Can we find investment opportunities in the capital structure maze?

Introduction

Conflicting or competing regulatory regimes on both sides of the Atlantic, a changing rates environment with central banks in easing mode, and consolidation are the new trends to watch in the European banking sector as we head into 2025. Select carefully and keep an eye on the emissions.

Three challenges in 2025: Basel IV, Rates, and Ongoing Decarbonisation Risks

There are many shifting pieces to the banking landscape kaleidoscope. Regulation is in question, profits may be under pressure, but some modest good news is that banks are becoming aware of the risk of carbon exposure. As banks fundamentals are sound up to now and bank equities have performed, a few opportunities may be found at the lower part of the debt capital structure.

Basel IV, or not?

Starting with the recent election of Donald Trump may create some hope of deregulation, particularly in the US. (“Hope”, of course, depends on one’s view of near-term profit versus medium-term risk.) This may push other European regulators to reconsider their structures, in an effort to maintain competitiveness in their own regions. We have already seen some discussion about reducing the information required in IPO prospectuses in the UK.

The elephant in the room, the implementation of Basel IV, is to begin in 2025 and be fully in place by 2033. Should the US decide not to adopt this suite of regulations in full, the US global systemically important banks would avoid the extra 9% burden on their risk-weighted assets, and would be free to distribute more capital to shareholders. Another potential weakening of regulation, the possible watering-down of the Fundamental Review of the Trading Book, could increase the competitive advantage of the European corporate and investment banks.

It remains to be seen how far regulators are willing to lighten regulation less than two years after the US regional banks crisis that triggered the fall of Credit Suisse. We expect the ECB to keep a strict stance creating an uneven playing field for European CIBs.

Rate cuts?

The main threat to bank investing for 2025 is the rate cycle, with the ECB embarking on rate cuts to bring interest rates closer to 2% by the end of 2025, particularly after the November PMI figures. We estimate that every 50 bps rate cut could reduce net interest income by 3% for the European banking sector, and reduce net profits by 5%. While market expectations for rates are coming down, some management targets are becoming less and less realistic as recently outlined by Unicredit CEO Andrea Orcel.[1]

ESG - Bank decarbonization targets?

One of the most pressing and material risks, both near-term and long-term, is bank decarbonisation targets. A detailed analysis by the UN-convened Net Zero Banking Alliance (NZBA) determined that among the 30 largest banks, most of the existing decarbonisation targets are irrelevant – they are unlikely to achieve the rapid emission reductions that the economy needs and must be re-designed.

Specifically, current targets based on financed emissions (from lending) and facilitated emissions (from capital markets activities) are based on ratios, instead of ceilings. Consider a US bank energy intensity mix target which covers oil, gas and clean energy. This calculation can be met by increasing finance for clean energy, without reducing financing of oil and gas.

While banks are not where they need to be on decarbonisation, they are slowly tackling this material risk issue. Since its launch in April 2021, membership of the Net Zero Banking Alliance has more than tripled from 43 to 144 banks. When a bank joins the NZBA, it independently and voluntarily (it is not a regulatory obligation) commits to transition its financing activities to align with pathways to net zero by 2050 at the latest, and to set intermediate sectoral targets for 2030 or sooner to put it on a path towards this goal[2]. This demonstrates a growing interest in joining the Alliance, indicating that banks view transition away from fossil fuel financing as a material goal.

Further, banks are bringing more sustainable investments to the heart of their strategy, by setting green financing targets for 2030 and publishing transition plans. However, we expect banks to reduce their exposure to high-emitting industries and further increase their share in green financing.

Those very few banks which might leave the Alliance in 2025 will likely do so because of failure to reach the milestones set up by the group, not because of political pressure. While we may continue to see “greenhushing” in the US, banks which are aware of the risk will not change their strategy just because of the new administration.

Finding the right part of the banking capital structure for 2025

While the regulatory angle, the macroeconomic environment and decarbonisation targets may raise questions, the bank’s fundamentals are sound with historically high levels of profitability, improving solvency ratios, credit quality legacies well-controlled and strong liquidity. And banks are finally bringing more sustainable investments to the heart of their strategy. The recent earnings season has shown solid results, but the focus is shifting to growth, fee income and consolidation.

Under this scenario, what are the opportunities in the capital structure?

