While easing interest rate pressure may bring some relief to the European property market, some challenges remain, making selectivity crucial in navigating today's uncertain environment.

The European real estate sector may be at a crossroads. In 2023, rising interest rates have weighed heavily on a sector that is highly leveraged. This has increased refinancing risks and weighed on valuations. However, recent developments such as monetary easing and structural developments driven by demographic shifts and the energy transition suggest the potential for a recovery. The key question is: where might the opportunities be?

Better financing conditions

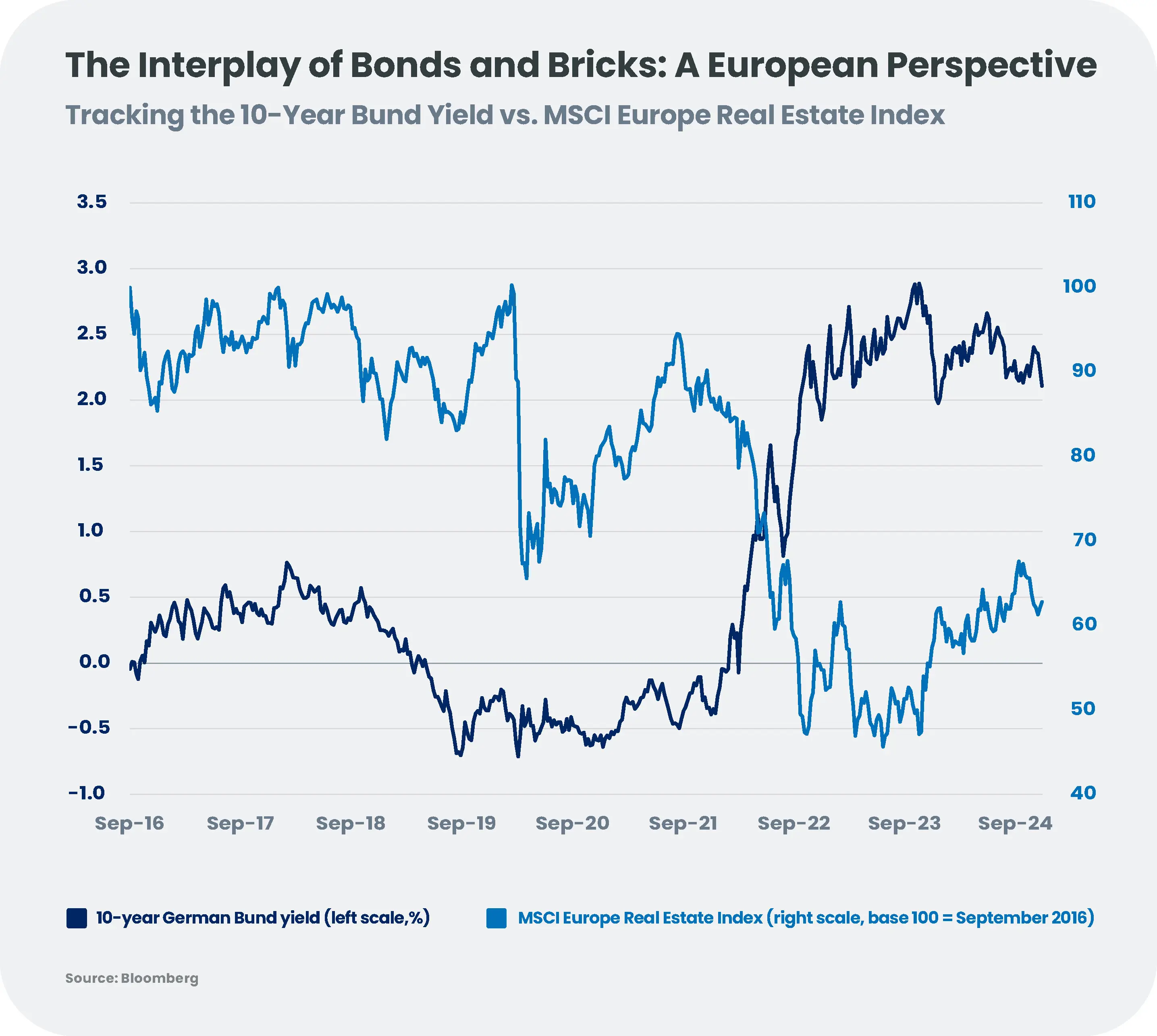

The property sector is highly dependent on leverage, with debt levels typically around 10 times EBITDA for European companies, compared with a maximum ratio of 2 to 3 for investment grade corporate issuers[1]. Historically, the sector has thrived in low interest rate environments, using cheap debt to finance acquisitions and development. However, aggressive interest rate hikes since mid-2022 have reshaped the landscape, with share prices dropping significantly - the MSCI Europe Real Estate Index fell 28% between 31 December 2021 and 28 November 2024[2].

