Alternative Investments, Fixed Income, Private Debt, Private Assets, Real Estate, Research Paper

Real Estate Private Debt: Time to Act?

Has commercial real estate reached its inflection point?

Agility underpins the private lending industry. So along with our strategic partner Kartesia, what changes are we seeing today, and are direct lenders ready?

Rates, of course, are always top-of-mind. Today, markets appear to be in the proverbial sweet spot for direct lending to small- and medium-sized (SME) borrowers. Rates are high enough to attract financial investors in these loans, yet within a range where the SME borrowers are likely to find spending on acquisitions worthwhile, generating some supply of loans from these (SME) borrowers.

The next topic for anyone who follows the news must be the potential impacts of geopolitics on SME borrowers. The bulk of Kartesia’s private loans are to European-based firms operating in defensive sectors, such as business services, healthcare, and financial services. Nevertheless, these borrowers may be looking to grow outside of their home markets, or may have important supply chains outside of Europe. Are borrowers diversifying any single-source supply chains they might rely on (for example, from China)? If these SME companies distribute product into the US, or plan to, will they be establishing US-based manufacturing?

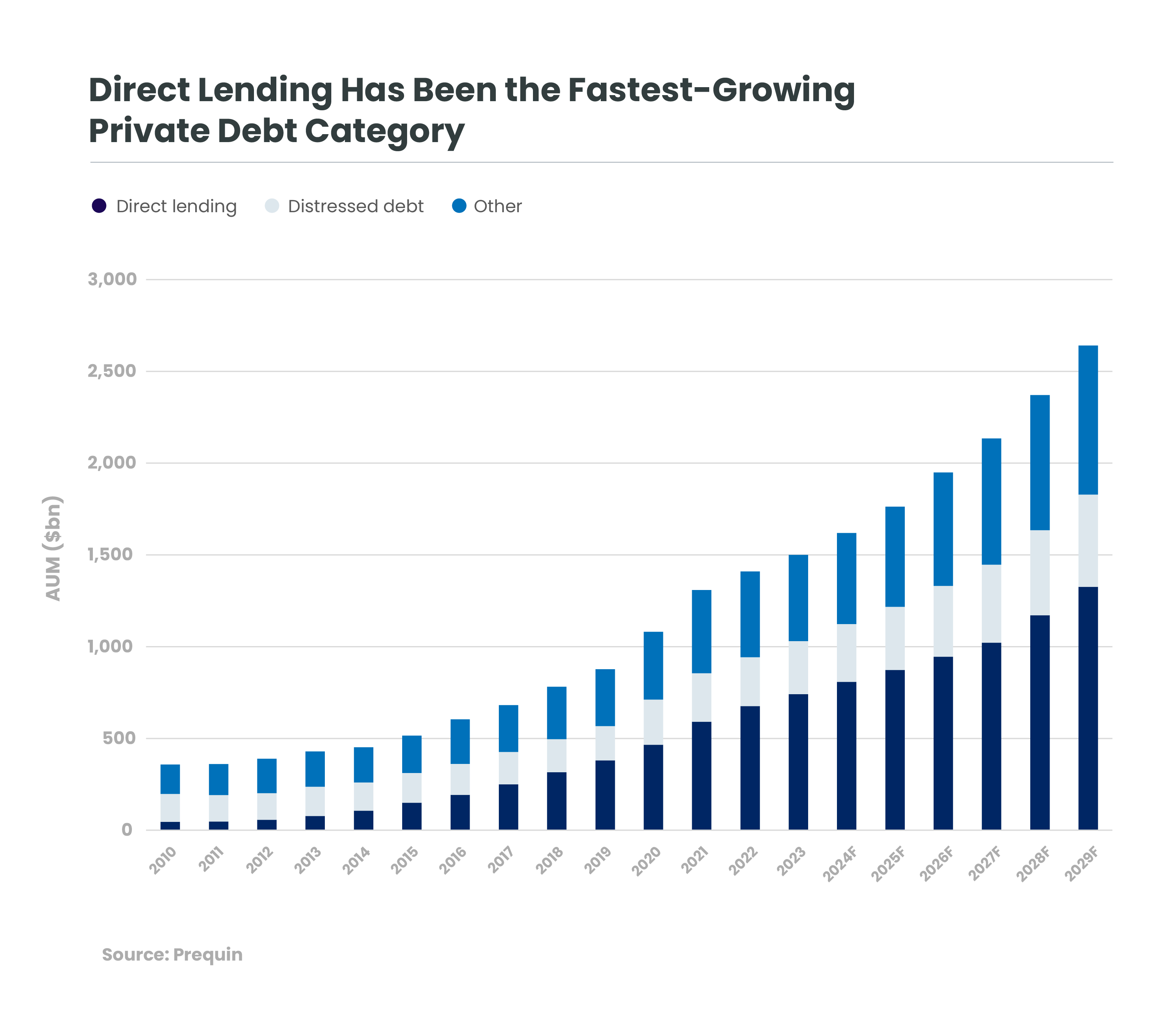

Direct lenders such as Kartesia naturally compete with banks, sometimes directly, in the frequently-changing lending landscape. At the larger end of the market, with M&A volumes down, yield spreads on large loans have shrunk while terms have loosened. Large borrowers are permitted higher leverage levels with fewer and weaker covenants as large banks compete for business. But that competition has not pressured the lower mid-market sector where Kartesia prefers to operate. Direct lenders still have opportunities to lend to resilient businesses which cannot access the markets directly, and to establish appropriate protections on that debt, across every part of the capital structure.

Non-sponsored deals have risen steadily over the last decade, and particularly since 2022.[1] That is, instead of a private equity firm seeking funding for a company in which they hold a large or majority position, company founders and owners are approaching private debt lenders directly. This allows these founder-owners to grow without diluting their ownership. As a direct lender, Kartesia believes that both sides of the transaction are Kartesia clients – clients are both our borrowers, and our investors who hold those loans.

These two apparently unconnected trends – the increase in non-sponsored deals, and the apparent dichotomy in terms between large borrowers and the lower mid-market -- both aid us in risk identification and management. In any environment, our fixed income mantra at Kartesia, and for Candriam, is to manage risk and protect the downside. As credit managers, we always concentrate on risk mitigation. While covenants are eroding for some larger borrowers, Kartesia and some other private debt lenders remain able to negotiate business-relevant covenants. In every part of the debt tier, Kartesia professionals stay close to the management teams of the portfolio companies. Often, Kartesia experts hold either board or board observer seats. This allows Kartesia’s industry specialists, often with relevant industry experience themselves, to offer early guidance on any challenges that might appear.

