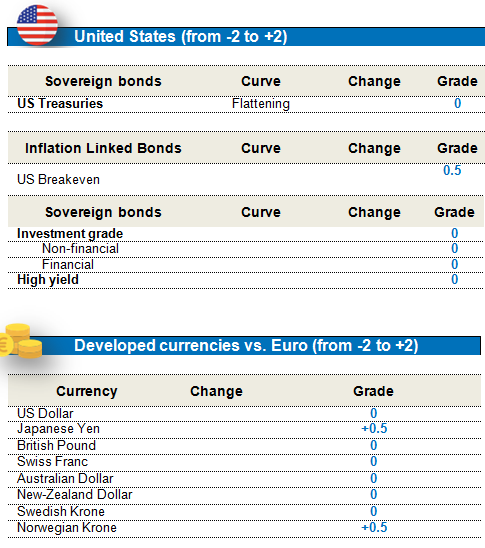

Neutral on Core European Rates and US rates

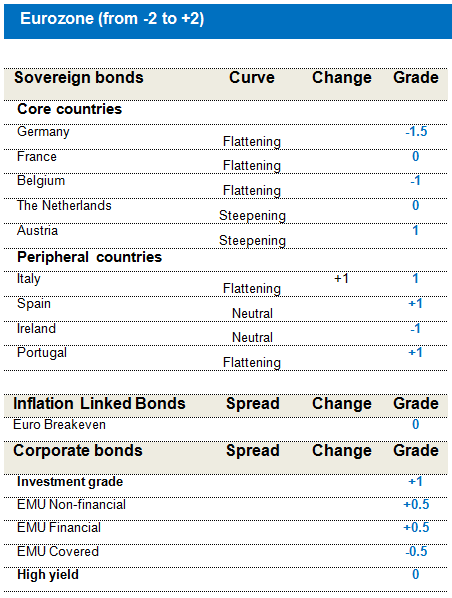

The Fed recently signalled its intent to hold rates low and in fact warned about the negative effects of the coronavirus. In this context, we prefer to move to a neutral stance on US rates rather than our previous negative stance. In the dollar bloc, we also have a small preference for Australian bonds, as activity cycle continues to deteriorate, helped along by bushfires and proximity to China (and hence negative impacts of the virus). Furthermore, the central bank appears to have dry powder to act in the form or rates or even a potential QE. European non-core markets have continued to receive support from the ECB’s quantitative easing and strong performance has been seen since the beginning of the year, with a special mention to Italy. where the extra premium priced in for Italian spreads due to risk of early elections has further room to decrease. With Spain and Portugal also exhibiting low short term political risk, we hold a material overweight position on peripheral sovereign bonds in the euro zone. Ireland is an exception to this as recent election saw the Sinn Fein achieve a historic result by scoring the highest percentage vote. We keep our negative stance on Ireland given current valuations.

Core euro zone rates have seen a significant move downwards with German rates moving from -0.2 to -0.4 in a matter of two weeks, principally driven by the uncertainty surrounding the outbreak and the economic impact of the corona virus. Indeed, in spite of the QE strategic review and some better data, safe havens such as German rates did well. In the face of an increased allocation to peripheral rates, our overall allocation to euro zone rates is neutral, thanks to the underweight stance towards German rates, which are relatively expensive versus their core sovereign peers (France, Austria).

We closed our long euro break-even inflation strategy on the back of the important performance seen since the summer and negative short term headwinds ahead. Indeed with weak oil price dynamics, weaker headline inflation data ahead in the coming months, historically high supply pipeline for Q1 and the less appealing break-even inflation carry in March we moved back neutral.

Developed Market Currencies: Neutral USD

Our proprietary framework continues to point towards a negative view on the US dollar. The Fed’s rate cuts and dovish stance also point to a weaker dollar, with the US president clearly indicating his preference for a weaker greenback. However, we do expect that, after recent actions, central banks are going to take a breather. In this context, we prefer to have a neutral position on the greenback and we continue to tactically manage the position.

Credit: Maintain Exposure to European Investment Grade

We maintain a favourable view on European IG asset class despite of its tight valuation. Strong technicals continue to support the asset class with massive inflows. The ECB backstop remains the primary source of support with more than €5bn net purchases in January. With the current purchase programme, net supply will be negative, supporting the cash market and containing any widening in spreads. Fundamentals appears healthy but we cannot exclude some profits revisions during the 2 next quarters following the pandemic and drastic measures adopted by Chinese authorities. Selectivity is still key as fallen angels risk remain with 20% of BBB companies at risk to be downgraded. Even if up to now companies are able to defend their IG rating, any downward revision in profits could accelerate the downgrades path. It’s even more true for US IG market as 30% of BBB are at risk. Debut issuers entered in the market in last December & January post weak fundamentals. So, taking into account higher leverage, higher sensitivity to interest rate and hedging cost, there is no incentive for an European investor to switch to the USD market.

