The increase in rates in the US continued throughout the month of March, with, in April, some stabilization, driven by better macro (especially employment) numbers, the encouraging vaccination drive and the promise of even greater fiscal stimulus. US rates reached 1.75% in March, while hitherto oscillating German rates remained relatively stable, at -0.3%. While core bond markets posted mildly negative returns, positivism returned to markets as risky assets rose significantly, with peripheral sovereign bonds posting positive returns. Spread products such as credit markets (both Investment Grade and High Yield) and emerging debt also experienced a temporary surge towards the second fortnight of March. Though the overall mood has been positive, it is worth flagging that, in certain parts of the Eurozone, and even in certain emerging markets (India, Brazil), COVID cases have seen a sharp rise and confinement measures have returned, in some cases alongside lockdowns.

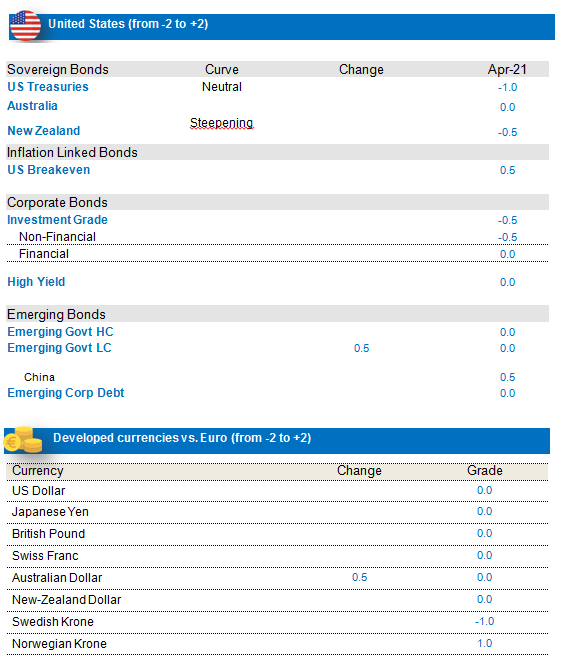

The US continues to maintain its lead versus other countries in terms of its macroeconomic outlook, with the economic recovery appearing to be at an advanced stage and our proprietary activity cycle looking more likely to enter into the expansion stage. Macro indicators are strong, after a small pause in February, and an extra 1 million jobs were added in March (though we probably won’t return to pre-COVID levels for some time). The two key elements behind the strength of the US outlook, however, appear to be the vaccine drive, where strong progress can be seen, and fiscal stimulus. Indeed, even in the midst of deployment of the current stimulus package, the Biden administration appears to be planning another multi-trillion fiscal support programme, which could further boost the American economy. The vaccine programme in Europe does not appear to be as successful as in the US or UK, though we expect a catch-up to take place as governments increase their efforts to have most of their populations vaccinated by end 2021. As a result of the delays, however, Europe appears to be lagging, in terms of the activity cycle, though data prints are still looking positive. Fiscal support also is likely to be reinforced in the Eurozone as national governments ponder additional support, while awaiting ratification of the current “Next Generation EU” package. Inflation data also appear to be a big contributor to the rising rates in the US, with the country now firmly in inflation territory. However, in the Eurozone and the UK, inflation is still lagging and in reflationary territory. While we expect the increase in inflation to continue, we believe that it is unlikely to turn the current rise in rates into a rate hiking cycle. This has been confirmed by the stance of the FED and the ECB, who have re-iterated their intention to continue their QE programmes and accommodative stance. The Fed, in particular, has also expressed its will to adopt a more flexible attitude towards inflation, allowing higher inflation levels to persist before acting. We hence recognize that the increase in core yields is likely to continue in the short term, and prudence – in this context – is warranted.

