The election of Donald Trump, coupled with the Republican Party's control of both houses of Congress, has resulted in a new political landscape in the United States. What key decisions must the new administration make? What impact will these decisions have on the macroeconomic environment, financial markets and investors?

To explore these questions, we are pleased to present the insights of Florence Pisani, Chief Economist, and Emile Gagna, Economist. We also invite you to hear the perspective of Lauren Goodwin, Chief Market Strategist at our parent company New York Life Investments, who offers her professional insights as an investor based in the United States.

Episode 5

17/04/2025

Only available in English

In these weeks of rapid change, events continue to push the US Federal Reserve’s two mandates, growth and inflation, in opposite directions. Tariffs have just increased the diverging pressures, and on 16 April, Fed Chairman Jay Powell admitted this publicly. The US view consensus seems to be that the Fed will cut rates to protect growth. But will Powell find it difficult for the Fed to cut rates with inflation this high, barring a dire recession? Meanwhile, the ECB is likely to find it easier to implement cuts.

Adding to the uncertainty in the US, as we enter the first quarter earnings reporting season, companies are providing either conditional earnings guidance or none at all. With US investors overweight their domestic holdings, we encourage them to increase European holdings.

17/04/2025 - US Chronicles: Up With Events

Episode 4

24/03/2025

Only available in English

The outlook may be shrouded in fog, but some large shapes are visible in the fog. Investors can use these longer-term shapes to make their way through the markets today. The US Fed is plagued by reconciling higher inflation and lower growth? Build resiliency into your portfolio, consider inflation-aware assets, and incorporate the crowing capital-intensity of digital and energy infrastructure into your investment allocations.

20/03/2025 - Clarifying the Known Unknowns

Episode 3

13/03/2025

Only available in English

Over the past few weeks, Europe took some big steps forward, with positive talks between Ukraine and Russia and Germany's plans for increased spending. In the last three months, the MSCI Europe index largely outperforms S&P 500. But there are still some major hurdles, like high energy prices and trade tensions. That said, the ECB’s accommodative policies and Germany’s potential fiscal stimulus could provide a tailwind. While it’s not a game-changer, it could act as an insurance policy against further economic damage. US investors, who are often underweight international stocks, may want to consider rebalancing their portfolios to include more European equities.

Host Lauren Goodwin, Chief Market Strategist at our parent company New York Life Investments, is joined by Emile Gagna, Deputy Head of Economic Research, to discuss the latest policy announcements in Europe and the economic outlook.

Episode 2 - “One Big, Beautiful Bill” [1]

06/03/2025

This second article in our series “Trump’s Economic Policy” is dedicated to the President’s budget agenda. Donald Trump has promised to reform “the deep state” and cut taxes. What are the stakes of the budget discussions that have just begun? How does the government intend to fund its costly tax cut programme?

The American budgetary process is complex, and several issues will take centre stage in the coming weeks. To avoid a government shutdown, Congress must pass a budget for fiscal year 2025 (which began in October 2024), or at least agree to vote for a new “continuing resolution” (the one adopted in December last year expires on 14 March, 2025). To avoid a technical default by the US government, the debt ceiling will also need to be raised.

The “Budget Reconciliation” Process

Given the marked political divide, the “reconciliation” procedure is the only way for Republicans to advance the President’s agenda without Democratic support. It avoids the risk of obstruction (filibuster) by Democratic senators who might be tempted to block the bill. Ending an obstruction requires a supermajority of three-fifths in the Senate (60 out of 100 votes) - a majority the Republicans do not have today.

The “Reconciliation” process allows bypassing the filibuster and passing laws with a simple majority. However, it is complex. The Senate or House Budget Committee gives instructions to its parliamentary committees to draft specific bills (such as funding to strengthen border security, reduce taxes, etc). It then combines these projects into one or more texts -- hence the name “Reconciliation” -- that must ultimately be adopted in the same terms by both chambers. However, Congress can only use “Reconciliation” once per “major issue” (spending, taxes, or debt ceiling) and per fiscal year. Importantly, the measures proposed in these texts must have a budgetary impact but must not worsen the budget balance beyond the reconciliation period (generally five to nine years), nor affect the Social Security system (ie, the first pillar of retirement in the United States).

One or Two Budget Bills?