Regional opportunities change, too. As it is rare for European economies to all be strong simultaneously, operating from eight locations allows our Kartesia team to be close to the opportunities as they arise. When softer M&A trends in the UK and France reduced the supply and therefore increased the competition among direct lenders for high-quality credits, the more favourable macro environments in the Benelux, Spain, and Italy generated strong deal flow in those countries. Whatever changes Kartesia might find in Germany over the medium term, our experts are ready.

With new ways to participate in non-traded investments such as the European ELTIF, both institutions and individuals can now participate.

Kartesia is agile not just geographically, but across sectors and levels of complexity – from senior vanilla debt all the way through the capital structure, even in equity. Our private debt specialists think that hybrid products will soon become real alternatives to private equity, unlocking value and growth for entrepreneurs who want to fund their growth without giving away control of their businesses.

It is no coincidence that Kartesia is part of the Candriam family. The Kartesia private debt range also includes impact strategies, a skill set we are jointly able to offer across our range of borrowers and products as the importance of sustainability grows in Europe for all types of businesses. The Kartesia stable of SME borrowing clients are tuning in to both the value-creation and risk control aspects of sustainability. Their customers, in turn, are asking these SMEs for evidence of positive impact when they bid for assignments and new business. Because Kartesia focuses on the lower mid-market, the borrowers are often not large enough yet to have either the sophistication, or the budget, for dedicated resources. Until they grow and evolve, we can help them not only improve their sustainability, but also measure it through KPIs and demonstrate their progress to customers and the financial community.

Despite some obvious macro challenges in Europe, private debt managers with a varied product range and broad European coverage are likely to encounter opportunities and raise their pace of investment in the medium term. During the zero-yield and lower-for-longer era, investors struggled g to find absolute return, with many categories of investors pushed further up the risk profile than they would otherwise prefer. The combination of higher absolute rates, the developments in private debt, and the ability of managers to both maintain spreads and address risk directly at smaller borrowers adds up to absolute returns and managed risk in this segment. With new ways to participate in non-traded investments such as the European ELTIF, both institutions and individuals can now participate. Along with these higher base rates, Kartesia projects a broader group of investors can now find 8-10%[2] unlevered net returns in a diversified senior loan portfolio, an attractive proposition.

All investments involve risks, including the risk of loss of capital. Returns are not guaranteed, and there can be no assurance that a private loan portfolio will consist entirely of senior loans, or achieve comparable results.

[1] Private Debt Investor, April 2023, The ascent of the non-sponsored market.

[2] FS Investments indicates that upper middle marker price credit was yielding 10.15% as of 25 January. Private credit yield premium hits a four-year high. Accessed 17 March, 2025.

Get information faster with a single click