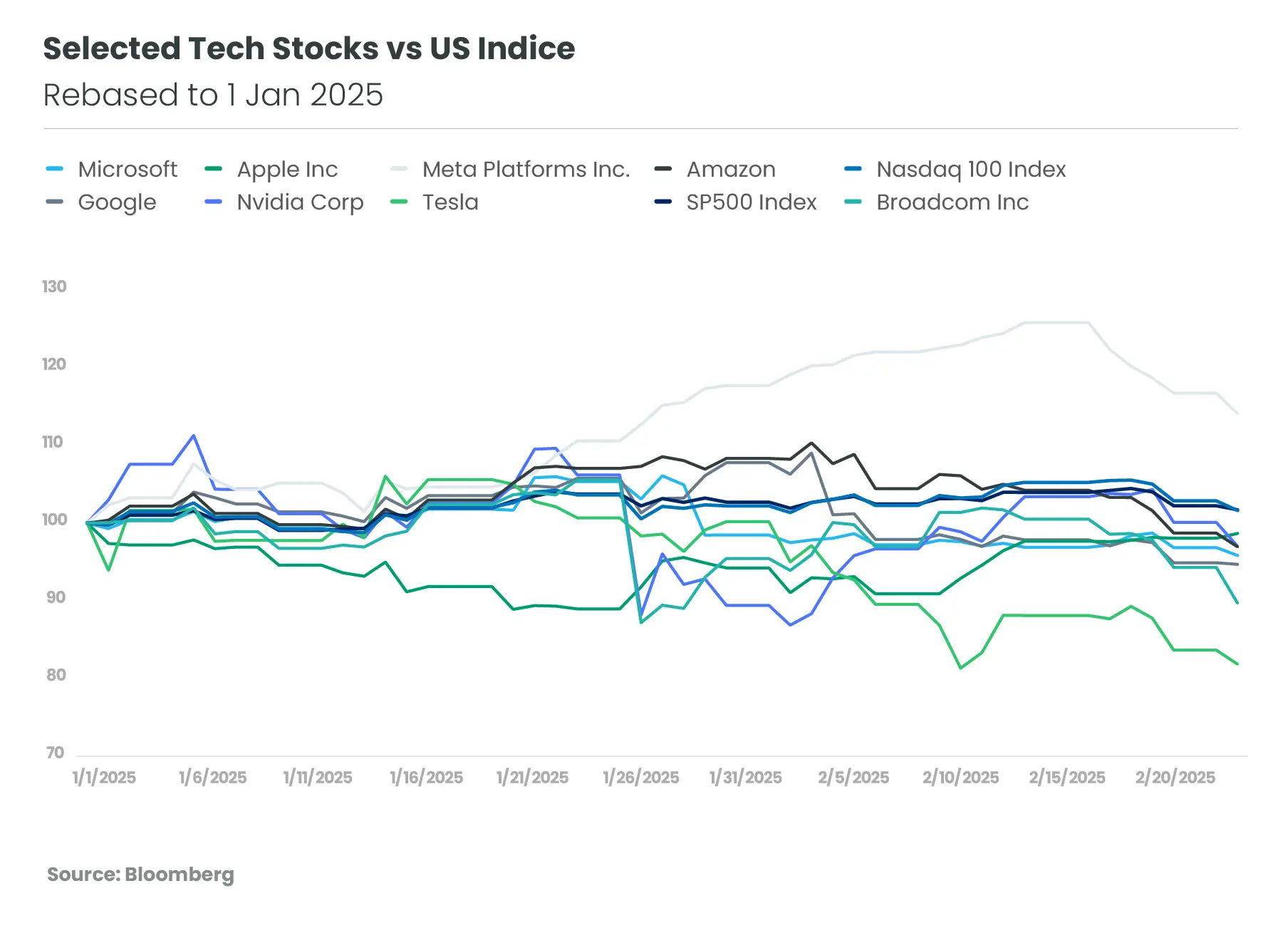

For the past decade, US stock markets have largely dominated the rest of the world, thanks to strong momentum in the technology sector and a favorable macroeconomic environment. Paradoxically, since the election of Donald Trump, this trend has reversed and the US market seems to have temporarily lost this leadership role. As of February 25, 2025, the Nasdaq 100 remains very close to its start-of-year level, while all the "Magnificent 7" names,[1] excluding Meta, are posting declines. Tesla shares, down over 20%,[2] illustrate the end of the "Trump effect" on the US market.

As a result, investors are re-evaluating their investment strategies this year, with a new focus on European equities and those from emerging markets such as China. This trend is supported by an analysis of flows in January 2025, which shows a clear slowdown in investment in US equities, particularly in the tech sector, to the benefit of Europe (with the exception of the UK). China has also been attracting investors since the DeepSeek announcement, with foreign investors buying Chinese technology stocks and abandoning India.

After a phase of extreme pessimism on the European market in the aftermath of the US election, the dynamic has reversed. The valuation of European equities is significantly below that of US equities. The price/adjusted earnings ratio by sector in Europe is 23% below that of the United States, well above the historical average gap. Furthermore, the diversification of European markets contrasts with the strong concentration of US markets around the tech giants. Europe's financial markets are now more evenly distributed among the financial, industrial and consumer goods sectors. The European context remains fragile and vulnerable, both politically and economically. However, in the short term, the end of the conflict in Ukraine, the stabilization of energy prices and fiscal easing in Germany are all potential positive surprises attracting investors. Supported by a more accommodating ECB, the European economy is also showing signs of improvement, notably in manufacturing and construction, while credit conditions are improving.

In the longer term, the United States still has major advantages. Innovation remains their main driver, particularly in technology and artificial intelligence, which offer long-term growth prospects. American companies stand out for their higher profitability than their European counterparts, driven by better capital allocation and a more dynamic economic environment. It's probably far too early to call for an end to American exceptionalism. This is reinforced by the fact that geopolitical and economic risks depend to a large extent on US political decisions, against which stock markets appear to be the main bulwark for the time being.

Against this backdrop, we recommend a more balanced investment strategy: One between the US and European markets. Such diversification should enable us to better manage risks and seize opportunities specific to each region. We have increased our exposure to European equities, particularly in undervalued sectors such as finance, industry and German midcaps. However, we maintain a core allocation to US equities, which remains necessary due to their structural advantages.

all the data as of 24.02.2025.

[1] Defined as Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia, Tesla. Source of definition: US News, 7 January, 2025.

[2] “Tesla's performance is mentioned here for illustrative purposes only and should not be considered as an investment recommendation or an indicator of future market trends”