Navigating fixed income markets can be a daunting task for those unfamiliar with their intricacies. A multitude of factors – fundamentals, valuations and technicals – can impact a wide range of instruments – sovereigns (developed & emerging), corporates (investment grade and high yield) –, contributing to a highly complex financial landscape. Achieving a comprehensive understanding of these dynamics often requires careful analysis and repeated engagement before one can effectively position a portfolio.

With a distinguished track record spanning over 25 years, Candriam manages €24 billion in fixed income, drawing on the expertise of more than 40 investment professionals and 26 ESG analysts[1]. This depth of knowledge enables us to provide valuable insights into evolving market trends. Each month, Charudatta Shende, our Fixed Income Strategist, offers expert perspectives to help investors navigate the market with clarity and confidence.

Shifts in Credit Markets: Rising Yields and Investor Implications

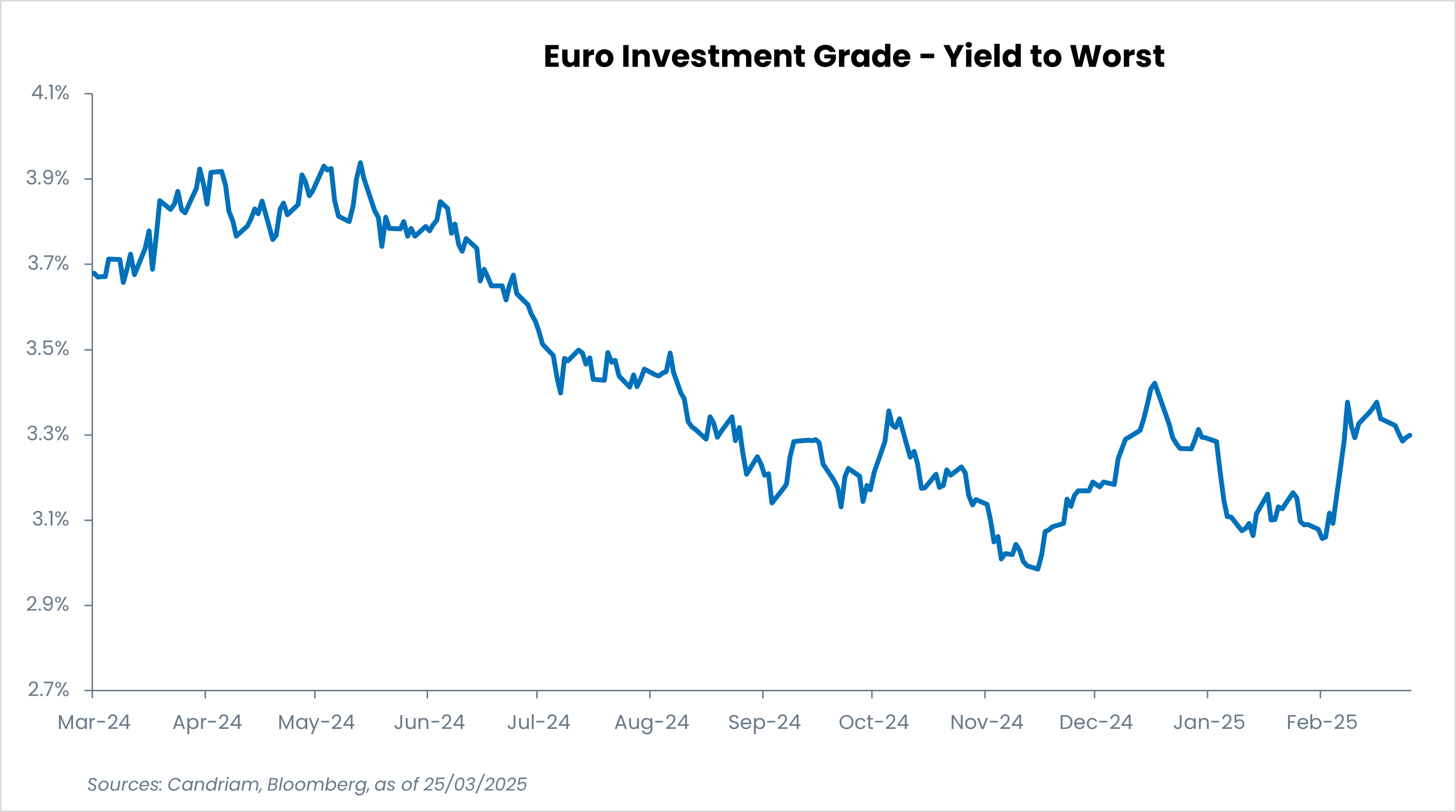