The European Central Bank (ECB) has started to ease monetary policy in mid-2024, with further rate cuts expected to bring interest rates closer to 2% by the end of 2025, according to our own forecasts. This shift is already improving funding conditions, facilitating refinancing and narrowing credit spreads. Real estate bond spreads appear to have completed their normalisation in 2024, after peaking at about 420 basis points (bps) at the end of 2022, i.e. a spread of over 200 bps compared to the average corporate spread (historically around 20-30 bps)[3]. After a year of transition, many property companies are returning to the capital markets, signalling renewed confidence.

While the immediate impact of tighter monetary policy remains, the long-term outlook is brighter. Lower interest rates are expected to support property values, decrease loan-to-value ratios and revive investment activity. However, issuer selection remains critical as debt markets stabilise unevenly across sub-sectors.

Past performance of a given financial instrument or index or investment service, or simulations of past performance, or future performance forecasts are not reliable indicators of future performance.

Housing affordability and demographic pressures

Access to housing remains a pressing issue across the developed world. In the EU, average rents increased by almost 23% and house prices by 48% between 2010 and 2023[4]. Residential, student and retirement housing companies are poised to benefit from supply shortages and demographic trends, especially if policies favour increased supply over rent regulation.

Furthermore, urbanisation and an ageing population are reshaping demand. Major cities such as London, Paris and Berlin continue to attract young professionals and students, while senior housing is becoming a critical segment as Europe's population ages.

While President-elect Donald Trump has pledged to prioritise deregulation and support construction to increase housing supply in the US, Europe is taking a different path, focusing on energy efficiency and affordable housing solutions. For the first time, the EU Commission has appointed a housing commissioner to tackle issues ranging from energy efficiency to investment and construction.

In addition to regulatory measures, tax debates, such as the recent discussion around Spain's Real Estate Investment Trust (REIT) regime[5], highlight the challenges governments face in balancing affordable housing initiatives with fiscal pressures. These risks could re-emerge as countries seek to finance growing deficits. Among the most vulnerable sectors are property developers. For the time being, however, these remain speculative concerns, with no concrete measures on the table.

Energy efficiency and the sustainability imperative

Globally, buildings account for 30% of final energy consumption and 26% of energy-related CO2 emissions, while contributing significantly to resource depletion, water use, waste generation and loss of biodiversity[6].

In response, many governments and companies have adopted carbon neutrality targets to reduce the built environment's reliance on fossil fuels. For example, France will introduce new restrictions on building standards from January 2025[7], while national Energy Performance Certificate (EPC) ratings[8] are driving renovation projects for poorly performing assets. Gradual minimum energy criteria for new and rented buildings are becoming the norm across Europe.

In listed real estate, we are already seeing progress in reducing Scope 1 and 2 energy intensity[9], with companies recognising the benefits of sustainable buildings. For example, office tenants are increasingly demanding green-certified assets, while logistics companies are monetising roof space by leasing it to solar energy companies. Despite this progress, Scope 3 disclosure remains inconsistent and lacks the granularity needed to accurately assess the true energy intensity of portfolios.

As interest rates fall, we expect to see an increase in environmental retrofit projects, particularly in the residential sector, where the high interest rate environment had previously slowed capital expenditure (CAPEX).

Winners and losers

European real estate has faced limited investment in recent years, leading to a shortfall in supply relative to projected demand and strong rental growth. While most companies trade at a discount to net asset value, the caution of equity investors contrasts with the growing interest of private players. However, the picture varies by sub-sector.

- Residential and student housing: In major European cities such as London and in Germany, residential and student housing face a significant supply-demand imbalance, with vacancy rates at historic lows. For example, demand for rental housing in the UK is expected to increase by 20% by 2031, supporting rental growth above inflation[10].

- Elderly housing: In the aftermath of the Covid-19 crisis and the Orpea scandal in France, seniors housing faced rising vacancies and bankruptcies. However, as Europe's population ages and confidence returns, vacancies are falling, margins are recovering and rents are set to rise, allowing for renewed investment.

- Offices: While the full remote working threat is disappearing, prime office assets that meet high environmental standards remain in demand, with vacancy rates for prime City offices at a decade low of 3.9%[11]. However, older assets require significant investment, so caution is warranted in this sub-sector. New flexible working habits also increase the importance of a well-connected location.

- Shopping centres: Despite a post-Covid slowdown, online sales continue to put pressure on shopping centres. Owners are countering this trend by creating destination centres and attracting anchor tenants.

- Logistics: Logistics assets face short-term pressure from global trade tensions and the economic slowdown but remain resilient due to reshoring trends and the need for higher inventory levels. Vacancy is low and market rents are expected to rise in line with inflation, supported by robust transaction activity.

Balancing bonds and equities in a changing market

Overall, we maintain a positive outlook on the European real estate sector and see potential equity opportunities in supply-constrained niches such as residential, student accommodation, senior living and logistics. In the bond market, our stance remains neutral on European investment grade real estate bonds, which have recovered much of their 2024 underperformance, limiting further spread tightening. However, green bonds stand out as they address environmental challenges while underscoring the sector's commitment to sustainability, with top players fully transitioning to green financing. Political risks, including fiscal pressures in high deficit countries and the rise of populism that undermines investor confidence, add uncertainty to the outlook and hinder bold climate initiatives. In such an uncertain environment, selectivity should remain paramount.

