Our convictions have evolved with the recent overcoming of 2 major hurdles: the US elections and the announcement of an efficient vaccine. Our strategy has, in turn, evolved towards a more risk-on approach that includes not only a slight equity overweight in specific regions and sectors, but also riskier bonds. There is a positive assessment for European and emerging equities, value sectors such as banks in both Europe and the US, and US small caps. European and US Investment Grade bond, as well as riskier bonds such as emerging debt and convertible bonds, are enhancing the strategy. While we may expect financial markets to integrate this rather good news in successive waves, medium-term perspectives are undeniably improving and will continue to do so, provided the vaccine truly turns out to be a game-changer.

Main hurdles

October was marked by a peak in stress, impacting global financial markets and triggered mainly by:

- the tight US presidential race;

- the increasing number of corona virus infections in Europe and in the US.

Hurdle 1: the US presidential elections and their implications for financial markets

The US presidential race ended early November, with millions of Americans going to the polls to cast their ballot. Democrat Joe Biden is now President-elect and will be inaugurated as the 46th president of the United States of America early next year.

President-elect Biden inherits a country that is deeply divided after a very polarized race to the White House. Voter turnout was the highest since 1900 and, although incumbent president Donald Trump received more votes in 2020 than in 2016, this was still not enough to secure a second term in the White House.

Joe Biden won but without a blue sweep. Democrats should retain their majority in the House, albeit a thinner one. It is also not known which party will control the Senate. It looks as though Democrats will have 48 seats and Republicans 50. That leaves the two Senate seats from Georgia to determine control of the Chamber. There will be a run-off election early January 2021. If Democrats win both seats, that will give them control of the Senate. If not, then we will have a divided government, with a Democratic majority in the House and a Republican majority in the Senate.

Joe Biden immediately vowed to bring the country together but, without a majority in Congress, his ambitious Build Back Better programme will be hard to implement. More pressing is the much-needed sustained fiscal support to the economy. In the shorter term, the lame duck Congress should at least vote a continuing resolution before December 11. It could also agree to extend supplemental unemployment assistance programmes, which end on December 31 and provide minimal help to States that are about to run out of resources. But the current President may push his executive and constitutional powers to the limit and beyond to pursue a different agenda.

Seen from abroad and from a global perspective, the election of Joe Biden is good news. American policy should reconnect with multilateralism and political risk should structurally be reduced. Joe Biden has vowed to reconnect with the world, place Asia back at the centre of foreign policy, and end Trump´s promises to put “America First”.

Global financial markets reacted positively to the news.

Hurdle 2: the vaccine

The coronavirus breakout put us all in unchartered waters. First, it was a breakout in some distant Chinese town called Wuhan, but rapidly it spread and the WHO declared a pandemic. Some countries decided to aim at and wait for herd immunity. Others decided to follow China´s example and impose social distancing measures and more stringent guidelines: mask-wearing, curfews, mobility restrictions. Rapidly, pharmaceutical companies aimed for a vaccine. Finally, it looks like we are getting really close to one, and thereby a possibly definitive solution to the spread of the coronavirus.

Pfizer and Moderna both quickly outpaced their competitors and now, in their last trial phase, are likely to obtain the necessary authorization from the US Food & Drug Administration to manufacture and distribute their newly found vaccines,.

Pfizer recently reported that its COVID-19 vaccine candidate had achieved a 90% efficacy on the first 94 subjects in its trial. Moderna must be close behind with its own vaccine candidate. With the higher vaccine efficacy rates also comes the increasing likelihood of a faster return to the economic activity levels of early 2020, before the breakout.

Acting as a shield against the justified second-wave worries, the news of an imminent vaccine is supporting global equity markets while making a dent in safe havens.

As we move closer to 2021, the very idea of getting the pandemic under control in this new year is reason enough to think that we are moving towards better auspices. There is, however, at least one last hurdle.

Hurdle 3: Brexit

Brexit is, hopefully, the final hurdle as we approach the new year. Negotiations recently resumed in the UK and, since last week, the tone has seemed to be changing/softening. The UK Foreign Secretary is no longer talking about “Red Line” boundaries but is, rather, increasingly voicing a “Meet us half-way” rhetoric.

On the European Commission side, Michel Barnier is said to have been openly talking about the kind of fisheries compromises that will be needed. It now seems a question of bartering over quota allocations along with a review of frequency. Still, significant outstanding differences include:

- fishing rights;

- ensuring a level playing field; and

- the long-term implementation of the Irish Protocol.