Negative stance on US rates

The return of growth and inflation is welcome in the US, and could continue on the back of the additional fiscal stimulus that has been voted and that is currently being deployed. Joe Biden’s agenda, focused on additional fiscal stimulus, should provide vital and much-needed support. In this context, we expect US rates to continue to move upwards. We also take note of the fact that short positioning on US rates has reduced, and the supply appears to be lower in April. Given the overall context, we hold a negative view on US rates, while taking some profit on trade, which has delivered performance. We also hold a positive stance on US inflation-linked bonds. The inflation cycle remains supportive, with US headline and core inflation expected to increase strongly over the coming two months. Combined with the high growth expectations for Q2 and Q3 2021, we revised our BEI target upwards. Lastly, US linkers continue to offer attractive carry and, though we take note that valuations at the front end of the curve are becoming stretched and that a change in risk sentiment could weigh on the asset class, we maintain our long conviction at this time.

The break-even inflation carry for US BEI trades relative to Euro BEI continues to be more favourable.

Our negative exposure to New Zealand rates continues on the back of some positive economic data, tapering of monetary support in the form of scalebacks in central bank asset purchases and a less attractive carry. We expect the curve to steepen further in the near term.

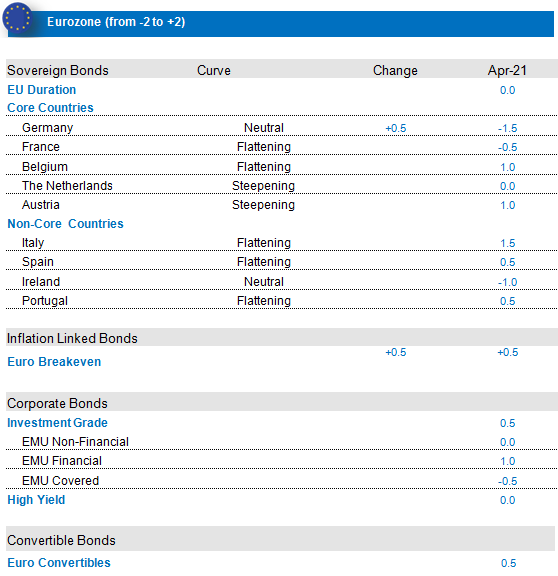

Negative bias on Germany and France but positive on Italy

Overall, cyclical indicators, both on economic activity and inflation, are still supportive of the expected eco-recovery. In spite of the fact that the budgetary cycle is less supportive of core European countries. Monetary policy, however, remains strongly positive, driven by the APP, the increased and extended PEPP announced in December and, finally, the announced higher pace of purchases announced in March to counter the impact of the coronavirus outbreak and weak inflation dynamics. This will continue to be a driving force of technicals for 2021, as net flows for Euro sovereigns will remain negative, supported also by EU issuance, which will also lighten funding pressure on sovereigns. For April, supply dynamics are very supportive. Lastly, fair value indicators continue to point to the expensiveness of core rates, and investor positioning indicates that the long duration trade is still crowded. In this context, we continue to hold an underweight position on core Eurozone markets (particularly in Germany and France) against peripherals.

The peripheral sovereign markets continue to be supported by fiscal and monetary policies, with the expected support from the European recovery fund with sizeable grants for non-core markets. Supply will be very supportive in April. In relative terms, versus core, flow dynamics are also improving for non-core countries. Positioning remains a negative driver, as long positioning remains high on non-core. While political risks have receded with the new Draghi government, it will be important to monitor the outcome of the German constitutional court’s decision on the Next Generation EU recovery fund’s ratification process. We maintain our preference for Italy and Spain.

Developed Market currencies: Long NOK vs. SEK

Our proprietary framework continues to point towards a negative view on the US dollar, on the back of twin deficits. However, with the improvement in growth and potential rise in economic activity, the Fed is likely to be more patient in the short term and not immediately add more stimulus. In this mixed context, the dollar could see a respite, following a period of weakness, thereby justifying our neutral stance.

We maintain our long NOK/short SEK. The Norges Bank has adopted a hawkish stance on the back of better inflation prints, paving the way for a potential rise in rates. On the other hand, the Swedish central bank has chosen quite a different approach, by extending and increasing the QE programme in December, and begun to become more verbal on the strength of the Krona while really cautious on the impact on inflation.