High Yield market retraced nearly all of its tightening during the January sell off. While it appears less expensive than two months ago , there were few opportunities out of oil & gas and telecom sectors. We prefer to wait better level to entry as low quality names are more sensitive to potential growth revisions following the coronavirus crisis. Moreover net supply is very positive on the asset class Only in January, €6bn were offered while there are only €34bn of redemptions for the year! Even if it’s well absorbed, it’s too complacency in the present environment.

Emerging Markets: more constructive on expectation of global growth stabilization and recovery on declining trade war risks

We remain cautiously constructive on EMD HC as the asset class continues to explicitly benefit from the accommodative Developed Market and Emerging Market central bank stance, from the stable outlook for commodities and expectations of a near-term de-escalation of the US-China trade relationship. The likelihood of the US and China agreeing on a mini-Phase 1 trade deal by end of Q1 2020 at the latest should deliver an uptick in risk sentiment. Absolute asset class valuations are not as attractive as at the start of the year, although there are pockets of value in select EM credits, especially in B- and BB-rated credits, where we are concentrating exposures, and in relative terms – versus US credit – as the percentage of negative-yielding fixed income securities has increased beyond their 2016 highs.

In our local currency allocation, we have neutralized the overall duration exposure and rotated from lower (Malaysia, Thailand) to higher yielding rates markets (Indonesia, Mexico) with residual upside in acknowledgement that EM central banks easing cycles are close to complete for now.

We retain an overall neutral EMFX exposure on concerns that the coronavirus growth impact is challenging the thesis of growth outperformance of EM versus the US – a necessary condition for EMFX outperformance. If we note a re-launch of the EM to DM growth outperformance we stand ready to add EMFX exposure.

Hard currency

The asset class rallied (1.5%) although the composition of performance switched from EM spread (-1.5%) to a US Treasury (3.1%) mid-month, in line with the rise of the coronavirus fears, and despite the better than expected global activity data. As a 'risk-off' mode set in, EM spreads widened by 23bps (to 314 bps), 10Y US Treasury yields rallied by 41bps (to 1.51%), Oil (-11.9%) collapsed on concerns over the impact of the global epidemic on the fragile global growth recovery, although the S&P 500 (-0.16%) held on to its December gains signaling a more muted and transitory impact. Province of Buenos Aires (Argentina) attempted to extend a partial amortization payment of a 2021 bond due in January to early May which was interpreted as adding unnecessary complications to an already difficult sovereign restructuring. IG (2.3%) out-performed HY (0.6%) with Suriname (+10.7%) and Tajikistan (8.1%) posting the highest and Argentina (-8.1%) and Ecuador (-5.5%) the lowest returns.

With a yield of 4.8%, EMD HC valuations are not compelling in absolute terms although they still offer value in relative terms to a still large universe of negative yielding global FI. The EM HY to IG spread is still attractive as are the EM single and double B rating categories versus their US HY counterparts. The medium term case for EMD remains supported by the stable US Treasuries and commodities outlook. Global growth and trade stabilisation can support the next leg of EM spread compression in environment of low trade tensions. On a one year horizon, we expect EMD HC to return around 2%, on an assumption of 10Y US Treasury yields at 1.7% and EM spreads at 300bps.

