How will the recent political developments in the U.S. and in Europe impact the transition? Is the energy transition still a relevant investment theme?

2024 concluded as another annus horribilis for climate action, with COP29 blowing “hot air”, reinforced geopolitical tensions overshadowing the climate crisis, and the re-election of Donald Trump in the U.S. We only have a couple of years left before spending the totality of the +1.5°C carbon budget. How will the recent political changes and global geopolitical tensions impact the transition?

The energy transition is not a question of ‘if’, but of ’when’ and ‘how’. Climate change is a physical reality, as seen in the recent deadly floods in Spain. Failing to act now means paying a higher price later, and forcing countries to adapt with far greater socioeconomic consequences.

While waning political ambition may slow the transition, we see it as an unstoppable trend that will continue to reshape our societies. The decisions guiding this energy transition will be increasingly driven by the pursuit of greater economic competitiveness and the imperative to secure maximum independence in energy supply chains

A delayed transition is now the most likely scenario

Global GHG emissions rose to 57.1Gt CO2e in 2023, up 1.3% over a year[1]. Unfortunately the peak of global emissions is now further away on the horizon. Current climate commitments are steering us toward a best-case global warming scenario of +2.6°C with severe environmental, social and economic consequences. The lack of ambition shown in Baku at COP29 and the election of Donald Trump in the U.S. are not signals of hope, at least on the medium term.

However, on the ground, many technologies key to the energy transition are showing very strong development, first and foremost renewables. Global renewable capacity is expected to grow by 2.7 times by 2030, surpassing countries’ ambitions by nearly 25%[2]. This represents an additional 5,500 GW of capacity, with about 60% of this growth occurring in China. While this falls short of the net zero trajectory objective of tripling renewable capacities, it underscores that renewable development is now less driven by environmental regulation and subsidies, and thus less subject to political volatility.

Politics and regulation are no longer the sole compass of this transition

The Inflation Reduction Act (IRA) in the U.S. showed how regulations can accelerate the transition. Although Trump announced he would aim for a repeal of this Act, a full repeal is unlikely given its economic benefits in many Republican-led states. Trump’s anti-environmental stance is likely to focus on symbolic decisions that shouldn’t jeopardise economic growth, such as reducing the power of federal agencies or repealing emissions and pollution controls.

