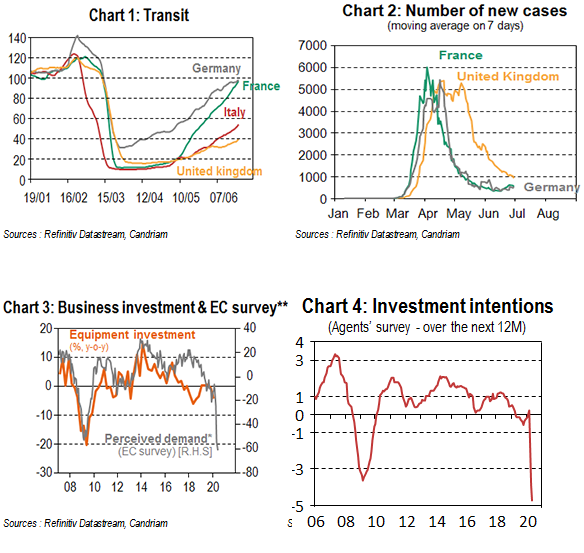

Following a record fall in GDP in April 2020 as a result of the Covid-19 lockdown, the UK economy is expected to experience one of its deepest recessions in modern times. A similar economic shock was observed across Europe due to the pandemic. However, the slower easing of lockdown measures in the UK has resulted in a slower economic recovery in comparison to impacted European countries, most notably Germany, France and Italy, which lifted lockdown measures more rapidly (Charts 1 and 2).

According to the Q2 2020 Summary of Business Conditions[i] report compiled by the Bank of England’s regional agents, UK businesses remain cautious about their growth path. Companies surveyed do not expect sales, employment or investment to return to normal before the end of 2021. The government’s support plan for jobs[ii] announced on 8 July will help the recovery, but corporate investment behaviour will continue to curb it. Demand remains depressed and the uncertainty generated by Brexit is also impacting businesses (Charts 3 and 4). The recovery should therefore remain very gradual. On average UK GDP is expected to contract by more than 10% in 2020.

In addition to the uncertainty around the future of the pandemic - a second wave cannot be ruled out – the outcome of the Brexit negotiations will also impact GDP growth in 2021. At the end of June, the UK government indicated that it would not ask for an extension of the transition period beyond 31 December 2020. Given the ratification process, the challenge today is therefore to conclude the negotiations with the European Union by October at the latest. At the moment, however, negotiations are still stalled on several key issues: the role of the European Court of Justice, ensuring a level playing field and the right of EU vessels to fish in British waters.

If both the European Union and the United Kingdom refuse to make concessions, the UK would leave the EU without an agreement and revert to the rules and tariffs set by the WTO. This would result in an additional economic shock to an economy already crippled by the coronavirus pandemic. The economic consequences for the UK could be substantial, with GDP not returning to its pre-crisis level for a few years to come.

* Composite indicator (0.7 x industry production trend + 0.3 x services recent evolution in demand)

** The scores indicate how investment intentions are behaving on a scale of -5 to +5.

[i] https://www.bankofengland.co.uk/agents-summary/2020/2020-q2

[ii] https://www.gov.uk/government/publications/a-plan-for-jobs-documents