The year 2024 ends with significant economic disparities between regions. Which asset classes should be prioritised for approaching 2025?

Global growth progresses in line with expectations, but the economic landscape remains fragmented. While activity is strong in the United States, the Eurozone is struggling to move forward, and China is penalised by weak consumption. Geopolitical tensions and the rise of political uncertainty in several countries risk exacerbating these divergences in 2025. These growth disparities between regions have already been largely reflected in equity performance in 2024, and investors have had time to position themselves accordingly. The year 2024 ends with a near-euphoric sentiment on the US market, while investors remain strongly underweight on European or emerging market equities. Here is the challenge for 2025: It seems difficult to go against these trends before knowing more about Donald Trump's policies; yet we believe opportunities could be found next year in assets that currently appear too weak or risky.

Our Asset Allocation at the Start of 2025

As we enter 2025, our asset allocation is based on a soft-landing scenario for global growth. The main central banks have entered a new cycle of monetary easing and will do what is necessary to support economic activity. China, for its part, is piling on measures and has sent a strong signal: The authorities want to get closer to their 5% growth target. The main risk to this scenario is Donald Trump's arrival at the White House in January, as it is still unclear which of his numerous campaign promises — tariffs, immigration, tax cuts, and deregulation — will actually be implemented. A hard stance on immigration and tariffs (the ‘hard Trump’ scenario) could derail these favourable prospects and would imply weaker global growth and higher inflation. Conversely, a softer version of his policies would not significantly undermine our overall growth and inflation forecasts.

Positive on Equities

In this context, our allocation remains positive on equities relative to bonds. We remain overweight on US equities. Although the US market's performance and valuation already incorporate a certain level of optimism following Donald Trump's victory, the growth trajectory of the US economy and corporate profits is much stronger and more resilient than that of other developed countries. We are, however, more favourable toward small- and medium-sized companies, cyclical sectors such as industrials, and financials, which should benefit most from Donald Trump's ‘reflationary’ and domestically favourable policies. We remain neutral on tech stocks, where valuations leave little room for new positive surprises despite a strong earnings momentum. In this sector, we prefer software and services over semiconductors.

We are underweight on European equities, which offer limited earnings growth prospects. Investor scepticism is very strong towards the region. The gap in investment and productivity gains relative to the United States continues to widen, and the political situation in France and Germany is mired in partisan divisions. Attractive valuation levels alone will not suffice to bring investors back. Europe will need to demonstrate better growth prospects, Germany will need to relax its ‘debt brake’, and trade tensions with the US will need to be successfully managed... which is possible, but far from certain. Outside the US, our preference leans toward emerging markets, which offer very attractive valuations and which are penalised by US interest rates and a strong dollar. The imposition of US tariffs represents the main risk for the region. However, Trump's first nominations and announcements seem to indicate a willingness to negotiate rather than engage in a full-scale trade war, which could weigh on US growth and inflation. The Chinese government’s successive announcements should help stabilise the country's economic situation and benefit the region as a whole. We are also neutral on Japan.

