European equities: Another rough month

European equities had a rough month of it, with the increases in cases outside China leading to a sharp sell-off and economic uncertainties. The outbreak in Europe caused governments to lock down the zone in order to slow the spread of the virus. Equities pared some of their losses in the last week of the month after governments and central banks responded to the outbreak through large monetary and fiscal stimulus packages.

European equities had a rough month of it, with the increases in cases outside China leading to a sharp sell-off and economic uncertainties. The outbreak in Europe caused governments to lock down the zone in order to slow the spread of the virus. Equities pared some of their losses in the last week of the month after governments and central banks responded to the outbreak through large monetary and fiscal stimulus packages.

As the evolution of the virus will remain the main market driver over the coming weeks, European investors are closely monitoring changes in its different phases.

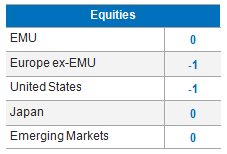

In our main scenario, we maintain the idea that the pandemic will result in a global, deep, but temporary, shock. It will probably take more time than initially thought for “normal” levels of activity to be resumed. Nevertheless, from a long-term perspective, European equity markets still offer value and represent upside potential.

Energy and Healthcare were the best performers during the month. Coronavirus continues to cause a flight to safety in favour of the Healthcare sector. Energy outperformed as oil prices rebounded. Mechanically, Financials underperformed as economic activity slowed down.

We see strong dispersion in Europe through different sectors. Financials, Transportation and Leisure sharply underperformed and continue to lag during the current rebound. On the other hand, Energy, which had also strongly underperformed during the first correction, is now the best performer of the current market rebound. Utilities, which proved to be very resilient during the correction, has started to lose its gains, with investors focusing on the significant debt level.

Value is attractive :

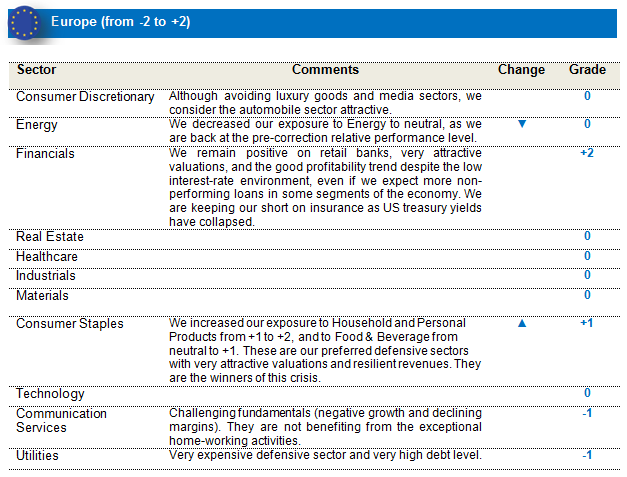

In terms of style, Value continues to underperform, with the extreme price discounts offering very attractive entry points. Supervisors called for dividend cancellations in 2020, and banks obliged; in response, many “Dividend Strategy” funds sold their stocks, which explains the current valuations. As a result of these very attractive valuations, we are keeping our strong conviction on retail banks. We'll closely monitor the performance of the Value style as the market recovers over the coming weeks and months. We expect a significant rebound of this style in the coming weeks.

We decreased our exposure to Energy to neutral, as we are back at the pre-correction relative performance level. In the meantime, the battle for market share between Saudi Arabia and Russia is a new element compared to 3 months ago, when we upgraded the sector. Oil prices may stay low for a long time. The only positive we see is the cash flow generation, thanks to massive CapEx cuts. On the other hand, we increased our exposure to Household and Personal Products from +1 to +2 and Food & Beverage from neutral to +1. These are our preferred defensive sectors, with attractive valuations, resilient revenues and returns to shareholders. They are the clear winners of this crisis.

We increased our exposure to Household & Personal Products as the sector, even though under-owned, is rather attractive. We neutralized our grade on the Healthcare sector in view of the exceptional health situation. We are keeping our strong overweight exposure on retail banks based on very attractive valuations and a good profitability trend despite the low interest-rate environment. We are also keeping our underweight on insurance, as US treasury yields have collapsed. Finally, we are keeping our slight overweight on energy, as current stock prices are already discounting the longstanding low oil prices.

US equities: Negative earnings revisions

US equity markets had a rough month of it, with US equities and US 10yr yields dropping significantly. The sole culprit: covid-19. The impact on the world economy will be bigger than first estimated, and that is why all central banks and governments have taken strong action to avoid a long-lasting and deep recession.

Earnings revisions are negative, and it's not over yet, as analysts are only just beginning to understand and integrate the consequences of the crisis into their analyses. The market is closely monitoring the evolution of the different phases of the virus (Increase/Stabilization/Decrease in the number of cases) in order to find the right momentum to return to risky assets. We saw strong equity outflows in the US throughout the month, as investors feared an economic crisis, depending on the duration of the containment.

No sectors were able to avoid the correction, with defensive sectors such as Healthcare, Consumer Staples and Information Technology clearly not faring as badly as the Energy, Financials and Industrials sectors. Quality stocks were the best performers, while small caps were the worst detractors. Information Technology also outperformed, as new technologies play an important role in the fight against the virus.

We see strong dispersion, though sectors as Financials sharply underperformed and continue to lag during the current rebound. On the other hand, although Energy and Automobile also strongly underperformed during the first correction, they are now the best performers of the current market rebound. Utilities, which proved to be very resilient during the correction, have started to lose their gains.

