European equities: Cyclical sectors clearly outperformed the broader market

Despite weak macroeconomic data (notably from Germany), European equities remained broadly flat in September, thanks to the announcement of the stimulus plan in China. However, Europe has faced the highest outflows since March 2022, to the benefit of emerging markets.

Despite weak macroeconomic data (notably from Germany), European equities remained broadly flat in September, thanks to the announcement of the stimulus plan in China. However, Europe has faced the highest outflows since March 2022, to the benefit of emerging markets.

With inflation cooling and activity relatively muted, the European Central Bank delivered its second rate cut in September (-25 bps), taking interest rates to 3.5%. Further rate cuts are expected by the end of the year.

Since the last committee in September, European equities have risen, with no strong performance dispersion between small/mid and large caps. Value stocks slightly outperformed growth stocks, for both large and small-/mid-caps.

Cyclical sectors clearly outperformed the broader market, with a positive performance across all sectors, notably driven by the announcement of the stimulus plan in China. The biggest outperformers were consumer discretionary and materials, followed by financials and industrials.

Conversely, defensive sectors came under pressure, with a negative performance for healthcare (mainly due to Novo Nordisk, which declined sharply), utilities and consumer staples. Energy was the only sector in positive territory, due to the Middle East conflict.

Lastly, information technology rebounded significantly, after its recent underperformance due to the weakness of the semiconductor segment, while communication services remained flat.

Earning expectations and valuations

Fundamentals remain well oriented for European equities, which continued to benefit from positive earnings revisions for 2025 and 2026 in all sectors.

12-month forward earnings are expected to grow by around 8% and are mainly supported by growth in technology, materials, healthcare, industrials and communication services. Energy and utilities remain the only sectors with negative earnings growth expected in the coming months.

European markets are trading at the bottom of their historical range when looking at the 12-month forward price-earnings ratio of 13.7 (stable vs last month). Technology and industrials are the most expensive sectors (P/E of 24.5 and 18.6x respectively), while energy and financials are the cheapest (7.9x and 9.0x respectively).

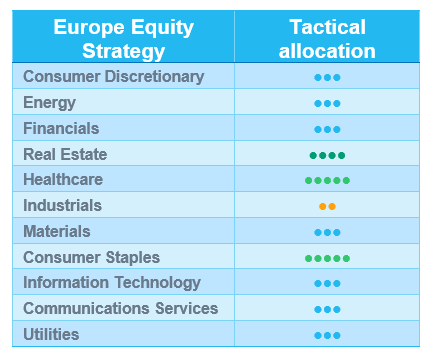

Household & Personal Care Downgraded To +1

During our monthly committee, we decided to downgrade HPC (household & personal care) from +2 to +1 for valuation reasons (Unilever, which accounts for 40% of the sub-sector, is very expensive after a 25% outperformance YTD). However, we maintain the current grade (+2) for consumer staples. This also includes food & beverage (+2), which remains attractive from a valuation standpoint and should benefit from an easy comparison basis in Q3.

We also maintain our positive (+2) rating on the healthcare sector, which offers an attractive risk-return profile thanks to reasonable valuations, strong cash flow visibility and projected earnings growth. Some companies in healthcare equipment (like Carl Zeiss) should benefit from their high exposure to China.

Lastly, we maintain the current grade (+1) on real estate, although a potential Trump victory would be a negative for the sector, as it would lead to higher long-term interest rates. We remain selective within the sector, as we favour certain niche segments (logistics, student houses and retirement homes) and avoid shopping malls and commercial properties.

US equities: Monetary easing makes a comeback

US equity markets have performed well in recent weeks, driven by the long-anticipated 50 basis point interest rate cut by the Federal Reserve and a substantial monetary and fiscal stimulus package from China. Despite weaker macroeconomic data, particularly in the eurozone, and ongoing geopolitical tensions, investor enthusiasm remained undeterred.

Cyclicals outperforming Defensives

In light of the recent rate cut, growth stocks have outperformed value stocks over the past few weeks. Small- and mid-cap stocks also benefited from the prospect of lower interest rates, outpacing their larger counterparts.

From a sector perspective, more defensive sectors like healthcare and consumer staples were among the weakest performers. Conversely, utilities fared well, benefiting from both the rate cut and increased energy demand, particularly from AI data centres. The energy sector outshone, buoyed by a strong increase in oil prices in the first week of October, with Brent crude rising to around $80 per barrel from $72 at the end of September.

The top-performing sectors are largely seen as cyclical: materials and industrials both outperformed the broader market. In addition to energy, communication services delivered strong results, while information technology also outpaced the broader market.

Approaching the Q3 earnings season

The third-quarter earnings season is about to begin, with consensus expectations revised downwards. According to FactSet Research, the estimated year-over-year earnings growth rate for the S&P 500 is around 4% (down from nearly 8% at the end of June). If realised, this would mark the fifth consecutive quarter of positive year-on-year earnings growth.

All sectors, with the exception of information technology and communication services, have seen earnings estimates revised downwards. Overall, earnings growth is expected to be driven by information technology, communication services and healthcare. Only three sectors—financials, materials and energy—are expected to post negative earnings growth.