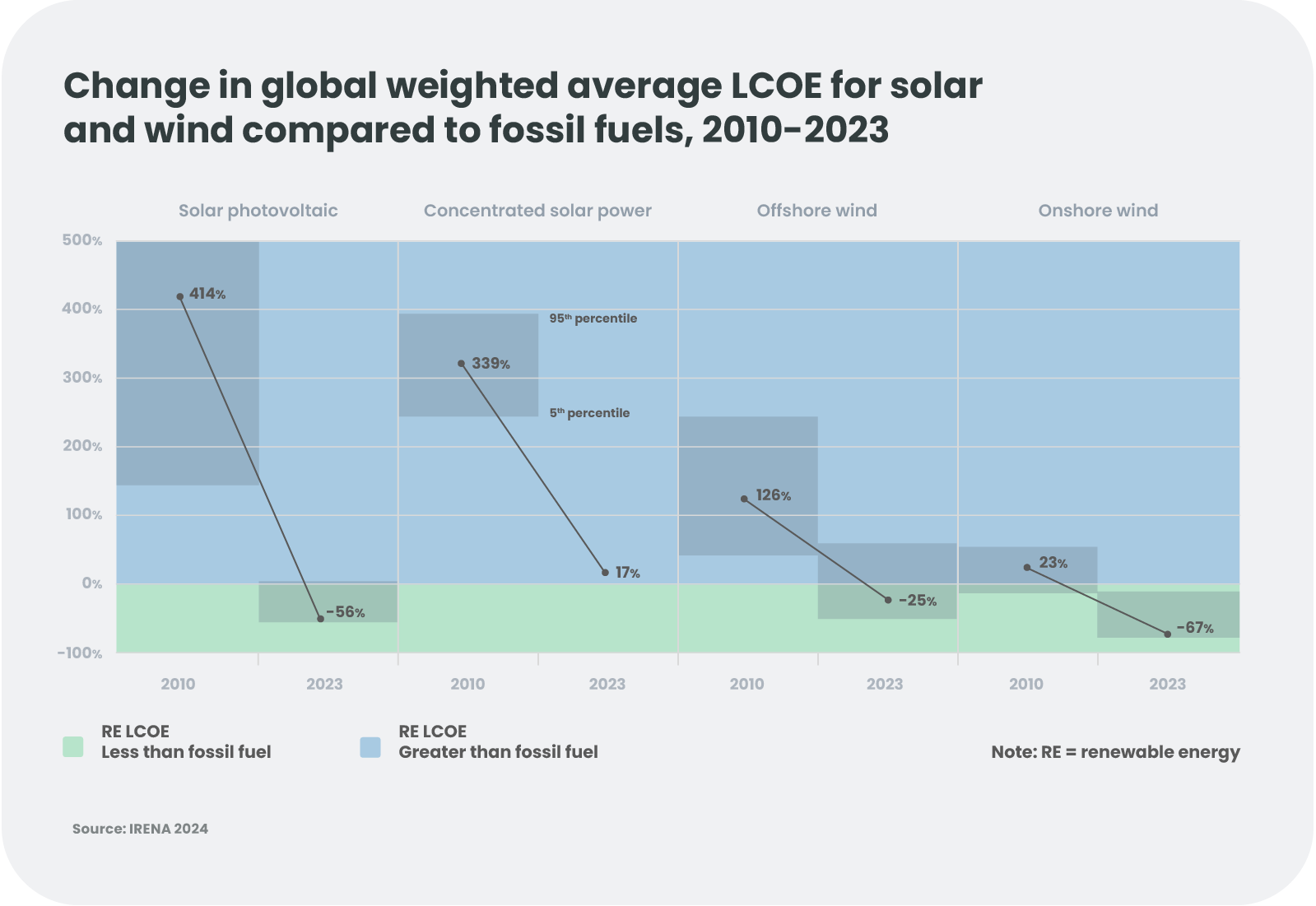

While regulations can accelerate the transition, the rapid deployment of renewables globally is now mostly driven by economic factors. in many regions thanks to a continuous improvement in their global weighted average Levelized Cost Of Energy (LCOE) - which technological advancements are expected to further reduce. Meanwhile, thermal power generation is challenged by rising carbon costs and volatile commodity markets.

Amid global trade tensions, the clean tech supply chain is becoming a key geopolitical battleground

A trade war is brewing between the U.S. and China, and to a lesser extent Europe, aiming to protect local clean tech industries. The clean tech sector has become a prime target for protectionism, as seen in May with tariff increases on Chinese products such as electric vehicles (EVs), solar cells, EV batteries and non-EV Lithium-ion batteries, or the Intergovernmental Critical Mineral Task Force Act enacted in September 2024 that aims to reduce US reliance on China for critical minerals used in clean tech.

This means that building regional clean tech supply chain and is now seen as a matter of competitiveness and sovereignty - one of the few topics that has bipartisan support in the U.S. This should serve as a guiding thread in decisions made beyond political divides.

The situation is similar in Europe. Despite the new Parliament and Commission’s softer stance on environmental matters, it is unlikely that the EU will dismantle flagship regulation such as the Net Zero Industry Act, which first and foremost aims at ensuring Europe’s competitiveness and independence on the long run.

Ultimately, while the regionalisation of clean tech supply chains is likely to increase the overall cost of the transition, it will require even more investments in clean technologies and their supply chains, creating larger investment opportunities.

How to seize investment opportunities in this new context?

Investments in the transition are on track to reach $2 trillion in 2024, a 60% increase since 2015[3]. According to the International Energy Agency’s (IEA) central “Announced Pledges” scenario, this number is expected to double in advanced economies and China, and quadruple in developing economies, reaching nearly $3.7 trillion. In the net zero scenario, investments are projected to increase to $4.8 trillion. Both scenarios create a wide range of opportunities for investors across a variety of technologies.

Electrification is key – with significant increase expected in power demand

Electrification is key to decarbonising the global economy. Global electricity demand is expected to rise faster over the next two years (+3.4% annually through 2026[4]), driven by demographics, new usages such as A.I. (data centers are expected to consume 1,000 TWh by 2026[5]) and the electrification of energy needs in buildings, industry and transport. In its base case “STEPS” scenario[6], the IEA sees electricity demand growing by 1000TWh per year throughout 2035 (45% coming from China), equivalent to adding another Japan to global electricity consumption every year.

The deployment of renewables is driven by increasing power demand and favourable economics

The global weighted average LCOE for utility-scale solar PV projects is now at $0.049/kWh[7], 29% lower than the cheapest fossil fuel-fired option[8]. The economic benefits of solar and wind technologies are compelling, even without subsidies. The Inflation Reduction Act and the Bipartisan Infrastructure Law have laid the groundwork for clean energy progress, and local, state and private sector leaders are expected to carry this momentum forward. Increasing power demand and further improvements in LCOE are the key drivers of the 2.7x increase in capacity by 2030 envisaged by the IEA in its base case scenario.

Massive grid investments are required to unlock the green potential

Upgrading and expanding transmission infrastructure is essential to decarbonise power systems. In the U.S., more than 70% of grid transmission lines and transformers are old and vulnerable to power outages, cyber-attacks, and susceptible of causing wildfires. According to the IEA, investments in grids must double to over $900 billion annually to meet climate goals, with every 1$ invested in renewables requiring another 1$ in grids. As of 2023, almost 1,500 GW of advanced wind and solar projects were in global connection queues, waiting to connect to the electricity grid due to a lack of grid availability. Governments have a crucial role to play in unlocking investments in larger, more resilient and more digitalised grids.

The (still) missing piece to net zero power systems: energy storage

The demand for storage solutions is rising rapidly. Battery storage capacity was projected to grow by 82% in 2024[9], with technological improvements allowing to reduce costs and improve efficiency up to 2030. In particular, sodium-ion battery technologies and on the longer term solid-state batteries are expected to help resolve the stationary storage technological conundrum, that has so far prevented energy storage system from playing the role they should in decarbonising power grids. We expect technological breakthrough in this space to happen before 2030.