Republican senators favour a two-step approach: voting a first bill that would include $340 billion in additional spending over four years (including $150 billion in increased military spending and $175 billion for border security), entirely financed by cuts in other spending, before a second bill that would make the tax cuts from the TCJA[2] permanent.

The House of Representatives, and Donald Trump, advocate a different strategy and want to vote on a single major budget bill. The resolution proposed by the House covers a nine-year period and includes $4.5 trillion in tax cuts, $300 billion in additional spending for border security, defence, and justice, and $2 trillion in spending cuts, largely focused on programmes for the most disadvantaged: Over the 2025-2034 period, the deficit would increase by $3.4 trillion. It also includes a $4 trillion increase in the debt ceiling.

This project has passed a first stage since it was narrowly voted (217 votes in favour and 215 against) on 25 February in the House of Representatives. The “Reconciliation” process will now begin in the House: Representatives will have to agree on the exact nature of the spending cuts and tax cuts. For the project to reach the Oval Office and be signed by the President, the Senate will also have to vote on the same text. Otherwise, a compromise will have to be reached between the two chambers. The “big and beautiful bill” desired by the President is therefore still far from being adopted.

A Budget Which Restricts Growth?

The House of Representatives’ budget proposal, which seems to be gaining traction today, is currently rather restrictive for growth. The envisaged tax cuts will not support activity as they mainly extend those implemented during Donald Trump’s first term (TCJA); the reduction in spending is, on the other hand, a factor which may drag on economic growth. Over the first year, we estimate that this budget would reduce GDP growth by 0.4 percentage points. Of course, Republicans can “play” with budgetary rules, for example, by extending tax cuts for only eight years and using the thus “saved” money at the end of the period to allow Donald Trump to keep some of his campaign promises in favour of the middle class (no tax on tips and overtime…).

However this is not the only effect of the Budget on growth. Despite lacking formal authority, the DOGE (Department Of Government Efficiency) promises even greater savings: $2 trillion… in just 18 months ! Its website already claims more than $65 billion in savings, though their origin is difficult to trace (adding up the value of the 2,000+ contracts the entity proposes to terminate only results in about ten billion dollars in savings).

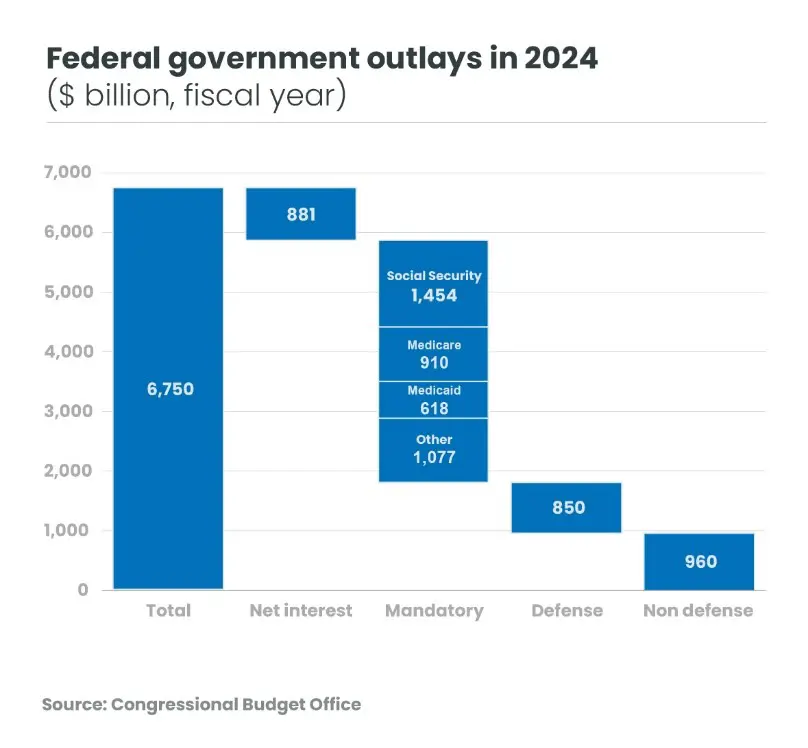

Given the structure of federal spending, Elon Musk’s promise seems unrealistic: The government must pay interest on its debt (nearly $900 billion) and the President has announced that he will not touch Social Security ($1.5 trillion) or Medicare ($910 billion). Cutting defence spending ($850 billion) would also be unpopular with the Republican electorate. This leaves $960 billion in discretionary spending and $1.6 trillion in various social programmes (eg, Medicaid, food stamps, and child nutrition programmes). Reducing these expenses by more than half in one year is a tall order!

