April 2025 marks a turning point in the global economic narrative. In the wake of the United States’ sharp tariff escalation – dubbed “Liberation Day” – investors are confronting the ripple effects of a protectionist revival. These tariffs, presented as trade remedies, represent in effect a new tax burden on American households and corporates. The average tariff rate on US imports is now around 20%, up from 2.5% at the end of 2024. We identify this as a key macro pivot, setting the stage for a reassessment of risk across asset classes, geographies, and currencies. We are therefore recalibrating our multi-asset strategy. The US is now at the epicentre of policy uncertainty and economic risk, while Europe emerges as a relative safe haven, bolstered by proactive fiscal measures. Our asset allocation reflects these divergences: long core European sovereign duration, underweight mainly in US equities within an overall underweight equity stance, cautious on credit, and opportunistic in FX and gold.

Liberation Day: Three Shockwaves

The introduction of sweeping US tariffs is transmitting economic strain through three dominant channels:

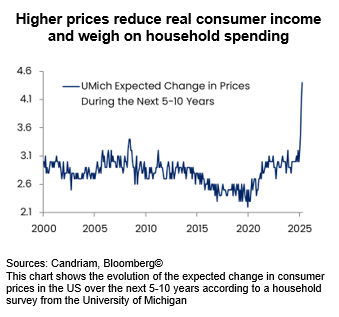

- Higher Prices: These tariffs are inflationary by nature, particularly for import-intensive sectors. Input costs are rising across pharmaceuticals, autos, and metals, reducing corporate profitability and household purchasing power.

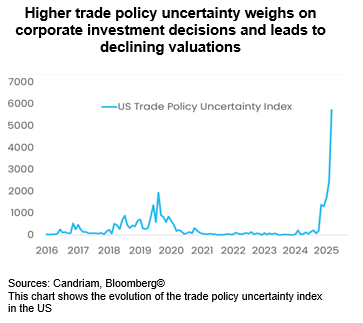

- Higher Uncertainty: The lack of clarity and frequency of policy shifts is freezing capital allocation decisions. Firms are delaying investment, inventories are misaligned, and global supply chains face renewed disruption.

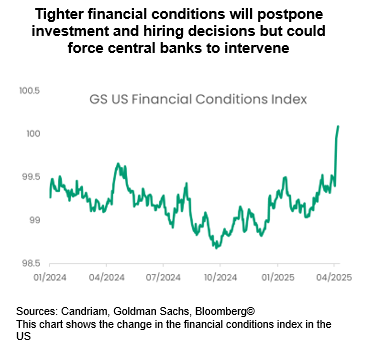

- Tighter Financial Conditions: As falling markets price in weaker growth and volatile earnings, financial conditions are tightening. This is evident in widening credit spreads, steepening yield curves, and risk-off moves in equity and currency markets.

Together, these forces are eroding confidence and reinforcing the likelihood of a US-led economic downturn. “Trumpcession” fears are further on the rise compared to last month.

Tax Americana in Motion

The administration’s erratic approach on the enactment of new tariffs on US imports took markets by surprise and currently leaves us with more questions than answers. We have nevertheless identified several areas of risk which call for close monitoring in the crucial period we have now entered.

- US Growth Deterioration: Our base case now expects US GDP to decelerate markedly from 2.8% in 2024 to 1.4% in 2025 and 0.4% in 2026, as tariffs, a fiscal drag, and weak private investment converge. The labour market, though still resilient, is softening. Consumption is slowing, and leading indicators such as ISM business surveys and consumer sentiment have turned sharply lower. The tariff-induced drag is particularly visible in sectors linked to global trade and in consumer-sensitive industries now facing margin compression.

- Earnings at Risk: Corporate guidance for 2025 is being revised downward, particularly in tech and industrials. Stock selection in US equities will be paramount as tariff-induced margin compression and uncertain fiscal outlooks weigh on business confidence. Meanwhile, investors should brace for lowered forward earnings estimates, with a particular eye on sectors most exposed to import costs and supply chain volatility.