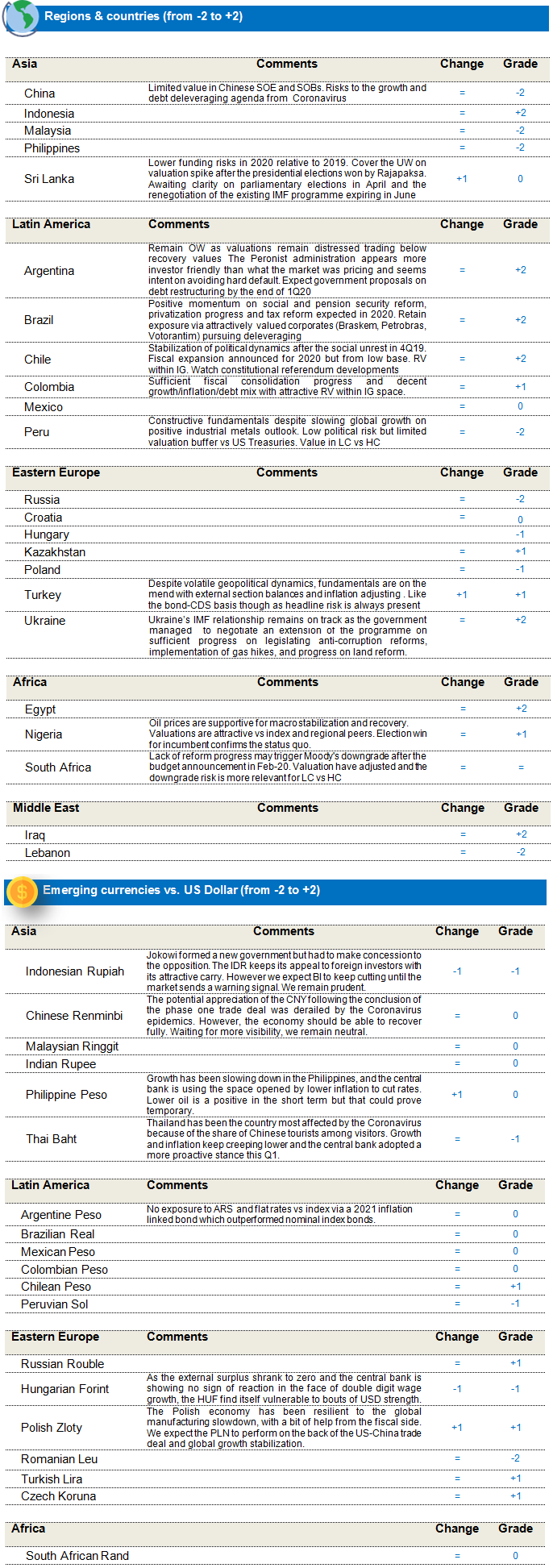

We retain an overweight of HY versus IG. In the High Yield space we remain exposed to idiosyncratic stories like Egypt, Ghana and Ukraine as these continue to offer value relative to the balance of fundamental/political risks, and to attractively priced energy exporters like Angola, Bahrain, and Ecuador. We retain exposure to Argentina as assets trade as distressed around the high 40s and below expected recovery values of around 60-70 cents on the USD. In the Investment Grade space we hold positions in Indonesia and Romania but remain under-exposed to the most expensive parts of this segment like China, Malaysia, the Philippines, and Peru.

We have retained underweights in Lebanon, Russia and Saudi Arabia as we do not assess we would get compensated for sanctions or political risks in these credits. In Brazil, Mexico and Turkey we hold overweights in attractively priced quasi-sovereigns and corporate bonds versus underweights in sovereign bonds. We also retain a tactical 6% CDX.EM asset class protection position in general asset class uncertainty related to the coronavirus global growth impact.

Local currency

The asset class saw a correction of 1.3% in January, from FX (2.7%), while duration added 1% and carry 0.5%. The market's bias to start the year adding risk was troubled by the breakout of the coronavirus in the Chinese province of Hubei. The virus triggered a knee jerk reaction in Oil (-12%) and core rates that also supported duration in EM local markets, while EM currencies where investors were most positioned saw a surge in volatility. Currencies most exposed to China underperformed, either through commodities (ZAR -6.8%, CLP -6.1%), or tourism (THB, -4.7%), while those seen as better insulated outperformed (IDR, 1.7%). CEE was in line with the EUR (-1.2%), with conservativeness of monetary policy being the differentiator (from HUF, -3.3% to CZK, -0.4%).

The rally in US treasuries (-40 bps) supported duration in Latam and Asia, where activity or inflation are still easing. Colombia tightened by 38 bps, followed by Brazil, Mexico, Indonesia and Malaysia all close to -20 bps. Rates underperformed in Chile (+13 bps) and Hungary (+9 bps).

We believe that with a yield of 5%, the asset class compares well to Fixed Income alternatives; especially given the respite from US-China trade tensions and global growth showing signs of picking up. The medium term case for EMD also remains supported by the improvement in the quality of fundamentals, benign inflation outlook and accommodative monetary policy globally. On a one year horizon, we expect EMD LC to return around 6%, with only a marginal addition from EMFX (1.0%) given the slightly stronger global outlook.

In EMD LC, we took partial profits in our lower yielding LC duration exposure and are now more exposed to higher yielding LC markets after the December announcement of a US-China trade deal raised hopes for global growth stabilization and as value in lower yielding, Treasury sensitive EM markets seemed exhausted. The EMD LC strategy is now only marginally long duration via high yielders like Indonesia, Mexico and a lower yielding China and Poland; moderately long duration in high yielders like the Dominican Republic, Peru, Russia, and Turkey and a lower yielder Malaysia, and is close to flat the rest of the EMD LC local bond markets.

The breakout of the coronavirus in China, and its diffusion in the rest of the world, has brought the global pickup in growth to a pause, despite the conclusion of the phase 1 trade deal. The proactive measures taken by the local government are causing significant disruptions in the global supply chain, in particular the electronic sector, and marginally in services.