Long viewed as a model, the German economy is now slowing. After the elections, can it regain its competitive edge?

Between 2005 and 2017, when most Eurozone economies saw declines in both the weight of their industries and their export market shares, Germany stood out for its powerful industry, strong market shares... and its fiscal rigor. Over this period, German GDP grew 10% faster than the rest of the zone.[1] Germany and its social co-management model (Mitbestimmung) have long been held up as the example.

Yet, as early as the mid-2000s, questions were already arising over the future of Rhineland capitalism. The findings of F. Pesin and C. Strassel,[2] among others, were severe: Industrial success in "trompe-l'œil", competitiveness without growth, pupils whose performance has fallen below the OECD average, and an apprenticeship system showing serious signs of running out of steam.

Twenty years on, the situation is even more worrying. The German economy is stagnating and even seems to be falling behind its European partners. While most Eurozone countries have returned to their pre-Covid growth trends, Germany's GDP is more than 6%[3] below. In real terms, it has not grown since 2019! Household consumption has stalled, residential investment has contracted by 10%, and despite a 10% rise in investment in intellectual property rights (R&D), total business investment has nonetheless fallen by some 5%. Exports, the mainstay of the German economy, have been at a standstill since... 2017. Worse still, like Italy, France, and Spain before it, Germany is losing export market shares.