- Credit Fragility: High-yield credit spreads, both in the US and Europe, have widened. We continue to view high yield as the weakest link in the fixed income space. We expect fundamentals to deteriorate significantly as policy-driven sentiment shifts may catalyse further stress and lead to credit events. In the US High Yield segment, the large part of issuers belonging to the commodity complex could represent an additional drag as the price of oil has been falling sharply. Our cautious positioning is reflected in underweight allocations to both US and European high yield, as well as to emerging market debt. Conversely, a longer duration positioning in German Bunds has remains justified by longer-term disinflationary forces and as one of the rare safe havens.

- Geopolitical Fragmentation: Undoubtedly, the US-China rift has deepened. China’s retaliatory measures – including rare earth export restrictions and import licensing – highlight the systemic risks of prolonged trade wars. Canada has also responded in kind, escalating tensions. These developments compound uncertainty and inhibit global trade flows, particularly affecting the integrated North American and Asian manufacturing ecosystems.

- Commodities and Currencies: Industrial metals and oil have declined, reflecting weaker demand expectations while Gold continues to be a key beneficiary of the flight to quality. Opportunities exist in currencies like the Japanese yen (JPY). In our thinking, the yen, in particular, remains a critical portfolio hedge amid rising volatility.

Opportunities Amid Dislocation

“Tax Americana” encapsulates this new environment – a world where economic policy unpredictability intersects with tightening financial conditions and geopolitical fragmentation while imposing higher costs on US households and corporate. Our allocation choices reflect a disciplined, forward-looking approach. With recession risks climbing and risk premia expanding, we maintain a defensive positioning while selectively embracing duration, defensive equities, and alternatives. Tactical currency and commodity exposures provide necessary flexibility as we navigate this volatile terrain. As global markets digest this protectionist pivot, active and nimble portfolio management is essential; we are entering Q2 2025 with resilience, prudence, and a sharp focus on fundamentals. The overarching themes in our portfolio construction can be summarised as follows:

- European Fiscal Anchor: In contrast to the US environment of new tariffs and fiscal uncertainty, Europe is embracing proactive fiscal expansion. Germany’s EUR500bn infrastructure plan and rising defence budgets across the EU are major tailwinds which should mitigate somewhat the hit to EU growth. These initiatives are driving up earnings expectations, particularly for mid-cap industrials and defence-linked equities, and could provide some support to European assets which have started to diverge positively from US peers in 2025.

- Sovereign Duration and Policy Divergence: Core European bond markets offer an attractive duration play. With inflation trending lower and the ECB expected to ease monetary policy further, Bunds and other core sovereigns remain in focus. Our long position in German Bunds, despite short-term volatility, remains a cornerstone allocation. In the US, while market expectations are now tilted toward several rate cuts as growth fears dominate monetary policy expectations, we remain more cautious.

- Defensive Equity Tilt: We continue to prefer sectors with pricing power and stable dividends – healthcare in the US, utilities and consumer staples in Europe. These sectors have provided insulation amid broader equity declines. Despite reducing overall equity exposure, we keep a neutral stance on European equities ex EMU on the back of earnings revisions.

- Currencies: We retain a constructive stance on long-term thematic investments such as climate transition, robotics, and biotechnology – despite near-term corrections. Currency-wise, we maintain tactical overweight positions in the JPY, which has demonstrated resilience and is supported by fundamentals and policy divergence.

- Commodities – Gold as Hedge: Gold has become a reliable hedge amidst growing stagflationary pressures and geopolitical instability. We view it as a structural allocation in the current regime.

- Alternatives and Market-Neutral Strategies: In light of persistent volatility and asymmetric market risks, we keep our allocation to market-neutral and alternative strategies. These approaches provide portfolio ballast and complement more traditional and directional exposures.