Although the peak in coronavirus is behind us, asset managers and investors find themselves again in unchartered territory: what does a “re-opening economy” look like? Are financial integrating the normalisation of the situation? The easing of lockdown is a delicate step to manage. If it goes too quickly, a second wave is a risk. If it goes too slowly, the downturn in the economy might be unavoidable within the hoped-for timeframe. We are not out of the woods yet and the next leg of the race is becoming bumpy – at least in the US – where the evolution of the epidemic is less predictable than in Europe or Emerging markets. We remain globally cautious while adding risk in a very selective way.

Equities vs. bonds

The coronavirus is not old news yet but the focus is increasingly shifting. What matters now is whether financial markets have integrated the normalisation of the situation. Both bonds and equity valuations are globally not cheap anymore. It was the quality names, growth and defensives sectors that benefited most from the rebound. As mobility trends increase, financial markets have partly recovered. The re-opening of economies is finally happening and is going well for a majority of countries. Volatility has also decreased and market sentiment is now more neutral. Risks of a second wave will persist and will remain on the side-line of that path to normalisation in financial markets. As a result, we remain underweight equities and have added protective derivatives strategies. The economic damage that the coronavirus triggered at a time when economies were already challenged by low growth, low inflation and low rates will outlive the virus, as will the policy responses from central banks and governments.

EMU: The investable region for bonds and equities

In the euro zone, where the shock first highlighted the North versus South divide, the policy response is improving in terms of coordination among member states. We have recently gone from one positive surprise to another:

- The virus is under control in most euro zone countries

- The risk to peripheral countries, less solvent, has decreased with the ECB’s multiple interventions

- Fiscal stimulus and solidarity, with the risk of fragmentation being addressed and grants being allocated to Spain and Italy

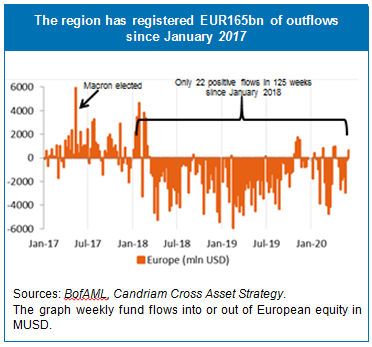

- The region has been under-owned after years of scepticism. Within the past 3 years, there have been €165bn in outflows.

As we observed structural changes in the Eurozone that could lead to a more persistent decrease in the risk premium, we decided to focus our allocation on:

- EMU value sectors, such as banks, over the broad EMU markets, and

- peripheral bonds over the broad bond markets.

In the US, the government and the Fed have also given the strongest monetary and fiscal support. This is also where the data point towards the least economic damage. However, standing president Donald Trump is being caught up by his poorly rated handling of the coronavirus crisis and social unrest, and his approval rating is decreasing in a crucial re-election year. The valuation of US equities is relatively less attractive after a strong rebound since March. We have decided to underweight US equities.

The main risks

Since mid-May, investors have mainly focused on the improving news: peaking and decreasing active covid-19 cases, resumption of pre-coronavirus activity levels, business sentiment, PMI, massive intervention from the central banks and increasing help to households and corporations to counteract the impact of the coronavirus; that said, risks persist.

The domino effect

The coronavirus itself, with its crushing weight on healthcare systems and its casualties, is not the only issue per se. Instead, we’re looking at where the domino effect will start and stop as the virus will be outlived by its economic damages. The road to recovery will certainly last longer than the epidemic and so will the policy responses. A peak – or lingering unemployment, bankruptcies and lower investments – could impact the economy in a durable way and we will keep monitoring those.

US elections

US elections usually slowly but surely gain in importance months ahead of D-day. Not so much here. The US elections will take place on November 3rd but are not yet a hot topic. Standing president Trump has been heavily criticized for his handling of:

- the pandemic,

- the economic crisis,

- the social unrest due to the death of George Floyd while in police custody.

While his approval rate has decreased, not only have the odds in favour of his Democrat opponent Joe Biden risen but also in favour of a Democratic Senate while the Democrats keep the House of Representatives.

Whatever the outcome, presidential elections usually trigger some volatility on financial markets and the upcoming election will certainly not be an exception.

Brexit

As the end of June is the deadline by which UK prime minister Boris Johnson has to ask the EU for an extension to Brexit, the topic has been increasingly gaining in importance. In spite of time passing by, negotiations of trade relations have made little progress. As a consequence, there is rising concern about a no-deal end to the transition period for the UK’s exit from the EU. It could end up being either:

- a ‘thin’ free trade agreement — incorporating zero-tariff/zero-quota trade in goods, but significant non-tariff barriers on trade in services — to be struck by the end of the year, which is a realistic assumption or

- a no-deal end to the transition (or just rising uncertainty around any deal or lack thereof), which would hit foremost UK domestic stocks

What’s in our portfolio?

As a multi-asset asset manager, we consider all options on the table and our investment universe is wide. Our in-depth analyses result in a multi-asset strategy that emphasizes:

The need to hedge and use protection on equities via options. We also use gold and yen.

The opportunities that can be found in the Eurozone on both the equity and the bond side. We have gone long European equities and value sectors over US equities. We have also gone long peripheral bonds vs. core countries. We stay underweight duration.

Further to the equities side, we remain neutral Japanese and Emerging equities. We also remain underweight Europe ex-EMU equities.

Further to the fixed income universe, we hold emerging debt in local currency, European and US investment grade bonds while staying neutral high yield.

In our latest transactions, we have taken profit, or partial profit, on “cyclical” trades that had strongly rebounded: for instance, on the European automotive sector.