In terms of healthcare subsectors, pharmaceutical companies, life science tools and services companies held up very well, while healthcare technology suffered the most, as elective procedures, services and equipment purchases are being postponed. Performance in the biotech segment was intermediate, with a large dispersion within that segment. In general, the larger capitalizations within biotech with solid commercial franchises held up best, while there was some risk-off trading in the emerging biotech companies. The logic being very clear, the impact on essential medicines will be limited to non-existent, but there will be greater impact on launches of new drugs as sales reps cannot visit the doctors. In addition, recruitment in clinical trials is mostly suspended, leading to delays. Overall, this has led to some shift in timelines but no dramatic changes in outlook, with the key risk to monitor here being companies with financing needs.

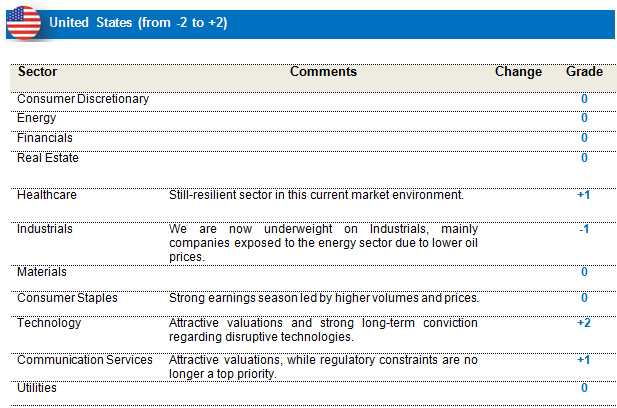

Although most of our bets paid off – as we were overweight Healthcare, underweight Industrials and strongly overweight Information Technology.

We are keeping our strong overweight on Information Technology due to attractive valuations and strong long-term convictions regarding disruptive technologies (home-working, 5G, cybersecurity,…). We have also kept our overweight on Communication Services exposure, based on attractive valuations, while regulatory constraints are no longer a top priority, given the current economic context. Finally, we are keeping our positive exposure on Healthcare, as the sector is rather defensive in the current market environment.

Emerging equities: One of the worst first quarters, historically

The global market correction that intensified in February due to the outbreak of the Covid-19 virus outside of China turned into a fierce bear market in March as the virus-spread grew into a global pandemic and, together with the oil-price collapse, resulted in an unseen sudden global economic stop, triggered by huge personal containment and quarantine measures, production stoppages and travel bans, hitting supply and demand at the same time.

While China, Singapore and South Korea managed to contain the virus spread, Italy, Spain and, later, the US were heavily impacted. Global financial markets collapsed, with huge volatility, while unprecedented monetary and fiscal support measures were announced to contain the healthcare and economic damage.

In this environment of expected global recession, deflation and severe earnings downgrades, emerging markets as an asset class continued to underperform, with all markets and sectors losing, but with strong dispersion between markets.

While north Asia (China, followed by Taiwan and South Korea) clearly outperformed, mainly due to more solid fundamentals, a higher exposure to technology and a prompt containment of the virus outbreak, markets and currencies of more fundamentally weak economies (Indonesia, India, Turkey) and commodity-dependent markets (Brazil, Russia) suffered strongly.

Sector-wise, in this environment, not surprisingly, defensive sectors like healthcare, communication and technology-driven stocks strongly outperformed cyclical sectors like financials, energy and commodities. The current correction ushered in not only one of the worst months, but also one of the worst first quarters, historically.

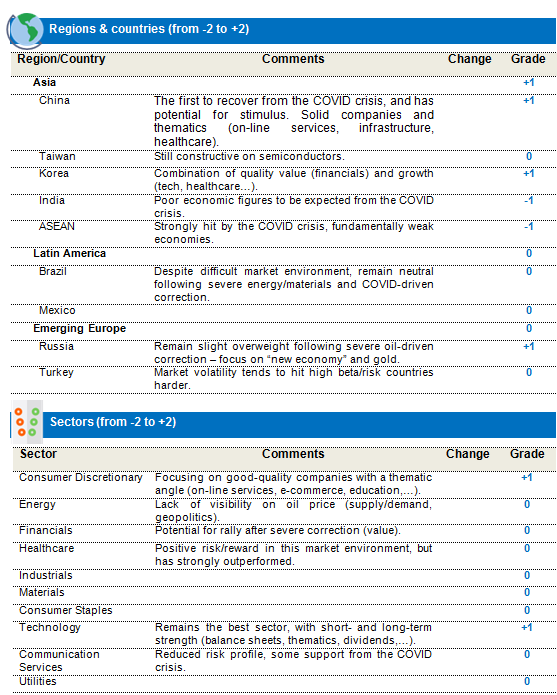

We remain constructive on north Asia (China, Korea, Taiwan) as the strongest (fundamentally) regional economies to have come out of the COVID crisis first, as well for their potential for fiscal and monetary stimulus and high exposure to technology and thematic stocks (healthcare, stocks linked to on-line services (e-commerce, cloud, networking, e-banking, etc., infrastructure investments, …). Nonetheless, the risk of a virus re-appearance remains.

We remain underweight ASEAN and India, both (fundamentally weaker) economies severely hit by the impact of the COVID-related crisis.

We remain neutral Brazil, following the severe correction in March. We are focusing on solid companies that have corrected strongly.