Central Bank Addicts

In its hit track 'Golden Brown', the British rock band 'The Stranglers' reminds us of the obvious: "No need to fight / Never a frown with golden brown." As the year draws to a close, it must be said that the financial markets were unable to withstand the 'golden brown' of central banks. On average, asset classes generated returns approaching 9%, one of the best years since 2012. And all this despite - excuse me for a moment - the economic slowdown, a near-recession in manufacturing, trade in the doldrums, and confused negotiations between Donald Trump and China. In short, such a synchronized performance of asset classes is inexplicable without reference to the massive intervention of central banks.

Never since the Great Financial Crisis have central banks lowered their key rates so quickly. After raising its benchmark rate four times in 2018, the US Federal Reserve made a complete about-face, with three decreases during 2019. The European Central Bank, which was expected to raise rates after the summer, lowered its deposit rate to a record low of -0.50%. The central banks of Australia, New Zealand, Switzerland, China, Mexico, Brazil, Indonesia, Turkey, Russia and even South Africa have all lowered their rates.

And as if this was the previous time, central banks injected massive amounts of liquidity. The Fed halted its balance sheet reduction, launching a monthly T-Bill purchase program of nearly $60 billion during the quarter. The ECB has also relaunched its €20 billion monthly bond purchase programme. After an attempt to overcome the dependency, the brown gold is flowing for the next few months. "Every time, just like the last / ... To distant lands / Takes both my hands / Never a frown with golden brown."

So much liquidity, but to what end? Since the 1970s, the principal mandate of central banks has been to control rising inflation. Since 2008, it has also been a question of controlling deflation. While financial markets have responded well to this monetary easing, inflation rates have remained oblivious. Since 2013, average inflation in the Euro zone has failed to reach 2%. In Japan, inflation rate is near zero. As to inflation expectations, the picture is not much more flattering: 5-year inflation expectations have reached their lowest point in the Euro zone at 1.10%, and 1.80% in the United States.

Should one conclude that central banks are inefficient?

Criticism and reduced independence

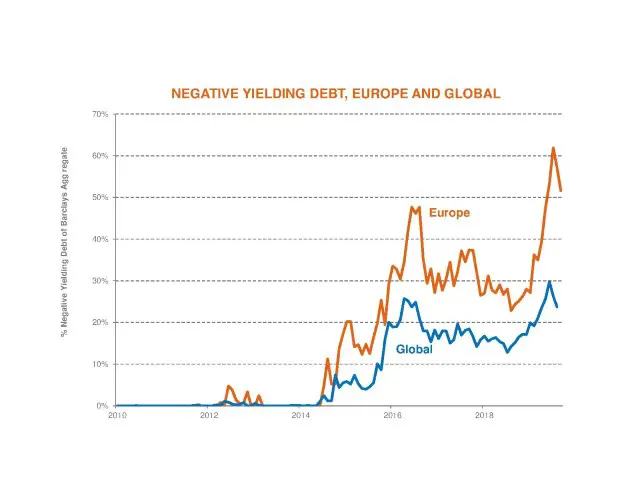

These mixed results have subjected central banks to strong criticism. Low rates are already a topic of debate, with the ECB subjected to the strongest criticism. By lowering its deposit rate, the ECB has caused a general decline in interest rates across Europe. Fifty percent of the Euro Aggregate bond index is in negative territory. This is a problematic situation for investors who - like French insurers or Dutch pension funds - have been very critical. This situation could jeopardise the ability of the European financial system to maintain pension levels. Commercial banks are also raising their voices. Caught between increasingly elaborate regulation and negative rates, their profitability is under strain. These effects are all the more worrying because by lowering rates below the psychological threshold of 0%, markets have begun to wonder whether the ECB can ever return to positive territory.

Additional criticism comes from the United States concerns the lack of central bank coordination. In 2018, the Fed was the only one to embark on a tightening cycle. Traditionally, the Fed has been followed by other developed central banks. But the causality has changed. Because the ECB and the BOJ, among others, are extremely accommodative, the Fed's room for manoeuvre has shrunk. The Fed is no longer independent from the rest of the world. All this has led world leaders to voice strong criticism of monetary policy - something not seen in 20 years.

Never give up!

Faced with low inflation, policy criticism, and policy limitations, central banks must reinvent themselves. Some options remain open to them.

First, they could adjust their mandates by making the inflation target either symmetric, or long-term. They could also integrate the management of financial conditions as an objective, which would provide a legal framework for the various quantitative easing programmes and offer more flexibility for their actions.

Another option would be to support governments by using negative rates for budgetary purposes. If France continued to borrow at negative rates (-0.50%) it could reduce its debt ratio by -40% in 30 years. A Maastricht counter-revolution to reach 60% without reducing its deficit!

Finally, the integration of climate risk could alter the situation. By facilitating the financing of virtuous activities, central banks would change their paradigm. The ECB could thus define common criteria for integrating climate risk management in the financial sector. It could also adapt its programme for purchasing financial assets dedicated to green investments, providing substance to the new Commission's stated plan.

"Never give up" was Mario Draghi's last message before leaving the ECB. While central banks seem to have reached their limits, thebig question of 2020 is whether they will successfully reinvent themselves and make a comeback in the face of widespread criticism. The question in the coming years is therefore less to predict the general level of rates than to anticipate the evolution of their political mandate. Their future is also our future.

The central banks are dead. Long live the central banks!

Source: Bloomberg, Candriam