The industry in slow motion

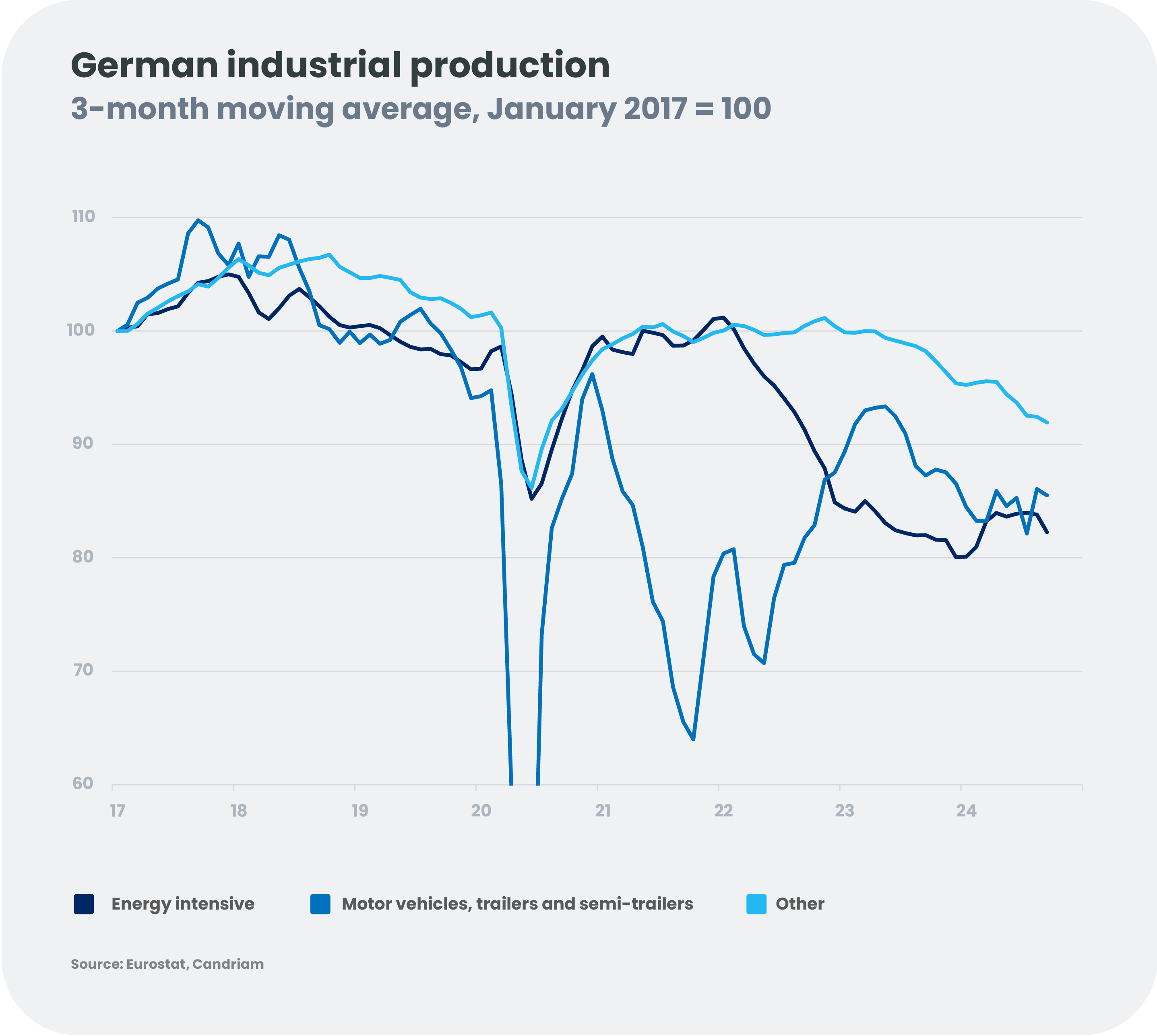

Germany’s growth engine, the industrial sector, is broken. The automotive sector, representing close to 5% of GDP and 16% of exports of goods[4] and already reeling from the dieselgate scandal, is facing sluggish demand in Europe: For many consumers, high-end versions are too expensive and in major cities, they are less and less popular due to traffic restrictions. The sector is also facing a slowdown in demand in China, and competition from Chinese manufacturers whose prices are much more competitive -- and who are now competing with German manufacturers on their own soil, particularly in electric vehicles. Rising energy prices have not helped. Since the beginning of 2022, industrial production in energy-intensive sectors -- particularly chemicals, which account for almost 4% of GDP and 17% of exports[5] -- has fallen by almost 20%.

A pressing need for investment

The conclusions of a recent report by the BDI -- the Federation of German Industry -- aptly sum up the disarray into which German industry has plunged. Without an investment effort of 1,400 billion euros by 2030 -- an amount almost twice that of the European "Next Generation EU" plan – the German industry will not be able to regain its competitiveness. This cry of alarm, coming from an organization traditionally in favour of free trade and free competition, is all the more astonishing given that the report suggests that a third of the funds should be provided by the public sector! Is this call for massive investment over the next few years likely to be heeded by Germany's leaders? Will Germany's industrial woes prompt it to loosen its debt brake and invest more at home to help the country regain its lustre? The fact that Chancellor Olaf Scholz has finally decided to part company with his Finance Minister, Christian Lindner (who is adamant about defending the budget brake), might suggest that at least part of the German political class is willing to go down this road.

Economic policy, a key issue in the upcoming elections?

Both the Bundesbank and the Sachverständigenrat -- the Economic Council of the Wise Men – also seem in favour of a reform that would slightly increase the flexibility of fiscal policy, without jeopardizing the sustainability of public debt. However, the window of opportunity to achieve this is narrow. The political process in Germany is set to culminate in early elections (scheduled for 23 February, 2025), which according to the latest polls would give the FDP, AFD and BSW, all opposed to any reform, a blocking minority. Aware of the risk of failing to muster a qualified two-thirds majority in the new Bundestag, Friedrich Merz, President of the current opposition party Christian Democratic Union (CDU), seems increasingly willing to discuss a reform of the debt brake before the elections. This would undeniably provide a little more breathing space to the next government, which, according to the latest polls, could be led by the CDU! It could also prevent an unnecessarily restrictive fiscal policy from depressing an already-sluggish economy.