There are still three possible scenarios for the post-transition period:

- a Comprehensive Agreement; or

- a World Trade Organization-type Brexit; or

- the more-than-likely possibility of an Economic Partnership (55%), i.e. an agreement on quota-free/tariff-free goods Free Trade Agreement (FTA).

With Joe Biden winning the US elections, UK Prime Minister Boris Johnson has definitely lost some grip on the Brexit negotiations, as Biden – unlike Trump – has already expressed his support for a Brexit under the condition that it upholds the Good Friday Agreement.

In addition, Joe Biden has already warned Boris Johnson that there will be no chance of a UK-US trade deal if Brexit undermines the Northern Ireland peace process, as, indeed, had Nancy Pelosi and the US Congress already two months ago. Whether Boris Johnson can persist on a collision course with both Mr Biden and the EU is unlikely.

Assuming that Brexit turns into an FTA deal, the financial market implications are rather positive.

The GBP should rerate, UK equities should outperform the market and, due to its lower exposure to foreign revenue, the FTSE 250 should outperform the FTSE 100.

Our current multi-asset strategy

Our multi-asset strategy is currently based on a barbell as we reinforce, on the one hand, what could benefit from a better news flow towards re-opening economies while, on the other, remaining convinced that there are long-term winners from the sanitary crisis who will remain the core of our portfolio. These include long-term thematics such as sustainability, technology and healthcare.

In the near term, riskier assets will benefit from 1) an exit from the pandemic becoming a reality, 2) fiscal stimuli to support economies and their stronger rebound, and 3) long-term accommodating financial conditions.

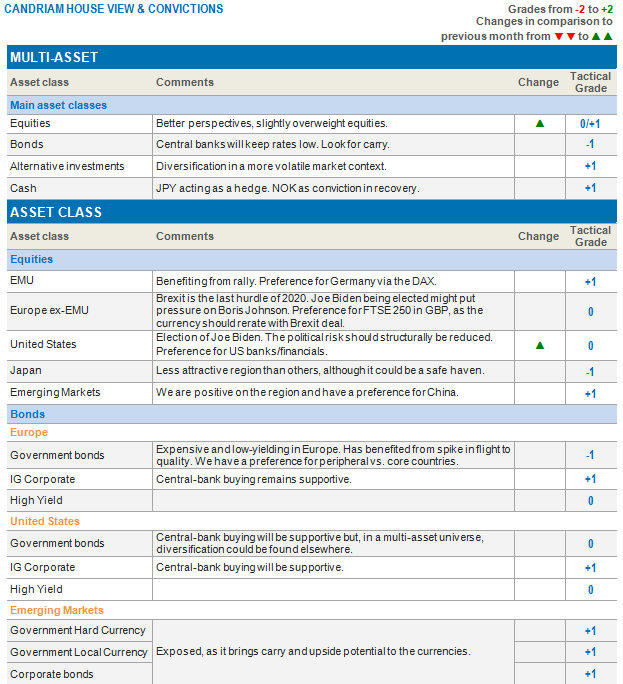

In practical terms, our multi-asset strategy is slightly overweight equity.

Getting past two hurdles with such promising outcomes has led us to slightly overweight our equity exposure.

Within the equity weighting, we remain overweight European equities, with a preference for the German equity market. Because a Brexit Free Trade Agreement is the most likely outcome, our strategy will gain in exposure to the British FTSE 250 in local currency.

We remain neutral US equities and, in our sectorial allocation, have added to US banks specifically, as the sector still offers very attractive valuations and should also be boosted by the important news on the vaccine.

We remain overweight emerging market equities, with a preference for Chinese A-shares, while remaining underweight Japanese equities.

Within fixed income, the strategy, being more risk-on, has led us to increase our exposure to convertible bonds.

Our bond allocation stays otherwise stable and positive on credit Investment Grade (Europe and the US) and emerging debt.

We also maintain a short duration bias, an underweight exposure to government bonds in Europe (on core countries) and an overweight in peripheral European bonds.

Our currency allocation is short USD vs. EUR, short USD vs JPY and long NOK vs EUR.

Risks remain present but seem limited. We do not exclude the possibility of the vaccine hitting a road bump in the manufacturing or distribution process or even in its acceptance by the population. Also, current US president Trump´s refusal to accept his loss puts the transition work towards a Biden presidency on hold.