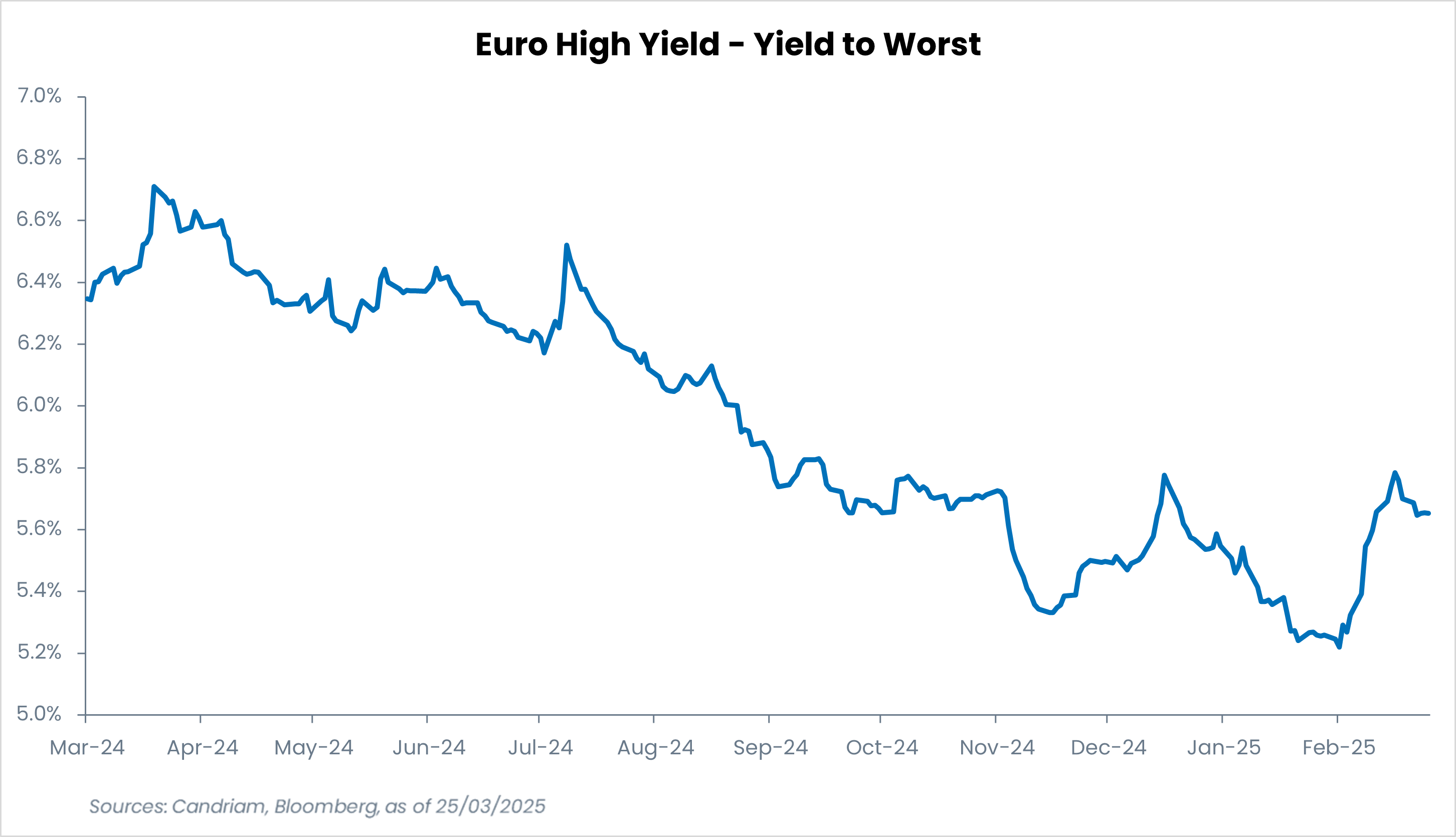

Credit markets have undergone a shift in recent weeks, primarily driven by rising sovereign yields. The European credit landscape, in particular, has seen notable developments as Euro-area interest rates spiked, fuelled by Germany’s anticipated fiscal stimulus and increased debt issuance. This surge has led to an increase in carry on European credit. The announcement of large-scale public spending and support for key sectors has triggered expectations of increased government bond supply, pushing yields higher. Consequently, corporate bond yields have risen, offering investors attractive return opportunities. With carry levels at 3.4% for Euro Investment Grade (IG) and 5.5% for Euro High Yield (HY)[2], investors are increasingly drawn to locking in these returns. Moreover, the resilience of credit markets during this yield widening phase further boosts investor confidence. However, risks remain, stemming from market volatility and uncertainty in global financial markets.