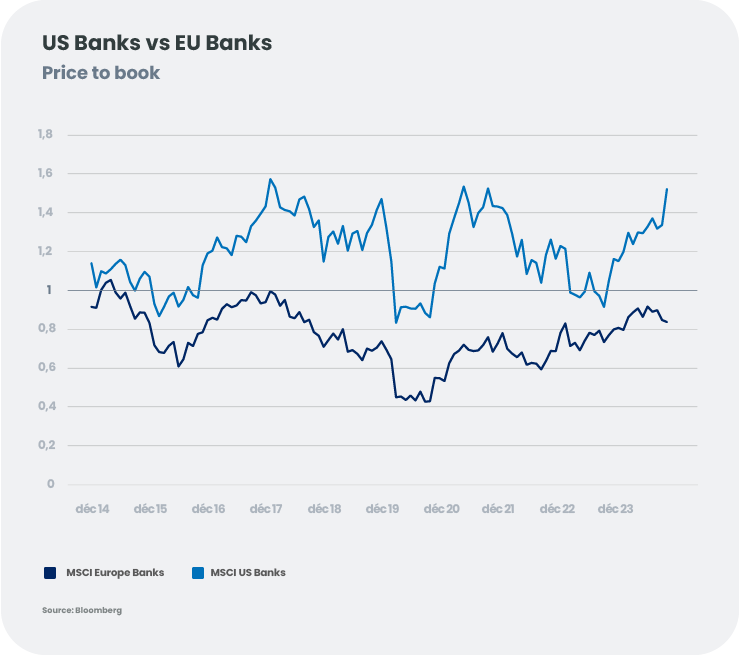

Equities: Are they already full?

Share prices have already risen sharply as European banks equities delivered another robust performance in 2024 (as implied by the price/book ratios in the figure). The rate cycle is likely to hamper earnings momentum, and while credit quality remains strong, it may deteriorate rapidly as the economy slows. Bear in mind the cyclicality and leverage of banking.

On a positive note, consolidation is rising. In recent months, BBVA launched a bid on Banco Sabadell in Spain, Unicredit acquired a 20% stake in Commerzbank, and BPM built a 9% stake in Banca dei Monte Paschi di Sienna. Unicredit (again) finally launched an offer on BPM, while Eurobank is buying the minorities in Hellenic Bank of Cyprus. This should benefit investors by forcing greater discipline on managements – in pricing, efficiency, and capital allocation. However, Europe remains a fragmented market and cross-border consolidation is restrained by the absence of a common banking market and by political resistance in domestic markets.

Also, the sector would not be fully immune during bouts of volatilities. Political and economic turmoil in some jurisdictions could spark the return of a bank-sovereign nexus, with peripheral countries such as Spain or Italy potentially better placed than historically core European countries (France or Germany).

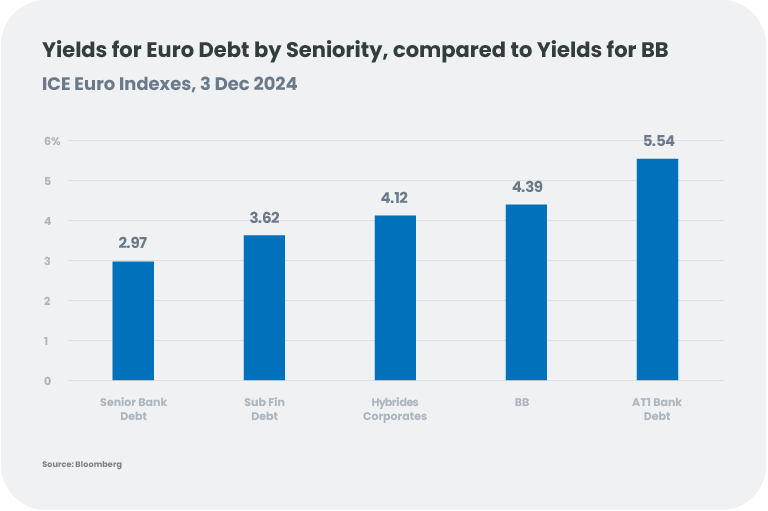

Bank Debt: Senior or Subordinated?