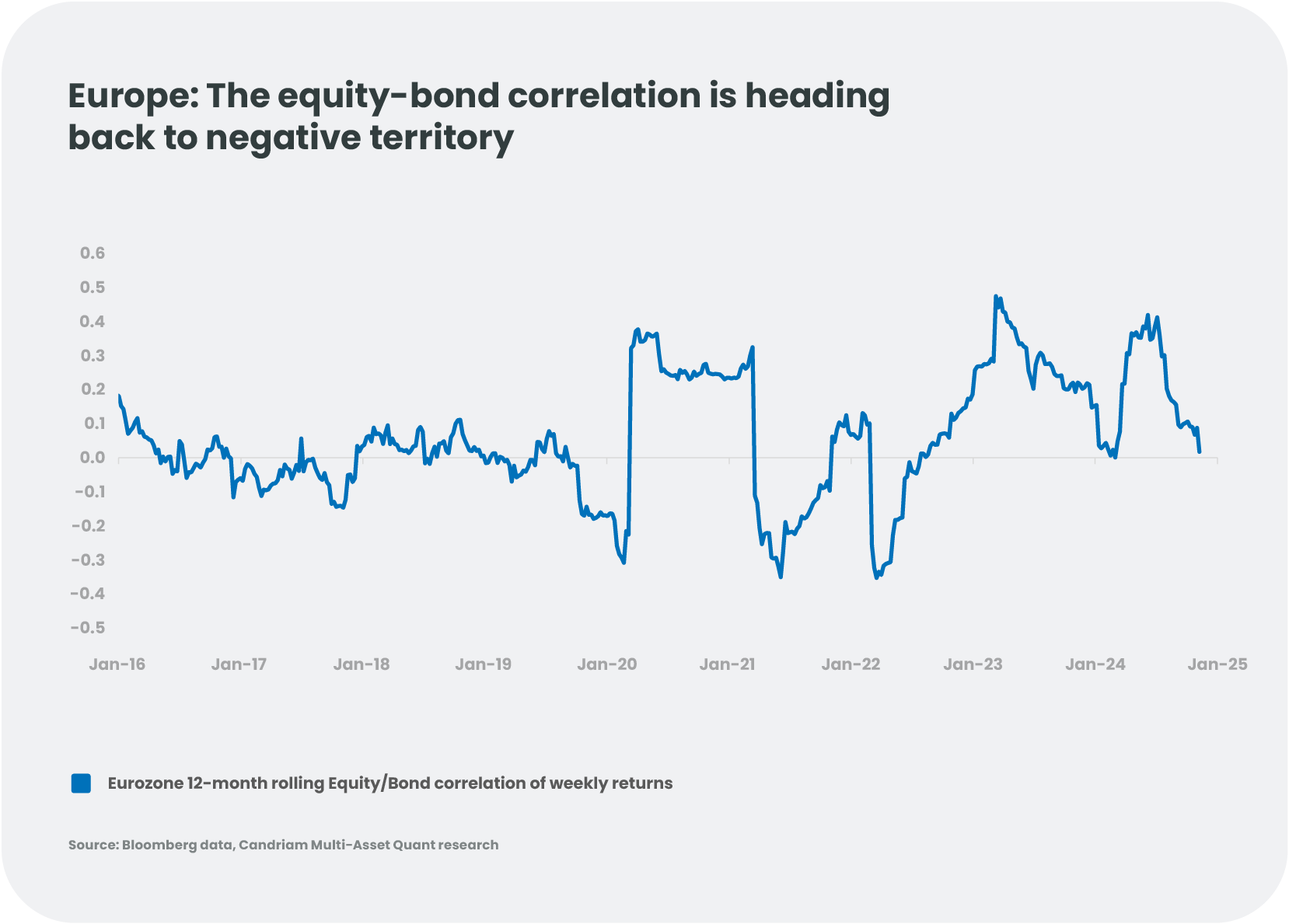

Government Bonds: Positive on Europe, but Negative on the US

We are long German duration in Europe. Growth expectations for 2025 are low, and we expect the ECB to cut rates further if necessary. Holding non-risky government bonds can also protect a diversified portfolio against any disappointment in growth levels, given that equities and bonds are once again negatively correlated in Europe in a context of disinflation. We remain cautious on French debt, awaiting an agreement on the 2025 budget, and prefer countries like Spain, where growth remains robust. Conversely, we are negative on US duration. While US rates have stabilised since Trump's election, the risk remains on the upside, depending on the measures actually implemented by the new president. The gap between US and European monetary policies is expected to persist. A negative position on US duration can also protect a diversified portfolio against a ‘hard Trump’ scenario and a significant rise in inflation expectations.

On Credit, We Prefer Europe

Credit spreads have significantly narrowed in 2024 and are now at historical lows for investment grade credit and high yield. In the US particularly, these levels make the risk asymmetrical, notably in high yield. The current spreads imply a default rate of 2%,[1] well below the current actual default rates of 4-5%.[2] Absent a recession, the risk of a significant spread widening is limited, but so is the potential for further narrowing. We therefore favour European credit, which benefits from a more favourable interest rate environment and higher spread levels overall than in the US. Regarding emerging market debt, spread levels appear more attractive, but we expect performance, particularly in local currencies, to remain highly dependent on US policy choices (evolution of US rates, the dollar, and the impact of potential tariffs on growth).