The difficulty that House representatives are having in agreeing on the nature of the $2 trillion in budget cuts over ten years speaks volumes about the whimsical nature of the goal of the DOGE: In the House budget proposal, $500 billion in budget cuts have not been assigned to any parliamentary committee, and the remaining $1.5 trillion is already the subject of lively debate among Republicans. For example, some propose that the Energy and Commerce Committee -- expected to save $880 billion over ten years -- make deep cuts to the Medicaid programme. Others, including Donald Trump, want to spare this programme, which benefits 72 million Americans.

Whatever the evolution of budget discussions in Congress, the administration dismantling operation, threats of layoffs of civil servants, etc could weigh on household confidence, which has already been eroded by the prospect of higher tariffs. In addition to the budget debates, markets will also be closely watching confidence indicators in the coming weeks!

Episode 1 - Tariffs

14/02/2025

Following US President Donald Trump’s economic policy can seem difficult. America First Trade Policy, Securing Our Borders, Unleashing American Energy, Regulatory Freeze Pending Review, etc. In just ten days, Trump signed more executive orders than his predecessors during their first hundred days! Behind this avalanche of orders, the orientation of the President’s economic policy remains clear. Trump is following the broad outlines of the program he sketched out during his election campaign: Increasing tariffs, halting illegal immigration, reforming the ‘Deep State’,” tax cuts, support for fossil fuels, and deregulation more broadly. Today we begin a series of ‘posts’ that aim to put into perspective the economic consequences of the decisions made by the new Administration. This first post is dedicated to tariff policy.

Tariffs appear to be Donald Trump’s favourite instrument, notably because he can use them most freely. It is also, at least from the President’s point of view, an instrument that allows him to achieve several objectives at once: Rebalancing the United States’ foreign trade, finding new revenue to finance the costly tax cut programme due to expire at the end of the year, or even fighting drug trafficking and illegal immigration.

Initial Announcements

Invoking the International Emergency Economic Powers Act (IEEPA) of 1977, a federal law that grants him broad powers in the event of a ‘national emergency’, Trump announced as early as February 2nd that he would impose tariffs of 25% on Mexico and Canada and 10% on China. Until now, the IEEPA had never been used by a President to impose tariffs. In May 2019, Trump had indeed already brandished this threat at Mexico. He backpedalled a few months later, as an agreement had eventually been reached to curb the entry of migrants at the US Southwest/Mexico border.

A few days after threatening Mexico and Canada in 2025, the President granted a one-month suspension of the implementation of tariffs on these two countries, in exchange for concessions aimed at strengthening border security. However, Trump decided to increase tariffs on China by 10%, a much more modest increase, it should be noted, than the 60% mentioned during the election campaign. In perspective, this increase remains for now relatively contained (the average tariff rate on products imported by the United States will rise from 2.5% to 4%) and its effects on inflation and US growth should be low.

What are the Impacts on Growth?