Looking ahead, the outlook for the next 12 months appears more optimistic. Earnings are expected to increase by 14%, with information technology, communication services and healthcare leading the way once again. Not a single sector is anticipated to report a decline in earnings over the next year.

With this in mind, and considering the outlook for the next 12 months, valuations seem stretched but not excessively so. The estimated 12-month forward price-to-earnings ratio stands at 21.4, above the five- and ten-year averages.

Pre-election indecision

Since the end of July, we only hold a positive grade on healthcare (upgrade to +1 on 25 July, while downgrading technology to neutral). We have maintained that sector allocation. As the recent presidential polls continue to indicate a tight race between Kamala Harris and Donald Trump, we expect a generally neutral market environment. Our overweight position in healthcare thus remains our primary conviction, on the back of the completion of post-pandemic normalisation, realistic earnings growth expectations, the sector's defensive characteristics and ongoing innovation.

Emerging equities: Sharp rebound for China

In September, emerging markets delivered robust returns (+6.4% in USD), outperforming developed markets (+1.7%).

In US, the Fed recalibrated its rates policy and announced a first 50 bps cut in over four years. Chair Jerome Powell insisted on a balanced approach, weighing between US economic resilience and labour market weakening.

China (+23.5%) saw a sharp rebound fuelled by substantial stimulus at the end of month. An unprecedent joint press conference was held by the Chinese central bank, the Chinese SEC and other financial regulators. Supportive measures included cuts to the reserve requirement ratio, policy rate and mortgage rates. Liquidity support targeting the stock market was also announced. Investment institutions, such as funds, insurance companies and banks, will be allowed to pledge their stock holdings at the central bank in exchange for funding that can only be re-invested in equities.

India (+2.2%) saw a further rise of its weight in the benchmark, supported by resilient earnings and a healthy long-term outlook. Furthermore, India’s full-year inflation outlook was in line with the central bank’s expectations.

In Taiwan (+1.2%), exports figures reached record highs in August. This was driven by resilient demand from AI and other computing needs, as well as the recovery from delayed shipments in July. In Korea (-3.6%), expectations rose on the Bank of Korea’s possible pivot in the coming months. The government’s value-up initiative continued its course with a launch of “value-up index” covering related companies.

In LatAm, Brazil (-1.0%) entered a rate hiking cycle, but the full-year GDP outlook remained healthy. Mexico (+1.1%) saw inflation ease. Its legal system is being reviewed by the President’s ongoing judicial reform proposal.

In other markets, Southeast Asia saw some improvement, helped by the Fed’s rate policy. At the beginning of the month, Bank Indonesia cut base interest rates by 25 bps. Elsewhere, South Africa (+6.4%) also joined in with the easing, with a 25 bps cut. Turkey (-1.9%) had a successful sale of 10-year dollar bonds to support the economy.

For commodities, crude oil declined 8.9% over the month. Gold rose by 5.2% and silver by 9.5%. US yields finished the month at 3.81%.

Outlook and drivers

Emerging market equities have demonstrated a robust recovery this year, with emerging countries playing a crucial role in global economic growth.

The Fed finally unveiled an easing cycle with a 50 bps cut, beating consensus. Chair Jerome Powell also confirmed the possibility of further cuts this year. Consequently, some Asian currencies are gaining tailwinds from a weakening USD, which also offers central banks more flexibility to react.

Chinese authorities have introduced monetary and fiscal measures to combat deflation and stabilise the economy, triggering a significant market rally. While these steps are a positive start, more government intervention, particularly in consumer spending, the property market and employment, is needed for a sustained recovery. Investors are optimistic about potential structural reforms and stronger government support, though further fiscal action is expected. Chinese stocks, trading at multi-decade lows compared to US markets, have room for growth, but execution on policy will be critical. Increased exposure to the internet, financial, consumer and property sectors reflects market confidence, though US elections may pose external risks.

India is being used as a source of funding for China, but we remain confident about the prospects of the country. India continues to gain momentum through infrastructure investments, supply chain diversification and rising consumption, while Indonesia and South Africa have begun their easing cycles, adding to emerging market resilience.

In the tech sector, Taiwan and Korea, both leaders in semiconductors, are collaborating with US chipmakers. Despite short-term market volatility and also being a funding resource for China, the long-term demand for AI investments remains strong, reinforcing our positive outlook for these regions.

Aligned with our strategy, we dynamically calibrate the portfolio’s risk appetite in response to evolving market dynamics, when maintaining a balanced position. We are monitoring US policy, as well as China’s potential economic recovery, fundamental factors in emerging market outperformance.

Positioning update

We are optimistic on the recovery of EM equities in 2024. The Fed annouced a 50 bps cut, which is encouraging.

The Chinese government’s new stimulus is sizable and well coordinated, but futher re-rating requires solid support on the fiscal side.

No change to our sector views. We are positive on the tech sector due to resilient demand.

Regional views:

No change to our regional views

China Neutral – China’s stimulus came rapidly and on a large scale, making it the best performing country globally in a short period. However, serious profit taking has already started. Further re-rating depends on the government’s decisiveness regarding fiscal support. Geopolitical pressure lingers with the US elections.

Sector and Industry views:

No change to sector views

We remain OW in Tech / AI in the long term. We have reduced our exposure to the sector on the back of near-term volalities.