Donald Trump’s return to the White House will likely bring a clearer picture of how dominant his policy plans will be. Undoubtedly, his rhetoric and his policy decisions will shape and shake the economy and financial markets. As we move further into 2025, financial markets continue to demonstrate resilience, supported by ongoing global growth, accommodative monetary policies and strong profit growth in the technology sector. In this context, we start the year with an overall slight overweight stance on global equities, with a focus on the United States amid supportive fundamentals. Regarding fixed income, we keep our preference for duration in core Europe (Germany) as we expect low growth for 2025 and the ECB will lower its rates further. Conversely, we are negative on US duration: the risk for US yields remains on the upside and the future will depend on the policies of the new administration. We remain long US dollar and Japanese yen.

Robust US economic growth constitutes the main driver for equities

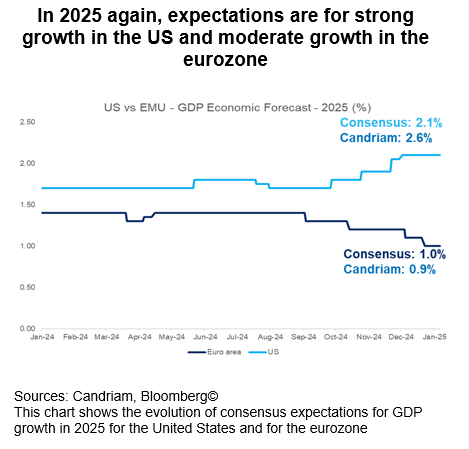

Expectations for 2025 point to robust economic growth in the United States, complemented by low but stable expansion in the eurozone. We anticipate 2.6% GDP growth in the US, driven by strong labour market dynamics, robust consumption and increased investment in technology sectors. Consumer spending remains a vital driver, buoyed by rising disposable incomes and relatively low unemployment rates. At the turn of the year, global economic activity is further supported by resilient service sectors and recovering supply chains. We will monitor the latter in the coming months as they may provide an early warning sign regarding the impact of potential new trade tariffs on prices.

In contrast, the eurozone’s subdued expected GDP growth of 0.9% in 2025 reflects structural challenges, including sluggish productivity and demographic headwinds. But improving retail sales, defensive fiscal measures and targeted investments in green energy and infrastructure offer glimmers of optimism to maintain an expansion.

Equities: Slight overweight via the United States and an underweight on Europe

As a consequence, we are overall constructive towards equity markets, favouring American stocks. Even though the performance and valuation of the American stock market already reflects some optimism, the growth trajectory of the US economy and corporate earnings is much stronger and more resilient than that of other developed countries, such as Europe.

The investment and productivity gains gap compared to the United States continues to grow and the political situation in France and Germany is bogged down in partisan divisions. An attractive valuation level alone will not be enough to ensure a lasting return of investors. We acknowledge that the weakening in the Euro currency, further expected ECB cuts and low positioning has provided some support in the past weeks for European big caps.

But Europe will need to show better growth prospects, Germany will need to ease its “debt brake” and trade tensions with the United States will need to be well managed. The eurozone’s heavy reliance on industrial exports, particularly automobiles and machinery, make it particularly vulnerable to trade policy shifts. We expect these uncertainties to remain, while PMI activity indicators show difficulties and bottom out.

Downgrade emerging-market equities to neutral

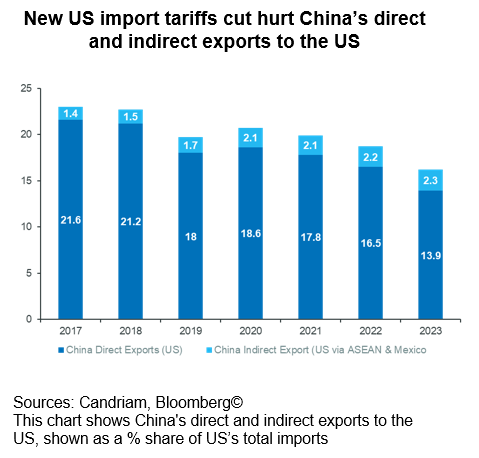

The election of Donald Trump and the Republican sweep in November 2024 has significantly heightened global trade policy uncertainty, returning it to levels above those seen during his first term. Proposed tariffs, particularly those targeting Chinese imports, risk reigniting trade wars and exacerbating geopolitical tensions. Emerging markets, especially those closely linked to China’s economy, face significant challenges as the US shifts toward protectionist policies. Tariff-related disruptions could reduce global trade volumes, weaken investor confidence and amplify currency volatility, creating headwinds for growth.