It remains to be seen whether the Germans will have the wisdom to bring to power parties prepared to invest in the physical and social infrastructures that could enable Germany to return to competitiveness in the future. We must hope so, for Germany of course, but also for Europe...

[1] Source: Eurostat

[2] F. Pesin and C. Strassel, Le modèle allemand en question, Economica, 2006.

[3] Source: Eurostat (all data in this paragraph)

[4] Source: Eurostat

[5] Source: Eurostat

-

Outlook 2025, Nadège Dufossé

Outlook 2025, Nadège DufosséAsset Allocation in 2025: Between Optimism and Uncertainties

Global growth progresses in line with expectations, but the economic landscape remains fragmented. While activity is strong in the United States, the Eurozone is struggling to move forward, and China is penalised by weak consumption. Geopolitical tensions and the rise of political uncertainty in several countries risk exacerbating these divergences in 2025. -

Outlook 2025, Steeve Brument, Bertrand Dardenne

Outlook 2025, Steeve Brument, Bertrand DardenneM&A: Triple Trends for 2025?

As we head into 2025, the stars seem to be aligning for a revival of mergers and acquisitions, creating a fertile environment for investors seeking new opportunities. Merger arbitrage strategies attempt to capitalize on M&A activity by using a structured approach returns. -

Outlook 2025, Alix Chosson, Tanguy Cornet

Outlook 2025, Alix Chosson, Tanguy Cornet2025: the swan song for global climate action?

2024 concluded as another annus horribilis for climate action, with COP29 blowing “hot air”, reinforced geopolitical tensions overshadowing the climate crisis, and the re-election of Donald Trump in the U.S. We only have a couple of years left before spending the totality of the +1.5°C carbon budget. How will the recent political changes and global geopolitical tensions impact the transition? -

Outlook 2025, Christopher Mey, Paulo Salazar

Outlook 2025, Christopher Mey, Paulo SalazarIs China ready for another Trump fight?

With Donald Trump returning to the White House in 2025, his second term is likely to see a resurgence of tariffs and export restrictions among other things, raising concerns about China's ability to withstand a resurgence of 'America First' policies. -

Outlook 2025, Thibaut Dorlet, Nicolas Rutsaert, Nicolas Cleris

Outlook 2025, Thibaut Dorlet, Nicolas Rutsaert, Nicolas ClerisDiversify Your Portfolio Through the Commodity

As Donald Trump returns to White House, his policy agenda could send ripples through the global oil market. His trade wars and immigration stance are expected to fuel inflation, while his commitment to deregulation and to increasing US oil production pose new challenges for oil prices. -

Johan Van der Biest, Vincent Compiègne, Alfred Sandeman, Outlook 2025

Johan Van der Biest, Vincent Compiègne, Alfred Sandeman, Outlook 2025Hello ChatGPT: Will AI continue to surprise the world?

If investors are expected to be early in detecting future trends, then our community certainly thinks AI is the future. Will the surprises continue? To help train ChatGPT’s response, we analyse the tangible revenue that has emerged so far, and consider the ‘sweet spot’, the ‘runners-up’ and the ‘too early’. -

Christian Solé, Thomas Madesclaire, Lucia Meloni, Outlook 2025

Christian Solé, Thomas Madesclaire, Lucia Meloni, Outlook 2025The 2025 European Banking Puzzle: Risks, Rewards, and Regulation

Conflicting or competing regulatory regimes on both sides of the Atlantic, a changing rates environment with central banks in easing mode, and consolidation are the new trends to watch in the European banking sector as we head into 2025. Select carefully and keep an eye on the emissions. -

Lucie Hamadache, Christian Solé, Rémi Savage, Outlook 2025

Lucie Hamadache, Christian Solé, Rémi Savage, Outlook 2025A New Dawn for European Real Estate? Navigating a Path to Recovery

While easing interest rate pressure may bring some relief to the European property market, some challenges remain, making selectivity crucial in navigating today's uncertain environment.