Diversify Your Portfolio Through the Commodity

As Donald Trump returns to White House, his policy agenda could send ripples through the global oil market. His trade wars and immigration stance are expected to fuel inflation, while his commitment to deregulation and to increasing US oil production pose new challenges for oil prices. The interplay among these policies and broader geopolitical and economic factors could redefine the energy landscape. Despite challenges, the oil and gas sector is adapting effectively to a shifting landscape, balancing operational efficiency with financial discipline to navigate heightened uncertainty. What does this mean for investors?

Slower Oil Demand Growth in 2025, and beyond?

Global oil demand is expected to grow slightly in 2025, increasing by around 1 million barrels per day to 103.8 mbd, according to the International Energy Agency (IEA). This slower growth reflects weaker economic conditions, the waning of the post-pandemic recovery, and the shift toward cleaner energy. Demand from China, a key driver of growth in recent years, is also expected to level off.

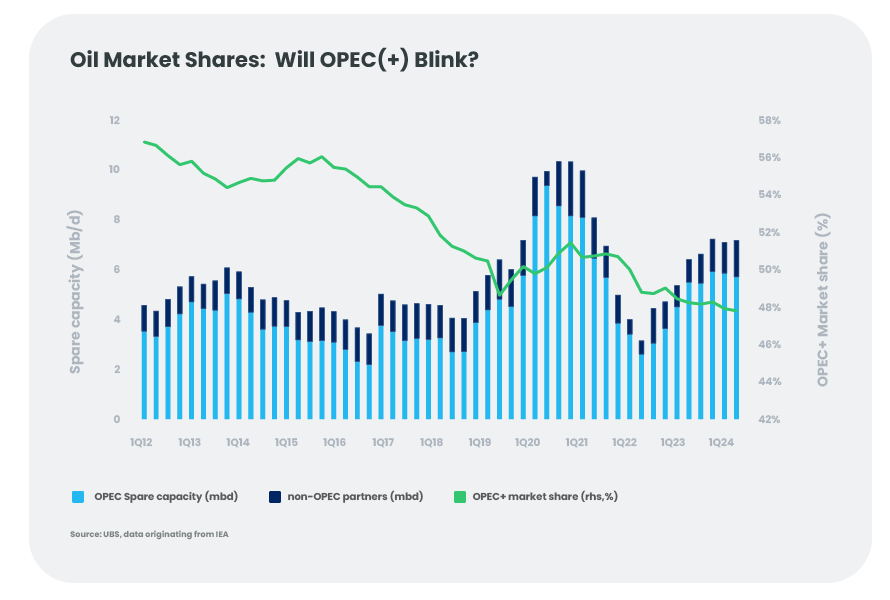

Balancing supply and demand will require careful coordination among OPEC+ members. Together, these 22 oil-producing nations in OPEC+ (the 12 OPEC nations and the additional 10 ‘non-OPEC partners’ who are included in OPEC+)1 are losing market share. Many want and/or need additional revenue, and we remain sceptical of their December 2024 production quota goals. We see room for OPEC+ to raise production in 2025. To add to dilemma faced by producing countries, global oil demand is expected to peak by the end of the decade and decline further by 2035.2 Plenty to this story to hold our interest!

Balancing Fundamentals, Politics, and Risk

In 2025, oil prices face both downside and upside influences, across the range of geopolitical, economic, and policy factors. We expect Brent crude prices to average around $70 per barrel in 2025 -- slightly above current market expectations but below the oil price necessary to keep many newer oil projects profitable. Depending on how these risks unfold, prices could range between $50 and $80 per barrel. This very wide range reflects how numerous and complex the risks are for 2025. Our range is wider on the downside than the upside because of the excess production capacity globally.

The US policy paradox stems from the promises made by President-elect Trump to keep inflation in check. Higher tariffs and tougher immigration polices, cornerstones of his policies, are both inflationary. We estimate that to offset the inflation of these two policies would require an oil price of $40 per barrel. But Trump’s pro-oil “Drill, baby, drill!” promise to the oil industry requires oil prices of $70 or higher to protect the US shale oil industry.

Middle East Tensions remain a potential upside for oil prices, especially if conflicts between Israel and Iran were to escalate.

Energy Sector Investments: Navigating Volatility and Adapting Strategies

Despite challenges, the oil and gas sector is adapting effectively to a shifting landscape, becoming more operationally efficient and increasing financial discipline,

Equity Outlook: Earnings are under pressure from global overcapacity, but downside risks appear limited. Companies are adapting to the uncertainty by cutting capital investments and adjusting share buyback programs. Recent declines in share prices have improved the relative value of the equity. Considering the already negative sentiment, we are neutral on the equities in the energy sector.

Bond Outlook: The US high-yield energy industry bonds face a slightly higher risk profile in 2025 compared to 2024, although company fixed income fundamentals are strong. Firms are maintaining high credit ratings and strong liquidity. If oil prices were to fall further, the valuation of the bonds could suffer, but we would not expect a significant increase in defaults. We remain unenthusiastic.

Conclusion: Diversify Into the Real Thing

The outlook for the oil equity and credit sectors remains subdued, but the global environment highlights the value of commodities as portfolio diversifiers. Even with expectations of weaker oil prices, with the support of a financial professional, a long position in oil as a commodity could serve as a hedge against geopolitical risks, offering investors some protection.

[1] L'OPEP (Organisation des pays exportateurs de pétrole) compte actuellement 12 pays membres (membres fondateurs et membres à part entière) : l’Iran, l’Irak, le Koweït, l’Arabie saoudite, le Venezuela, la Libye, les Émirats arabes unis, l’Algérie, le Nigeria, le Gabon, la Guinée équatoriale et le Congo. Depuis 2016, l'OPEP+ compte dix "non-membres", comme le montre le graphique, à savoir l'Azerbaïdjan, le Bahreïn, le Brunei, le Kazakhstan, la Malaisie, le Mexique, Oman, la Russie, le Soudan du Sud et le Soudan.

[2] IEA, Oil Market Report, novembre 2024.

[3] IEA, Oil 2024 Analysis and forecasts to 2030.

-

Outlook 2025, Christopher Mey, Paulo Salazar

Outlook 2025, Christopher Mey, Paulo SalazarIs China ready for another Trump fight?

With Donald Trump returning to the White House, tensions between the U.S. and China could rise again. His administration is expected to reintroduce tariffs and trade restrictions as part of an "America First" agenda, putting pressure on China’s already struggling economy. -

Outlook 2025, Thibaut Dorlet, Nicolas Rutsaert, Nicolas Cleris

Outlook 2025, Thibaut Dorlet, Nicolas Rutsaert, Nicolas ClerisTry a Cup of Texas Tea: Oil as a Diversifier

As Donald Trump returns to White House, his policies could send ripples through the global oil market. These new effects add to the broader geopolitical and economic factors already faced. The interplay across all of these elements could redefine the energy landscape. -

Johan Van der Biest, Vincent Compiègne, Alfred Sandeman, Outlook 2025

Johan Van der Biest, Vincent Compiègne, Alfred Sandeman, Outlook 2025Hello ChatGPT: Will AI continue to surprise the world?

The power and the profit potential of AI are mesmerizing, and the equity markets have certainly benefitted from the dream.