Conclusion

The political developments of 2024 have challenged the transition to net zero. However, the physical reality of climate change remains the same, or worse. A senior US advisor said in Baku: “This is not the end of our fight for a cleaner, safer planet. Facts are still facts. Science is still science. The fight is bigger than one election, one political cycle in one country”.

The momentum around the transition is now supported by the drive for increased economic competitiveness and the need to ensure maximum energy supply chain independence, that should mitigate the influence of shorter-term political changes. Ultimately, in the context of deglobalisation, investments needed for the transition are likely to be higher than expected, creating a wide range of investment opportunities.

[1] United Nations Environment Program, 2024 Emissions Gap Report

[2] International Energy Agency (IEA), "Renewables 2024" report

[3] International Energy Agency (IEA), "World Energy Investment 2024" report

[4] International Energy Agency (IEA) , “Electricity 2024” report

[5] International Energy Agency (IEA), "World Energy Outlook 2024" report

[6] The Stated Policies Scenario (STEPS) is designed to provide a sense of the prevailing direction of energy system progression, based on a detailed review of the current policy landscape. It provides a granular, sector-by-sector evaluation of the policies that have been put in place to reach stated goals, taking account not only of existing policies and measures but also those that are under development (IEA)

[7] International Renewable Energy Agency (IRENA), "Renewable Power Generation Costs in 2022" report

[8] For power generation, the main fossil fuel-fired options are coal, conventional natural gas, and natural gas combined cycle – which is the cheapest

[9] Visual Capitalist, “2024 U.S. Clean Electricity Outlook “

-

Outlook 2025, Nadège Dufossé

Outlook 2025, Nadège DufosséAsset Allocation in 2025: Between Optimism and Uncertainties

Global growth progresses in line with expectations, but the economic landscape remains fragmented. While activity is strong in the United States, the Eurozone is struggling to move forward, and China is penalised by weak consumption. Geopolitical tensions and the rise of political uncertainty in several countries risk exacerbating these divergences in 2025. -

Outlook 2025, Steeve Brument, Bertrand Dardenne

Outlook 2025, Steeve Brument, Bertrand DardenneM&A: Triple Trends for 2025?

As we head into 2025, the stars seem to be aligning for a revival of mergers and acquisitions, creating a fertile environment for investors seeking new opportunities. Merger arbitrage strategies attempt to capitalize on M&A activity by using a structured approach returns. -

Outlook 2025, Alix Chosson, Tanguy Cornet

Outlook 2025, Alix Chosson, Tanguy Cornet2025: the swan song for global climate action?

2024 concluded as another annus horribilis for climate action, with COP29 blowing “hot air”, reinforced geopolitical tensions overshadowing the climate crisis, and the re-election of Donald Trump in the U.S. We only have a couple of years left before spending the totality of the +1.5°C carbon budget. How will the recent political changes and global geopolitical tensions impact the transition? -

Outlook 2025, Christopher Mey, Paulo Salazar

Outlook 2025, Christopher Mey, Paulo SalazarIs China ready for another Trump fight?

With Donald Trump returning to the White House in 2025, his second term is likely to see a resurgence of tariffs and export restrictions among other things, raising concerns about China's ability to withstand a resurgence of 'America First' policies. -

Outlook 2025, Thibaut Dorlet, Nicolas Rutsaert, Nicolas Cleris

Outlook 2025, Thibaut Dorlet, Nicolas Rutsaert, Nicolas ClerisDiversify Your Portfolio Through the Commodity

As Donald Trump returns to White House, his policy agenda could send ripples through the global oil market. His trade wars and immigration stance are expected to fuel inflation, while his commitment to deregulation and to increasing US oil production pose new challenges for oil prices. -

Johan Van der Biest, Vincent Compiègne, Alfred Sandeman, Outlook 2025

Johan Van der Biest, Vincent Compiègne, Alfred Sandeman, Outlook 2025Hello ChatGPT: Will AI continue to surprise the world?

If investors are expected to be early in detecting future trends, then our community certainly thinks AI is the future. Will the surprises continue? To help train ChatGPT’s response, we analyse the tangible revenue that has emerged so far, and consider the ‘sweet spot’, the ‘runners-up’ and the ‘too early’. -

Christian Solé, Thomas Madesclaire, Lucia Meloni, Outlook 2025

Christian Solé, Thomas Madesclaire, Lucia Meloni, Outlook 2025The 2025 European Banking Puzzle: Risks, Rewards, and Regulation

Conflicting or competing regulatory regimes on both sides of the Atlantic, a changing rates environment with central banks in easing mode, and consolidation are the new trends to watch in the European banking sector as we head into 2025. Select carefully and keep an eye on the emissions. -

Lucie Hamadache, Christian Solé, Rémi Savage, Outlook 2025

Lucie Hamadache, Christian Solé, Rémi Savage, Outlook 2025A New Dawn for European Real Estate? Navigating a Path to Recovery

While easing interest rate pressure may bring some relief to the European property market, some challenges remain, making selectivity crucial in navigating today's uncertain environment.