Credit yields remain attractive

Market stability and Emerging Risks: balancing Opportunities and Caution

Despite this resilience of credit markets in the face of higher yields, caution remains essential. The current stability can largely be attributed to favourable market technicals, including substantial flows into investment-grade credit and limited issuance in the high-yield segment. These technical factors have played a crucial role in containing spread volatility. However, this stability is fragile. A spike in volatility or negative news flow could prompt investors to retreat from the credit asset class, potentially challenging the stability of spreads. Another key supporting factor has been the relative stability of corporate fundamentals. Strong balance sheets and low default rates have provided issuers with some degree of insulation from macroeconomic shocks. So far, credit markets have seen net positive rating actions, with an increasing number of rising stars [3] reflecting issuer strength. However, as economic conditions evolve, this stability could be tested, particularly in sectors more exposed to cyclical downturns or geopolitical risks.

The imposition of tariffs by the Trump administration has introduced additional uncertainty into the global economic landscape. These tariffs have direct implications for the European and global economies, particularly affecting cyclical sectors such as retail and automotive. Beyond growth concerns, tariffs also pose inflationary risks, prompting both the Federal Reserve (Fed) and the European Central Bank (ECB) to reassess their policy stance. The ECB recently executed a "hawkish cut," while the Fed opted to remain on hold. If inflation remains sticky, interest rates could remain elevated for longer, potentially increasing default risks among weaker credit issuers and heightening refinancing challenges for highly leveraged companies. In this environment, idiosyncratic risks [4] are rising, particularly among weaker high-yield credits and fragile crossover names [5].

A cautious investment approach is essential in such an environment. Key indicators such as fund flows, central bank rhetoric, and tariff-related developments, must be closely monitored. Investors should focus on resilient sectors and high-quality issuers.

Selectivity in the Investment-grade Segment

Within the investment-grade segment, financials present an attractive opportunity, particularly as they stand to benefit from yield curve steepening. We favour national champions—institutions with strong capitalisation, solid return on equity (ROE), and robust interest coverage ratios. In the subordinated debt space, we maintain a long-term positive outlook, while ensuring that risk premiums adequately compensate for associated risks. Additionally, defensive sectors such as utilities and telecommunications are well-positioned to withstand market volatility, given their stable cash flows and strong credit profiles. Conversely, more economically-sensitive industries, such as industrials and consumer discretionary, require a more prudent approach.

High-yield: Focus on High-quality Names in Defensive Sectors

In the high-yield market, a selective approach is also paramount. While recent spread widening in US hybrid names [6] has created opportunities, we prefer to remain cautious. We prioritise higher-quality issuers and defensive sectors, underweighting industries like autos and retail that are more vulnerable to macroeconomic pressures. Non-cyclical sectors such as healthcare and consumer staples offer relative stability within the HY space. Additionally, select energy-related credits with strong balance sheets and sustainable cash-flows have displayed resilience. However, speculative-grade issuers with weak fundamentals remain at risk, particularly if refinancing conditions deteriorate.

We advocate for active management and selectivity

The recent evolution of credit markets presents both opportunities and risks. While higher yields enhance carry potential, macroeconomic headwinds, fragile technical factors, and sector-specific vulnerabilities demand a prudent approach. Given the complexities of the current credit environment, active and selective management is more critical than ever. Market complacency appears to be settling in, underscoring the need to differentiate between resilient and vulnerable segments. By maintaining rigorous risk assessment and monitoring sector-specific dynamics and key indicators, investors can navigate credit markets with greater confidence and stability. Selectivity, active management, and a focus on high-quality issuers, portfolio flexibility, and responsiveness to market signals will enable credit investors to navigate potential challenges while capitalising on attractive investment opportunities in this evolving landscape.