Compressed valuations of bank debt suggest that performance is more likely to come from carry than from spread tightening, all across the capital structure. But bank subordinated debt (Additional Tier 1 and, to a lower extent Tier 2) may selectively offer attractive yields, not only versus senior debt, but also in comparison with other riskier assets such as high-yield BB and hybrid corporates.

Pick the Right Issue

Supported by sound capital ratios and reasonably strong asset quality, we think a few selective opportunities may be found at the lower part of the debt capital structure. AT1 debt instrument and Tier 2 offer a yield close to High yield BB but are issued from banks with A rating in average. Taking into account current solvency ratios, banks are effectively far from the point of non viability which would trigger absorption risk and potential coupon switch. Sound track records on AT1 calls and liability management exercise comfort us that banks will continue to call but issuer selection remains critical. We retain our preference for national champions and, more broadly, higher-quality names.

[1] Comment made during the 25 November 2024 “BPM acquisition” conference call.

[2] These intermediate targets should cover all or a substantial majority of nine carbon-intensive sectors.

-

Outlook 2025, Nadège Dufossé

Outlook 2025, Nadège DufosséAsset Allocation in 2025: Between Optimism and Uncertainties

Global growth progresses in line with expectations, but the economic landscape remains fragmented. While activity is strong in the United States, the Eurozone is struggling to move forward, and China is penalised by weak consumption. Geopolitical tensions and the rise of political uncertainty in several countries risk exacerbating these divergences in 2025. -

Outlook 2025, Steeve Brument, Bertrand Dardenne

Outlook 2025, Steeve Brument, Bertrand DardenneM&A: Triple Trends for 2025?

As we head into 2025, the stars seem to be aligning for a revival of mergers and acquisitions, creating a fertile environment for investors seeking new opportunities. Merger arbitrage strategies attempt to capitalize on M&A activity by using a structured approach returns. -

Outlook 2025, Alix Chosson, Tanguy Cornet

Outlook 2025, Alix Chosson, Tanguy Cornet2025: the swan song for global climate action?

2024 concluded as another annus horribilis for climate action, with COP29 blowing “hot air”, reinforced geopolitical tensions overshadowing the climate crisis, and the re-election of Donald Trump in the U.S. We only have a couple of years left before spending the totality of the +1.5°C carbon budget. How will the recent political changes and global geopolitical tensions impact the transition? -

Outlook 2025, Christopher Mey, Paulo Salazar

Outlook 2025, Christopher Mey, Paulo SalazarIs China ready for another Trump fight?

With Donald Trump returning to the White House in 2025, his second term is likely to see a resurgence of tariffs and export restrictions among other things, raising concerns about China's ability to withstand a resurgence of 'America First' policies. -

Outlook 2025, Thibaut Dorlet, Nicolas Rutsaert, Nicolas Cleris

Outlook 2025, Thibaut Dorlet, Nicolas Rutsaert, Nicolas ClerisDiversify Your Portfolio Through the Commodity

As Donald Trump returns to White House, his policy agenda could send ripples through the global oil market. His trade wars and immigration stance are expected to fuel inflation, while his commitment to deregulation and to increasing US oil production pose new challenges for oil prices. -

Johan Van der Biest, Vincent Compiègne, Alfred Sandeman, Outlook 2025

Johan Van der Biest, Vincent Compiègne, Alfred Sandeman, Outlook 2025Hello ChatGPT: Will AI continue to surprise the world?

If investors are expected to be early in detecting future trends, then our community certainly thinks AI is the future. Will the surprises continue? To help train ChatGPT’s response, we analyse the tangible revenue that has emerged so far, and consider the ‘sweet spot’, the ‘runners-up’ and the ‘too early’. -

Christian Solé, Thomas Madesclaire, Lucia Meloni, Outlook 2025

The 2025 European Banking Puzzle: Risks, Rewards, and Regulation

Conflicting or competing regulatory regimes on both sides of the Atlantic, a changing rates environment with central banks in easing mode, and consolidation are the new trends to watch in the European banking sector as we head into 2025. Select carefully and keep an eye on the emissions. -

Lucie Hamadache, Christian Solé, Rémi Savage, Outlook 2025

Lucie Hamadache, Christian Solé, Rémi Savage, Outlook 2025A New Dawn for European Real Estate? Navigating a Path to Recovery

While easing interest rate pressure may bring some relief to the European property market, some challenges remain, making selectivity crucial in navigating today's uncertain environment.