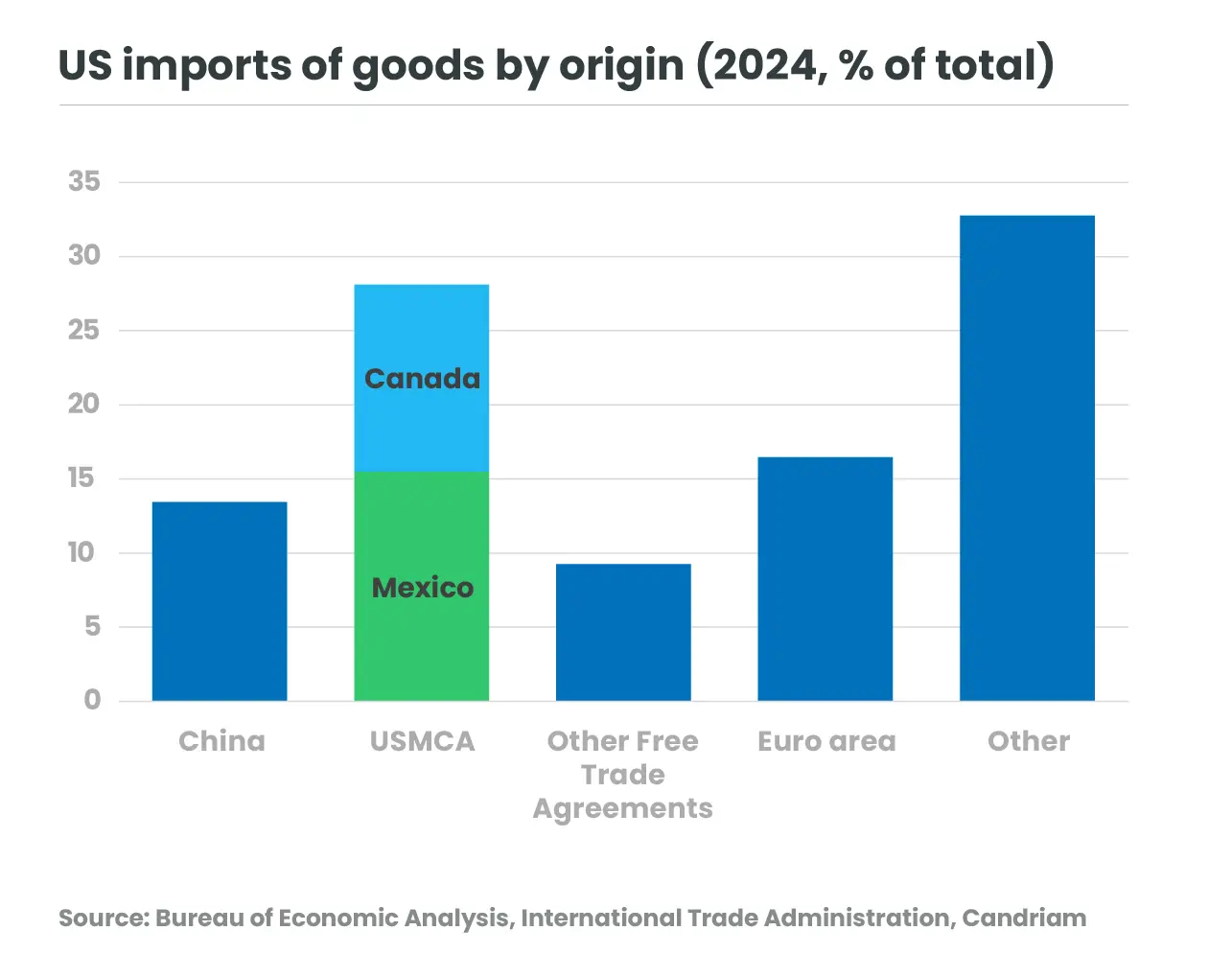

If Trump were to implement his threat against Mexico and Canada, things would change, however. Given the weight of these countries in US trade, the average tariff rate would exceed 10%, a level not seen since the end of the 1930s! Activity in Mexico and Canada would be seriously slowed (an estimated loss, according to Brookings[3], or one point of GDP if the countries do not retaliate and three points of GDP with a retaliatory response of the same magnitude), particular because of to the magnitude of their trade with the United States.

Given the size of the US economy, the effect on domestic growth would be more moderate (a loss of 0.2 to 0.3 points of GDP). However, it can be argued that this effect is underestimated because trade models do not fully account for the complexity of the deep economic integration of the three economies. In the automotive sector, for example, it is not uncommon for products to cross borders multiple times: If US manufacturers had to pay 25% tariffs each time they source from Mexico or Canada, this would increase the price of cars by an average of $3,000[4].

Imposing tariffs on Mexico and Canada would also run counter to the Trump administration’s goal of developing more secure supply chains. It could also push these countries to forge other economic partnerships with countries now seen as more reliable than the United States. Paradoxically, by undermining recent efforts to relocate supply chains to the American region (nearshoring), an increase in tariffs on Mexico or Canada could even, in the medium term, end up benefiting… China!

And What Next?

For now, of course, the President’s goal seems to be to obtain concessions in the fight against drug trafficking or illegal immigration. Perhaps it is also a matter of preparing for a renegotiation of the terms of the USMCA[5] free trade agreement more favourable to the United States. It is therefore far from certain that Trump will impose tariffs on all imports from historical US partners. In the meantime, however, on February 10th Trump just announced tariffs of 25% on steel and aluminum[6] (about 2. 5% of total US imports in 2024), an increase that will first affect Canada and Mexico!