Prices and calculations as of 28 November, 2024.

[1] Source: Candriam

[2] Source: Bloomberg

[3] Sources: Bloomberg, Candriam

[4] Source: Eurostat

[5] While the Spanish left-wing party Sumar proposed to abolish the tax advantages of the SOCIMI (Spanish REIT) regime, this proposal was rejected by the Parliament on 20 November 2024.

[6] Source: International Energy Agency: Buildings - Energy System - IEA

[7] In France, a new threshold of the RE2020 building code will apply from 1 January 2025, requiring new multi-family buildings to achieve a maximum energy consumption of 260 kgCO2eq/sqm/year. guide_re2020_version_janvier_2024.pdf

[8] Energy Performance Certificates are a rating system that summarises the energy efficiency of buildings. The building is given a rating between A (very efficient) and G (inefficient).

[9] Scope 1 includes direct greenhouse gas (GHG) emissions from facilities or vehicles directly controlled by the organisation. Scope 2 covers indirect emissions from the production of purchased electricity, heat or steam used by the organisation. Scope 3 encompasses other indirect emissions, such as those from procurement, which often account for more than 60% of a company's total GHG emissions. Scope 3 for the real estate sector includes embodied-emissions from construction materials as well as “in-use” emissions from heating, ventilation and air conditioning.

[10] Source: Grainger FY 24 conference call

[11] Sources: CoStar, JP Morgan as of 20/11/2024

-

Outlook 2025, Nadège Dufossé

Outlook 2025, Nadège DufosséAsset Allocation in 2025: Between Optimism and Uncertainties

Global growth progresses in line with expectations, but the economic landscape remains fragmented. While activity is strong in the United States, the Eurozone is struggling to move forward, and China is penalised by weak consumption. Geopolitical tensions and the rise of political uncertainty in several countries risk exacerbating these divergences in 2025. -

Outlook 2025, Steeve Brument, Bertrand Dardenne

Outlook 2025, Steeve Brument, Bertrand DardenneM&A: Triple Trends for 2025?

As we head into 2025, the stars seem to be aligning for a revival of mergers and acquisitions, creating a fertile environment for investors seeking new opportunities. Merger arbitrage strategies attempt to capitalize on M&A activity by using a structured approach returns. -

Outlook 2025, Alix Chosson, Tanguy Cornet

Outlook 2025, Alix Chosson, Tanguy Cornet2025: the swan song for global climate action?

2024 concluded as another annus horribilis for climate action, with COP29 blowing “hot air”, reinforced geopolitical tensions overshadowing the climate crisis, and the re-election of Donald Trump in the U.S. We only have a couple of years left before spending the totality of the +1.5°C carbon budget. How will the recent political changes and global geopolitical tensions impact the transition? -

Outlook 2025, Christopher Mey, Paulo Salazar

Outlook 2025, Christopher Mey, Paulo SalazarIs China ready for another Trump fight?

With Donald Trump returning to the White House in 2025, his second term is likely to see a resurgence of tariffs and export restrictions among other things, raising concerns about China's ability to withstand a resurgence of 'America First' policies. -

Outlook 2025, Thibaut Dorlet, Nicolas Rutsaert, Nicolas Cleris

Outlook 2025, Thibaut Dorlet, Nicolas Rutsaert, Nicolas ClerisDiversify Your Portfolio Through the Commodity

As Donald Trump returns to White House, his policy agenda could send ripples through the global oil market. His trade wars and immigration stance are expected to fuel inflation, while his commitment to deregulation and to increasing US oil production pose new challenges for oil prices. -

Johan Van der Biest, Vincent Compiègne, Alfred Sandeman, Outlook 2025

Johan Van der Biest, Vincent Compiègne, Alfred Sandeman, Outlook 2025Hello ChatGPT: Will AI continue to surprise the world?

If investors are expected to be early in detecting future trends, then our community certainly thinks AI is the future. Will the surprises continue? To help train ChatGPT’s response, we analyse the tangible revenue that has emerged so far, and consider the ‘sweet spot’, the ‘runners-up’ and the ‘too early’. -

Christian Solé, Thomas Madesclaire, Lucia Meloni, Outlook 2025

Christian Solé, Thomas Madesclaire, Lucia Meloni, Outlook 2025The 2025 European Banking Puzzle: Risks, Rewards, and Regulation

Conflicting or competing regulatory regimes on both sides of the Atlantic, a changing rates environment with central banks in easing mode, and consolidation are the new trends to watch in the European banking sector as we head into 2025. Select carefully and keep an eye on the emissions. -

Lucie Hamadache, Christian Solé, Rémi Savage, Outlook 2025

A New Dawn for European Real Estate? Navigating a Path to Recovery

While easing interest rate pressure may bring some relief to the European property market, some challenges remain, making selectivity crucial in navigating today's uncertain environment.