Credit: Favouring European credit markets

In spite of rates continuing their rise, Credit markets appeared quite resilient over the past month, even posting positive returns as the risk-on mood continued. While we continue to operate in a low-yield environment, it is clear that the substantial fiscal and monetary support and the vaccination programmes across the globe are leading to markets anticipating improvements in the macro-economic outlook. Finally, positioning is no longer as strong as previously witnessed, and supply is expected to be less strong than in the past. Furthermore, as credit spreads remain relatively attractive in a low-rate environment, investors are likely to continue to pile into the asset class.

EU IG & EU HY: Spreads have been remarkably resilient during the rising rate environment, with the long positioning and stretched valuations retracing somewhat. We expect higher yields to attract more buyers on the asset class. The improvement of medium-term perspectives, thanks to a more positive outlook on the fight against COVID-19, as well as ample monetary support, will continue to positively affect the European credit asset class. Issuers’ fundamentals are improving and we expect more rising stars over the course of the year. Deleveraging is underway and, as balance sheets are improving, we expect defaults to have reached peak levels and to move lower in the coming months. In this context, we hold a positive view on the Euro Investment Grade segment and, from a valuations perspective, we favour hybrids vs Senior debt while holding a favourable view on financials. The Euro financial sector should benefit from the rising rates and the steepening that has taken place, and riskier tranches such as AT1s offer a good yield pick-up. On the high-yield segment, we notice that BB vs BBB spreads are still at interesting levels in spite of the HY vs IG spread compression, and we hence favour the BB ratings. Once again, from a valuations perspective, we favour the hybrids sector over senior debt.

US IG. & US HY: Though our earnings expectations on US Credit remain strong, we believe that the balance sheet recovery has been fully priced in and we take note of the reappearance of M&As and slightly more aggressive supply dynamics on the Investment Grade front. In this context, we maintain an underweight positioning on US IG, while staying neutral and selective on the US High Yield front.

Finally, we think EUR Convertibles should benefit from positive dynamics such as the coordinated action from the EU Next Generation recovery fund, positive surprises/ better visibility from quarterly results, less political noise than in the US and some economic recovery of China.

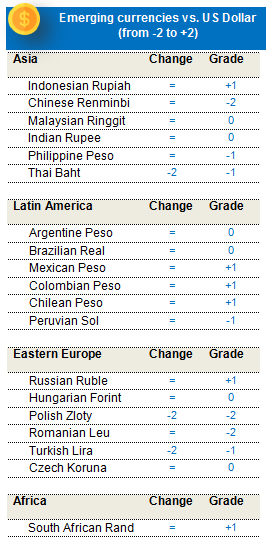

EMD: Positive on EM FX

Our Global Macro Score is neutral, helped by the still-abundant liquidity but held back by DM risk appetite indicators at overstretched levels. US rates pose a risk and we maintain a short bias, whereas China and commodities are unlikely to be major drivers, as China is no longer leading the recovery and commodities await more supply coming on-stream. Oil prices should stabilize as OPEC gradually increases production, the US oil rig count starts rising and Iranian production comes to market. These are still slow-moving factors, offset by the still-strong global demand and inventory drawdown. Industrial metals continue to be supported by infrastructure spending, but more supply is coming on-stream. Precious metals are under pressure from rising US real yields. As regards EMD segments, fundamentals are positive for corporates (low default rates) and EMFX (large external surpluses) but negative for rates (inflation picking up) and neutral for HC sovereigns (minor fiscal adjustment versus last year). Technicals are mostly challenging for sovereigns, due to supply expectations and more extended positioning, whereas EMFX and LC bonds have seen a clean-up in positioning. Valuation is attractive in HC (sovereigns and corporates) vs US HY, but more stretched, in absolute terms. Rates have gained some attractiveness, as curves have steepened, and EMFX – judging by REER levels – remains cheap.