There was no lack of market events during September to cool off investors’ enthusiasm for being long risk. The risk posed by Evergrande, one of the most levered companies in the world, is real but, in investors’ minds, inflation seems to be contained locally and under control. Inflation across most developed economies remains robust. Although many consider it to be a temporary result of supply being unable to satisfy strong consumer demand, it is perceived as a real threat to economic growth as it might get out of control.

Most equity markets were down for the month, declining by mid-single returns. The S&P 500 had its first negative month since the start of the year. Japan and Norway equity markets were among the few positive exceptions. Cyclicals clearly outperformed the pricier market segments but energy companies were the only direct beneficiaries of strong rising energy prices.

Developed markets’ sovereign yield curves went up, with 10-year maturity yields rising between 20bps and 40bps, and adjusting to inflation expectations and diminished central bank liquidity injections. Investment grade and high yield credit spreads were unchanged over the period.

The supply-demand imbalance at the energy level led to a strong increase in futures for Nat Gas and Coal, with serious negative consequences for industrial companies.

The HFRX Global Hedge Fund EUR returned -0.44% during the month.

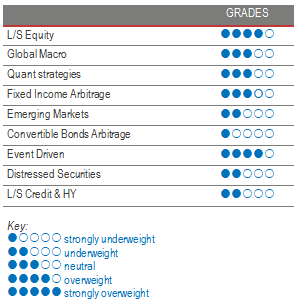

Long-Short Equity

On average, Long-Short Equity funds’ absolute performance was negative during the month. Directional strategies and managers with a growth bias weighed negatively on the sector. Energy thematic funds, low net strategies and managers with a value bias outperformed their peers. On a relative basis, the results were more encouraging for the strategy since, on average, it was slightly negative for the month (less than one percent), offering a good downside capture ratio versus equity indices. Since the start of the year, alpha generation has been challenging for Long-Short managers due to the underperformance of the short book. To minimize this negative impact, managers have reduced short books and replaced single shorts by indices. Equity markets have enjoyed a long recovery period since March 2020 and are considered by most analysts as fairly valued if not pricey. Going forward, we think Long-Short Equity funds are well positioned to benefit from both their long and short books offering an interesting risk-reward ratio. They will also benefit from increased intra-sector dispersion and try to capture, with their short books, the excesses of liquidity flowing into the markets, and particularly dislocations in work-from-home beneficiaries.

Global Macro

Market action in September led to some dispersion in returns across Global Macro managers. Discretionary managers have on average outperformed systematic strategies, benefiting from a better market read and putting to profit tactical positions in a rapidly evolving economic scenario. Long positions in the energy complex and short positions in sovereign rates were the main profit-drivers for the month. While Global Macro funds can suffer at times from a noisy market environment, we believe they could be an interesting investment opportunity to capture asset repricing moves if a persistent upward inflation market were to materialize. We continue to favour discretionary opportunistic managers who can draw on their analytical skills and experience to generate profits from selective opportunities worldwide.

Quant strategies

On average, September was a positive month for quantitative strategies. Trend-following models benefited from moves on currencies and commodities but these were negatively balanced by positions on rates and equities. Multi-strategies were up, on average, low single-digits for the month, as they continued to build a strong year-to-date performance. Equity statistical arbitrage, one of the year’s best-performing models, was slightly down for the month.

Fixed Income Arbitrage

Since the unwinding of the steepening trade on the US yield curve, the slope has stayed more or less unchanged while the bond rally took a pause. In the relative value space, swap spreads were quite stable as were the basis minimizing opportunities for fixed income RV. Nonetheless, we expect volatility to come back, especially if inflation fears ultimately materialize.

Emerging markets

The repositioning of the investment community around the reflation trade generated short-term volatility on cyclical commodities and Emerging Market currencies, which were also affected by the move on the US yield curve. Emerging Markets will be natural beneficiaries of a continuation of the world’s economic recovery. However, there are important moving pieces such as COVID-19 infection levels and the resilience of world economic growth that will probably lead to higher volatility levels. Emerging Markets, although an appealing investing ground for investors seeking decent-yielding fixed income assets, are still in a fragile situation since vaccination programmes are far behind the pace of richer nations. Although EM fundamental managers reckon the space is an interesting option in a zero-rate world, considering the fragility of fundamentals, they usually adopt a very selective approach. Caution is required, due to the higher sensitivity of the asset class to investor flows and liquidity.

Risk arbitrage – Event-driven

September was flat-to-slightly-negative for Event-Driven managers. The strategy offered very good downside protection in a risk-off environment. On a year-to-date basis, there was some performance dispersion across managers, proving that, even in a relatively benign environment for the strategy, deal-picking and sizing is important to reach return targets. Starting in June, the spread risk on Merger Arbitrage deals was re-priced, adjusting to the new reality implying higher regulatory scrutiny, specifically in the US, and to the still-high bilateral tensions between China and the Biden administration. It is common belief among the merger arbitrage investment community that, although deal completions will probably take longer to close, the market is over-pricing merger spread risk, offering an interesting double-digit annualized IRR. We therefore think that the opportunity set for the strategy remains very interesting, offering one of the best risk-adjusted returns.

Distressed

Stressed and distressed strategies continue to perform well. It is interesting to note that they remained unaffected by sector and market reversals, generating returns from idiosyncratic profitable trades and a positive risk-on sentiment. The last 15 months have been, on average, the highest performance period since the Great Financial Crisis of 2008. The COVID crisis has been a source of numerous opportunities to date, but, as the level of corporate bankruptcies is relatively low versus previous expectations, due to strong monetary and fiscal incentives, the opportunity set for the moment is more modest or limited to specific sectors. We remain attentive because, as central banks initiate tapering and rates start to rise, this strategy might become more attractive. We favour experienced and diversified strategies to avoid having to face extreme volatility swings.

Long short credit & High yield

Following the market crash at the end of the first quarter of 2020, hedge funds opportunistically loaded on IG and HY credit at very wide spreads. Managers that were able to go into offensive mode were aggressively buying on the market or making off-the-market block trades, whereas other managers, unable to meet margin calls, needed to quickly cut risk. Since then, spreads have completely reversed to pre-COVID levels. Multi-strategy managers have significantly reduced exposure to credit and high yield, as current valuations present limited expected gains and a negative risk-return asymmetry.