Given the evolving trade dynamics and the lack of details on monetary and fiscal stimulus before the Chinese National People’s Congress “Two Sessions” scheduled in March, we are downgrading emerging markets in our recommended allocation. New US tariffs are expected to directly and indirectly impact China’s export-driven economy, with spillover effects on supply chains across Asia. The anticipated GDP growth slowdown in China (we forecast 4.5% for 2025) highlights the challenges faced by emerging markets in adapting to these disruptions and a stronger US dollar environment.

Monitoring the Bond/Equity relationship

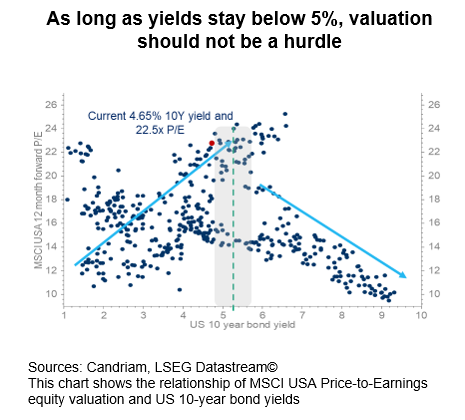

Rising bond yields, closely linked to the risk of inflationary measures via higher tariffs and lower immigration-linked labour market supply, constitute a risk to our central scenario. An outsized rise in trade tariffs could trigger a stagflationary impulse, raising inflation expectations while depressing real yields. A potential additional rise in bond yields might start posing a valuation risk for equities. While 10-year US Treasury yields remain below the critical 5% threshold, a further increase could pressure valuations, particularly in long-duration sectors including Technology. In a nutshell: the risk for US yields remains on the upside, depending on the policies of the new administration.

From a financial-conditions standpoint, the interplay between rising yields and equity market performance warrants close monitoring, as a sharp adjustment could trigger broader financial instability since markets have not forgotten that US regional banks had to mark down the value of their Treasury holdings in spring 2023. Rising term premiums in recent weeks likely reflect investor concerns over fiscal policies, inflationary risks and rising government debt. Most recent labour market and inflation data for the month of December have also illustrated the data-dependency – the tail risk of the Fed having to hike rates increased and then receded, causing sharp reversals.

Fixed income: Monetary policy divergences lead to nuanced allocation

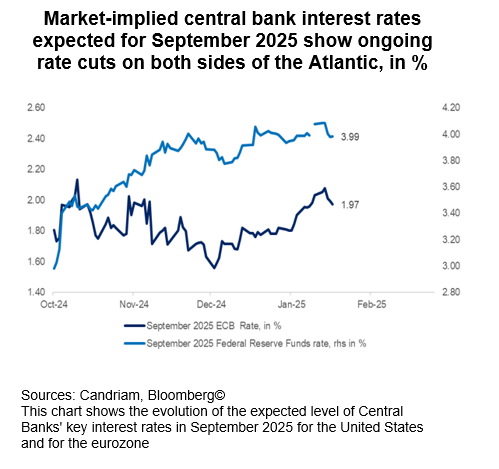

Monetary policy remains accommodative as central banks across major economies reduce interest rates. Market-implied projections indicate further rate cuts in both the US and eurozone through 2025, albeit at a different pace: this year, we expect two cuts from the Federal Reserve (Fed) and four cuts from the European Central Bank (ECB) as the growth/inflation mix evolves in opposite directions.

The Fed’s more cautious stance reflects less progress in disinflation trends, which have eased from 2024’s highs, and less effort to sustain economic activity while domestic policy uncertainties are just around the corner. The first decisions of the new US administration will be read through the lens of reducing the risk of hikes rather than a material increase in the probability of cuts. Clearly, the administration’s tariffs and immigration measures could pause the disinflation process and therefore limit the amplitude of Fed easing.

On this side of the Atlantic, the anaemic domestic situation is leading the ECB to cut out of necessity, and not by choice. The ECB’s actions are motivated by the need to counteract weak growth and persistent disinflationary forces. With short-term yields trending downward, lower borrowing costs are expected to stimulate corporate investment and consumer spending. Recently, bond markets have been influenced by the external environment of rising yields in the US. We are convinced that this presents an opportunity and hold a long German duration.

The divergence in monetary policies between advanced and emerging economies adds complexity to the global financial environment. While rate cuts in developed markets are increasing liquidity, emerging economies face tighter monetary conditions due to currency pressures and inflationary risks. This dichotomy underscores the importance of selective positioning in fixed-income markets: we are slightly long duration in Europe, slightly short in the US and have a neutral allocation towards emerging-market debt. On Credit, we remain overall neutral on Investment Grade and High Yield, as spreads are tight while very few defaults are expected to occur.