Will the pace of mergers & acquisitions (M&A) run out of steam one day? This is a legitimate question for investors to ask, as the past 5 years have seen a heavy M&A dealflow, which has created significant value. Since 2014, almost 1,300 deals have been launched in the European and US markets, including takeovers of all sizes totalling over 7,700 billion dollars[1].

Although the scale of these incredible statistics is giddying, the reasons are clearly identified:

- Interest rates are close to zero, which enables companies to borrow at low costs;

- Markets have been bullish, and this gives companies the chance to deploy their shareholders’ equity to fund their transactions;

- The failure of economic growth to trigger stronger earnings momentum has incited companies to expand through bolt-on growth;

- The geopolitical context has been relatively stable despite the Brexit and the trade war between China and the US.

2019 has not proved to be an exception, as at the end of August more than 155 deals had been announced in Europe and the US, representing almost 1,000 billion dollars[2].

2020: the same causes and effects?

Will the coming year extend this trend? It would appear so, as nothing has changed significantly.

Sources of tension have certainly not been lifted and should therefore lead to continued uncertainty.

- The chaotic Brexit resolution has impacted the number of deals in Europe and driven the UK, traditionally a leader in the European M&A market, towards defensive domestic transactions rather than targeting the continent. This trend appeared to be inverting during the last quarter of 2019, however.

- The trend towards a smaller number of deals in the oil sector, due to tensions in Iran and North Korea, is expected to continue.

- Spreads among certain deals should remain volatile due to the trade war between China and the US. These include Mellanox Technologies, which is being taken over by Nvidia. The spread almost doubled during the summer following a tweet from Donald Trump sparking fears that the Chinese antitrust regulator would block the deal.

Aside from these specific periodic issues, leading M&A indicators are still flashing green.

- The economic and market context is still showing growth, while the cost of borrowing is also still extremely cheap to finance deals, and volatility remains low.

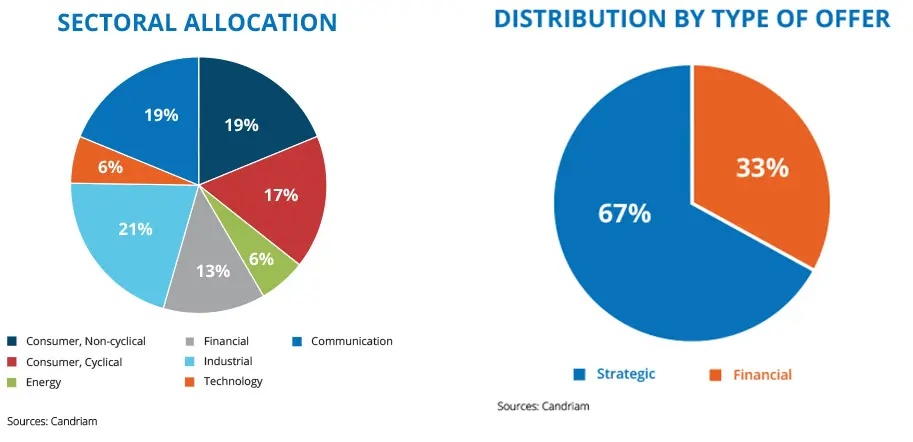

Deal sector breakdown remains highly diversified. - Although the proportion of financial deals (LBOs, MBOs, private equity) increased sharply during the second half of the year, their weight still remains far below industrial transactions. It should be highlighted that the number of LBOs collapsed in 2007, when credit facilities available in the interbank market suddenly dried up.

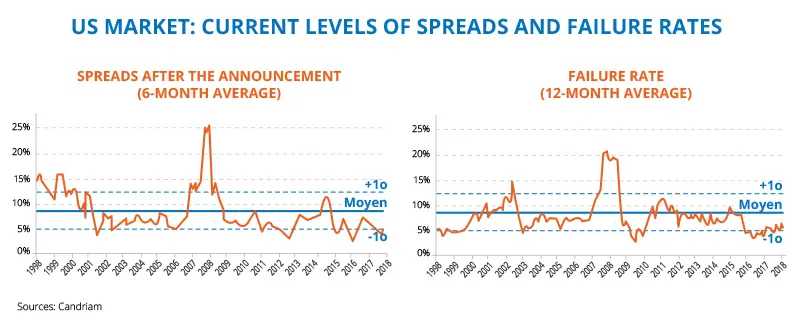

- Lastly, although spreads are tight, the deal break ratio remains extremely low, which is reassuring for the coming months.

Several growth drivers

All of the required conditions are in place for corporate managers to feel more confident about acquiring or merging with other companies. This is why negotiators always refer to “boardroom confidence” as a leading indicator for the mergers & acquisitions market. Confidence remains high and we cannot see any reason for that to change in the short term:

-

Available cash for merger & acquisition deals remains very high;

- Activist shareholders seek returns by continuing to put considerable pressure on companies to undertake mergers or acquisitions and therefore create greater value;

- In choosing between starting a project from scratch or buying a business, the latter option is more rapid and a safer bet, according to pharmaceutical companies, and as illustrated by the recent $5 billion takeover of Spark Therapeutics by Roche and the bid on The Medicines Company by Novartis valued at $9.7bn;

- Lastly, the uberisation of entire segments of the economy is inciting traditional players to plunge into the digital era by taking control of the challengers within the new economy.

A strategy which still makes perfect sense

In other words, all of the catalysts for a strategy aiming to capture value created by merger & acquisition deals are still in place.

----

[1]&[2] Deals recorded by the management team in the MAGMA proprietary database.