Governments have started laying out plans to reduce confinement. In most cases, they have succeeded in bending the curve in terms of infections and thereby also reduced the pressure on healthcare services. The objective is now to re-open economies before they dwindle more than necessary. But lockdown-easing will be a moment of truth. A second wave of epidemic is a real possibility and the current surge in cases in areas of de-confinement is comparable to a sword of Damocles. Another challenge will be inter-governmental coordination – in the European Union and in the US – to kick-start local economies when individual states could not always agree either on the degree or the length of confinement in the first place. Our newly-defined Candriam House View will hence highlight those anticipated structural changes and opportunistic choices.

Equities vs. bonds

So far, this year, alongside the coronavirus outbreak, financial markets have dived. By the end of April, only gold and US government bonds had performed positively. By mid-May, global equity markets, although still in the red, had recovered roughly half their decline. The fiscal and monetary stimuli rapidly announced and put into place were strong supportive. Equity markets are now trading in a range, looking for direction. Will markets find some stability? The way forward will be determined, among other things, by the evolution of the epidemic. If it lingers, or worsens, confinement measures will be re-applied and, with that, economies come to a halt. If the epidemic finally slows down in a durable manner, countries will gradually be able to re-open while imposing a series of security measures: we are by now all too familiar with wearing a mask in public spaces and keeping our distance. As European countries are progressively exiting containment, a second wave of covid-19 is the main risk. This would hurt confidence, could trigger new containment measures and weigh on economic recovery. Market risk, valuation, epidemic-linked indicators, activity levels and policy response have all impacted our asset allocation. We currently remain underweight equities.

Equities

Regional equities and their inherent bias

Let’s start with what regions have in common: very active central banks and governments – although the European Union has the additional challenge of finding compromises with the many Member States. We are confident that authorities, central banks and governments will do “whatever it takes” to avoid a financial crisis in addition to the healthcare and economic crisis. Monetary policy responses will ensure ample liquidity and, in some cases, further quantitative easing. Fiscal policy responses will temporarily ease the tax burden on households and corporates and ensure unemployment benefits in an effort to sustain or boost demand. In the US, especially, the response has been massive: The Coronavirus Aid, Relief, and Economic Security (CARES) Act can be expressed in trillions, not billions, of USD and is geared towards avoiding dramatic disruptions in income and financial flows. It includes additional funding to public services, loan guarantees to businesses and states, tax cuts, guarantees and loan forgiveness for payroll, rent and mortgage interest, utilities for small and mid-size companies, and income support to households. In the European Union, announced fiscal packages represent at the very least 4.5-5% of each Member State’s GDP and a budget deficit closer to 15% of GDP in the US. Because we anticipate that both fiscal and monetary policy responses will outlive the virus, our regional allocation to US equities has recently been upgraded from underweight to neutral. US equity valuation, although seemingly expensive compared to its historical average, is, in our opinion, justified. The Trump administration and the Fed are providing a very high level of fiscal and monetary support. GDP will contract but less than in Europe and forecasts for 2021 anticipate a realistic catch-up. Same for earnings growth. In Europe, the response from the European Investment Bank and the various governments comes with more strings attached. Germany, for instance, has excluded the issuance of Eurobonds as an instrument of joint responsibility. Nevertheless, we are neutral EMU equities and aware that certain sectors are trading at a discount. We are also neutral Emerging markets and Japanese equities, and underweight Europe ex-EMU equities.

Within those regions, we are, however, very selective, in terms of sectors, and opportunistic in terms of style.

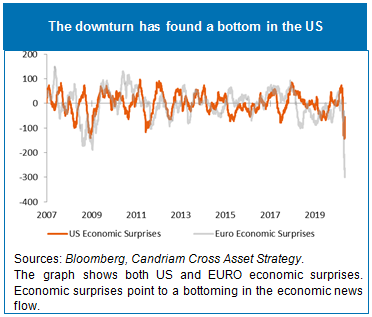

Within the US – where the downturn seems to have bottomed – we have a preference for the technology sector.

The graph shows both US and EURO economic surprises. Economic surprises point to a bottoming in the economic news flow.

It is, in our opinion, one of the thematics that is already benefiting from the life changes initiated or boosted by the corona crisis. Healthcare will become an even greater focus for citizens and governments, and valuations have recently risen. Sustainability will continue to take "share of mind", including greater attention to social and environmental aspects.

Within EMU equities, we have adopted a more opportunistic style. The crisis has brought some historically attractive valuation levels to various sectors, that cannot be bypassed:

- Banks have so far performed poorly, offering significant upside potential from a bottom-up perspective;

- The automotive sector has also garnered investors’ attention for its valuation.

That said, we are well aware that the European political response needs to be improved. EU leaders have agreed on the need for a European Recovery Fund post “corona” but the scope is still unclear.

Underweight Europe ex-EMU

The region is facing two challenges:

- The corona crisis, i.e. getting the virus under control and re-opening the economy in a safe way; but also

- Renegotiating trade relations between the EU and all of its partners, including the US.

The country has also already made it clear that the UK’s withdrawal from the EU will not be delayed beyond 31 December 2020.

Neutral Emerging markets & Japan

Relations between the US and China will likely remain on edge for the coming months. This is clouding local and global growth, and impacting open economies like Japan, which are highly dependent on external trade.

nbsp;

Fixed Income & Currencies

In the fixed income universe, government bonds have temporarily benefited from the flight to quality but, in the long term, we anticipate that yields will stay low.

We are therefore diversifying into investment grade bonds in both Europe and the US. Central banks’ buying and helping corporates with loans and grants will be supportive of the asset class.

We are also diversifying into Emerging Market Debt to catch some carry. Not only does this asset class have an attractive carry, it also has spread-compression potential. In addition, as emerging currencies are at historically low levels of valuation, we have exposure to both hard and local currencies.

In volatile markets, it is not easy to find the best entry point but, for a long-term investor, it makes sense to strengthen the position.

In terms of currency, we already had exposure to the YEN, a faithful safe haven. We recently bought NOK vs EUR as the Norges Central Bank had put a limit to its currency depreciation after a 30% decline. We also have some gold.

nbsp;

Outlook

Our main scenario – that of a global, deep, but temporary, shock due to the pandemic – hasn’t changed. Although it will probably take more time than initially thought to revert to “normal” levels of activity, we still believe in a U-shaped economic recovery.