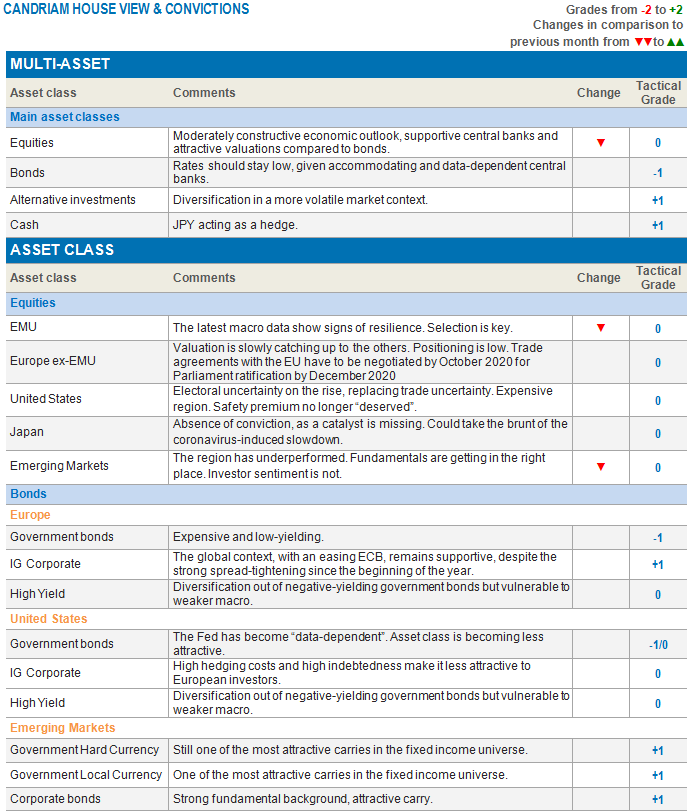

Leading indicators stay on course but the news flow could weigh on investor sentiment. Mixed messages include a performing US equity markets but decreasing oil prices and yields. As an asset manager, it is important to remain cool-headed. Here is how we have designed our asset allocation strategy to navigate the unchartered waters ahead.

Equities vs. bonds

In the current environment, dominated by the coronavirus news flow, the epidemic reaching a peak and other news fading into oblivion, some equities valuations continue to become more expensive -- and so are bonds.

As asset managers, we continue to believe in a moderately constructive medium-term scenario as leading indicators continue to strengthen, rates remain very accommodative, the economy steers clear from recession, and expected returns are positive -- albeit expectations are lower than in 2019.

The surge of the coronavirus might be a blessing in disguise, that could contributes to a prolongation of the economic cycle and a rather equities-friendly environment. Inflation is barely present and central banks are in chronic Quantitative Easing mode or “QE forever”.

Nonetheless, we are currently neutral equities and underweight bonds as the market catches its breath. January’s global PMI’s, manufacturing PMI’s and the global OECD Leading Indicator are confirming the upturn but the breakout of the coronavirus is jeopardising Q1 economic activity and earnings.

Equities

US: expensive but leading

While US equities are a core holding, valuations have become very expensive. The market is currently leading global equity markets. The labour market is strong. The January US job report surprised again on the upside. The country added a much stronger-than expected 225K in non-farm payrolls. The unemployment rate grew to 3.6%, but labour force participation also grew, to 63.4%. The weather-sensitive construction industry contributed the most, thanks to a mild winter in many parts of the US.

In addition, Jerome Powell, Federal Reserve Chairman, confirmed in his last monthly testimony to Congress that the US economy is healthy, and that the current stance of policy and interest rate is conducive to supporting growth.

However, the Fed continues to monitor the coronavirus for its impact on both China and on the global economy.

Another source of uncertainty that will likely impact the US economy, equities and sectorial rotation is the race for the White House. Across the US, voters will head to the polls on November 3rd to re-elect incumbent Republican president Trump or replace him by another candidate. The first state primary leading to the choice of the Democratic candidate, the Iowa Caucus, was chaotic. No clear winner emerged for a week after the event. US president Trump saw his approval rate increase while Democrat Michael Bloomberg gained in credibility and popularity, although he was too late to be listed in either the Iowa Caucus or the New Hampshire primary. Next is the Nevada Caucus on February 22nd.

Between the high valuation, US equities already being a core holding, the increased electoral uncertainty, our positioning on US equities is therefore currently neutral, as it has been since mid-December.

Europe: selection is key

The wide gap between euro zone and UK equities performances is closing in as UK equities are catching up. Both regions can show positive earnings revision for the Q4 2019 season. Upcoming earnings growth is expected to be positive in 2020, more so for the euro zone than for the UK as the region has yet to negotiate trade agreements with the European Union and implement the long-awaited Brexit.

Nevertheless, flows are negative and investors that do maintain their exposure, are very selective.

Our positioning on European equities is overall neutral, regardless of the region, but selective with respect to investment style and sector.

Our thematic allocation draws on opportunistic investment and long-term convictions. Opportunistic allocation choices include value-style investments, such as banks, which have lately shown resilience, and UK domestic assets.

Our long-term convictions target underlying growing markets, a competitive edge in a low-growth world. They include climate action equities, infrastructure, robotics and cancer cure-related investments.

Emerging markets: (hyper-)mediatized coronavirus?

The coronavirus that broke out in the Chinese town of Wuhan has definitely put that town on the map. The severe flu-like disease has spread to other countries in spite of China displaying strong crisis management skills. How much damage can it cause?

It is hard to assess. A similar contagion occurred in 2003/2004 with the epidemic of SARS. However at that time, China represented only a single-digit percentage of the world’s economy. China has since become a major player, and that player is forced to slow down and put an immediate halt to trivial activities, disrupting supply chain management, transport, and consumption.

In addition, the epidemic happened at one of the worst possible seasons: the new year’s holiday, a period that usually boosts private consumption and corporate revenues.

Financial markets are reacting with mixed messages. On the one hand, oil prices dropped as the market anticipates less demand, and yields dropped as investors fled to quality, pushing bond prices up. Conversely, some equities performed reasonably, in euro terms and local currency. This has been the case for US and European equities. Emerging markets, UK and Japanese equities performed the least well.

Short-term noise or long-term derailment? We believe that markets are efficient and that once we get past the disappointing dip in activity of the first months of the year, it will be business as usual.

Until then, we expect Chinese authorities shall further use monetary and fiscal policy tools to support the economy, including injecting liquidity into the system.

Our positioning has recently become neutral emerging markets equities.

Bonds and currencies

Our underweight government bonds stance continues. Low-yielding sovereign bonds are not the only segment available to investors. Instead, we focus on higher-yielding asset classes, such as corporate debt of EUR-based companies.

We are still overweight emerging markets debt.

In the currency universe, we remain long JPY as a hedge.

We also have an exposure to gold, which we believe remains an attractive hedge in the current context.