Campaign statements and the America First Trade Policy executive order signed on January 20th -- the day of his inauguration -- suggest, however, that Donald Trump will not stop there in terms of tariff policy. On April 1st, he will receive reports allowing him to act using Section 232 of the Trade Expansion Act of 1962 or Section 301 of the Trade Act of 1974 to extend his threats to other countries… The EU, for instance, which Donald Trump has already called an ‘atrocity’ on trade!

… to be continued!

Update on US Liberation Day

As expected, ’Liberation Day‘ has brought a raft of new tariffs.

[1] D. Trump: « One, Big Beautiful Bill »

[2] Tax Cuts and Job Act, 2018, also called the ‘Trump tax cuts’.

[3] Trump’s 25% tariffs on Canada and Mexico will be a blow to all 3 economies

[4] Eric Levitz (2025), “Is Trump’s trade war with Mexico and Canada over? Why the tariffs might — and might not — still happen”, Vox

[5] US-Mexico-Canada.

[6] In Mars 2018, citing national security concerns, the President had already imposed tariffs of 25% on steel and 10% on aluminum under section 232 of the 1962 Trade Expansion Act.

-

US elections, Asset Allocation, Macro, Florence Pisani, Emile Gagna

US elections, Asset Allocation, Macro, Florence Pisani, Emile GagnaTrump’s Economic Policy

The election of Donald Trump, coupled with the Republican Party's control of both houses of Congress, has resulted in a new political landscape in the United States. What key decisions must the new administration make? What impact will these decisions have on the macroeconomic environment, financial markets and investors? -

ESG, SRI, US elections, Climate Action, Alix Chosson, Lucia Meloni, Rémi Savage

ESG, SRI, US elections, Climate Action, Alix Chosson, Lucia Meloni, Rémi SavageShould the sustainable community be concerned about a Trump 2.0 Presidency?

Donald Trump’s re-election as president of the United States has sparked concerns about his potential impact on key sustainability topics, notably climate action. -

Charudatta Shende, Nicolas Jullien, Fixed Income, US elections

Charudatta Shende, Nicolas Jullien, Fixed Income, US electionsBallots to Bonds

Following the US election, what will the bond landscape look like around the world in the near term and the medium term? President-elect Trump should be able to implement much of his political agenda over the next few years. We think four themes stand out: Tariffs, Regulations, Tax Cuts, and Immigration. What we don’t yet know is the timing and the magnitude of these elements. -

US elections

US elections : Hear it directly from the US

In the run up to the November 2024 US elections, our special correspondent in the US, Lauren Goodwin, Chief Market Strategist at our parent company New York Life Investments, shares her analysis on the campaigns and how US investors are navigating the environment. Every two weeks. Make sure to visit our US Chronicles ! -

Nadège Dufossé, Florence Pisani, Asset Allocation, US elections

Nadège Dufossé, Florence Pisani, Asset Allocation, US electionsUpdate on US elections

Donald Trump heads back to the White House as the 47th President, with an increased likelihood of a Republican sweep. Yesterday (6 November), market reactions were strong, with US stocks hitting all-time highs, 10Y bond yields jumping to 4.5%, and the dollar surging against most currencies. -

US elections, Christopher Mey, Paulo Salazar, Emerging Markets, Equities, Credit

US elections, Christopher Mey, Paulo Salazar, Emerging Markets, Equities, CreditChina’s economic outlook: Opportunities and threats as US elections loom

Chinese authorities have begun addressing deflationary pressures through a series of monetary and fiscal measures, signaling their growing urgency to stabilise the economy. -

US elections, Nadège Dufossé

US elections, Nadège DufosséHow should we position portfolios ahead of the US elections ?

Numerous statistics are being published on the performance of financial markets in the run-up to the US elections. US presidential elections do not occur often enough to generate statistically significant data, but we generally observe an increase in volatility from the summer preceding the election date, with range-bound markets. After the election, the uncertainty usually subsides, and the promises of the future new president may generate an end-of-year rally. -

Nicolas Forest, Florence Pisani, US elections

Nicolas Forest, Florence Pisani, US electionsShould we be afraid of the US elections ?

With the partisan divide hardening in the run-up to November 5, the presidential race was revived with the withdrawal of Joe Biden at the end of July. In just a few weeks, Kamala Harris has breathed new energy into the Democratic campaign.