Currencies at the Heart of Trade Negotiations

The US dollar has appreciated by 5% this year against the euro but has remained within a 1.05-1.12 range since the beginning of 2023.[3] While Donald Trump calls for a weaker dollar to boost the competitiveness of US companies, the policy axes he defended during his campaign are bullish for the greenback! This paradox could limit the dollar's appreciation potential. Exchange rates will be at the heart of trade negotiations with the United States' main partners. This is particularly the case for the Yuan, which is currently close to its low points but could appreciate if the Chinese economy picks up and if compromises with the United States emerge on trade. The Yen could also appreciate with the stabilisation of the dollar.

Which Diversifying Assets do we Favour?

We remain positive on gold, which has suffered somewhat from a shift towards cryptocurrencies since Trump's election and has been penalised by a strong dollar and rising US real interest rates. In the longer term, however, gold retains its role as a diversifier and a protective tool in asset allocation. The underlying demand from many central banks remains strong relative to annual production and limited gold reserves. Any weakness in the price is an opportunity for us to increase our exposure to precious metals.

Some alternative strategies can also be included in an asset allocation in 2025: Market-neutral strategies may be used with the aim of benefitting from increased market volatility and dispersion while limiting direct market exposure risk, or risk arbitrage strategies with a view to take advantage of a potential resurgence in M&A activity in the US.

Conclusion

Each year, one uncertainty replaces another. The economic context has finally normalised with a soft landing for global economic growth and inflation moving out of a dangerous zone for economic stability. The election of Donald Trump introduces new uncertainties and risks, both economic and political. However, financial markets, to which Trump seems particularly sensitive, could play a safeguard role against overly extreme choices... which could reassure investors about the direction markets will take in 2025!

-

Asset Allocation in 2025: Between Optimism and Uncertainties

Global growth progresses in line with expectations, but the economic landscape remains fragmented. While activity is strong in the United States, the Eurozone is struggling to move forward, and China is penalised by weak consumption. Geopolitical tensions and the rise of political uncertainty in several countries risk exacerbating these divergences in 2025. -

M&A: Triple Trends for 2025?

As we head into 2025, the stars seem to be aligning for a revival of mergers and acquisitions, creating a fertile environment for investors seeking new opportunities. Merger arbitrage strategies attempt to capitalize on M&A activity by using a structured approach returns. -

2025: the swan song for global climate action?

2024 concluded as another annus horribilis for climate action, with COP29 blowing “hot air”, reinforced geopolitical tensions overshadowing the climate crisis, and the re-election of Donald Trump in the U.S. We only have a couple of years left before spending the totality of the +1.5°C carbon budget. How will the recent political changes and global geopolitical tensions impact the transition? -

Is China ready for another Trump fight?

With Donald Trump returning to the White House in 2025, his second term is likely to see a resurgence of tariffs and export restrictions among other things, raising concerns about China's ability to withstand a resurgence of 'America First' policies. -

Diversify Your Portfolio Through the Commodity

As Donald Trump returns to White House, his policy agenda could send ripples through the global oil market. His trade wars and immigration stance are expected to fuel inflation, while his commitment to deregulation and to increasing US oil production pose new challenges for oil prices. -

Hello ChatGPT: Will AI continue to surprise the world?

If investors are expected to be early in detecting future trends, then our community certainly thinks AI is the future. Will the surprises continue? To help train ChatGPT’s response, we analyse the tangible revenue that has emerged so far, and consider the ‘sweet spot’, the ‘runners-up’ and the ‘too early’. -

The 2025 European Banking Puzzle: Risks, Rewards, and Regulation

Conflicting or competing regulatory regimes on both sides of the Atlantic, a changing rates environment with central banks in easing mode, and consolidation are the new trends to watch in the European banking sector as we head into 2025. Select carefully and keep an eye on the emissions. -

A New Dawn for European Real Estate? Navigating a Path to Recovery

While easing interest rate pressure may bring some relief to the European property market, some challenges remain, making selectivity crucial in navigating today's uncertain environment.