European equities: Still outperforming

“Uncertainty” was probably the most important driver behind the stock market’s behaviour over the past four weeks.

Growing uncertainty about the impact of the US administration’s policy agenda sent shock waves through international equity markets. European equities have continued to outperform over the past few weeks, buoyed by economic growth and increasing confidence that we will see a ceasefire between Russia and Ukraine.

Since our last committee in February, Value stocks have outperformed Growth stocks. This outperformance mainly came from large and mid-caps. This value bias has been the main driver of the recent market advance.

Among defensive sectors, consumer staples was the strongest outperformer compared to the broader European market, followed by utilities, while healthcare was broadly flat. Inversely, energy clearly lagged over the past few weeks due to a significant decline in Brent crude oil prices, towards around $69/barrel.

Within cyclical sectors, Financials was the clear outperformer, followed by Materials and Industrials, which both trended well, while Real Estate and Consumer Discretionary posted a negative performance over the period.

Finally, Information Technology was the biggest underperformer, still due to some names exposed to artificial intelligence. Conversely, Communications Services continued its positive trend.

Earnings expectations & valuations

Fundamentals remain well oriented for European equities, which continued to benefit from positive earnings revisions for 2025 in almost all sectors. Positive earnings revisions have been supportive for the European market.

12-month forward earnings are expected to grow by 7.8%. Looking ahead, consensus expects this EPS growth to be driven by Information Technology, Consumer Discretionary, Communication Services, Materials and Healthcare (with double-digit EPS growth for each). On the other hand, Utilities and Energy have the smallest EPS growth expectations, but these are now in positive territory.

Since the last committee, European valuation multiples have increased slightly, with 12-month forward P/E of 14.4x, which remains well below US multiples (22.0x). Information Technology and Industrials are the most expensive sectors (P/Es of 27.9x and 19.5x respectively), while Energy and Financials are the cheapest (P/Es of 8.3x and 10.0x respectively).

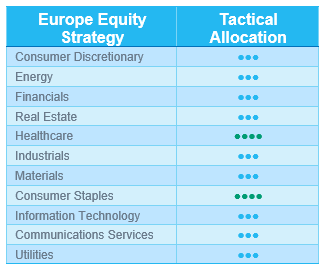

At the end of February, we tactically upgraded the Food & Beverage subsector from neutral to +1, given the strong results of food producers such as Nestlé, Danone and beer producers (AB Inbev, Heineken). Their valuations are still attractive after two years of de-rating and the subsector is significantly under-owned. There is no or little impact from tariffs (local production in the US in food and beers). Only spirits may be impacted by significant discounting and we can expect an upturn in cognac (Pernod) after a year of destocking.

During our March committee, we made the following changes:

- Consumer Staples :

We have tactically upgraded the sector from neutral to +1, given the weight of Food & Beverage (6.5%) vs. Food Retail (0.8%) and also based on Beiersdorf’s strong results in HPC. Within the sector, our preferred industries remain Food & Beverage and Household & Personal Products, as both benefit from resilient margins.

- Healthcare:

We have changed our short-term view on Healthcare Equipment & Services by bringing it back to neutral (vs +1). The subsector has benefited from some good revenues momentum and significant US dollar exposure. However, the current dollar weakness is a headwind for the subsector and valuations have become less appealing.

Finally, we have maintained a neutral grade for the other sectors, as maintaining a cautious approach continues to make sense. We also remain constructive on European semiconductors and an upgrade could occur over the next few weeks at a good entry level, as this sector should benefit from the recovery in consumer electronics in H2-25 and 2026.

US equities: uncertainty drives equity market

Uncertainty has been the key driver of equity market behaviour over the past few weeks, with concerns about Donald Trump’s policy agenda sending shock waves through international equity markets. The unclear impact of potential tariff increases on inflation, economic growth and central bank reactions led investors to reposition defensively.

Defensive large caps outperformed

After a strong start to 2025, US equities have undergone a notable correction in recent weeks due to increasing uncertainty surrounding the US administration's policy agenda and renewed concerns about economic growth.

Consequently, value stocks outperformed growth stocks, large caps outperformed small caps, and defensive sectors, such as Consumer Staples and Healthcare, significantly outperformed. More cyclical sectors such as Consumer Discretionary, Financials and Information Technology strongly underperformed the broader index.

Ongoing Q4 2024 earnings season

Meanwhile, the Q4 earnings season is heading into its final weeks. At the time of writing, almost all S&P 500 companies have released their actual results of the last quarter of 2024. Of those, 76% have reported earnings per share exceeding expectations, resulting in a blended year-over-year earnings growth of 18.3% - the highest since Q4 2021. On average, companies are exceeding earnings estimates by 7.4%, according to FactSet’s Earnings Insight report.

Looking ahead, earnings growth for the next 12 months has nevertheless been revised down to around 12%, from the previously expected 14%. Uncertainty is undoubtedly one of the main contributors to the negative earnings revisions, as an increased number of S&P 500 companies citing “tariffs” on earnings calls has increased considerably and reached record levels, according to Factset Research.

Growth expectations continue to be driven primarily by Information Technology, Healthcare and Industrials. Against this backdrop of slightly revised earnings expectations and recent weak market performance, the S&P 500's forward 12-month price-to-earnings ratio declined to 20.7, but remains above both the 5-year and 10-year averages.

Adjusting our sector allocation

Although fundamentals haven’t materially changed for now, the increased risk of a severe trade war between the US and the rest of the world, and the related growth fears, sparked a considerable decline in both the US dollar and US long-term rates. Considering this changing market environment, we decided to slightly adjust our sector allocation:

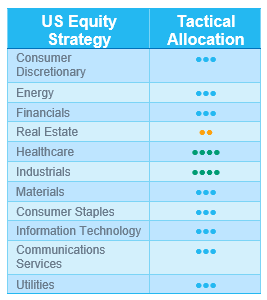

- Upgrade Consumer Staples to neutral (from -1): We recognise earnings revisions are still negative, but defensive market positioning is more important than underlying sector fundamentals. Within Consumer Staples, we have a preference for the Household & Personal products subsector, which has been upgraded to +1 (from -1). The sector has a defensive nature and contains a lot of companies with strong brands with pricing power and high consumer loyalty. The segment has an attractive valuation. Stock picking is key though.

- Downgrade Financials: The sector has performed well since we upgraded it after the US elections, as investors anticipated, among other things, looser regulations and higher long-term interest rates. For now, we don’t see any catalyst, such as deregulation or higher rates, which could lead to continued outperformance. Therefore, we decided to take some profit.

In the meantime, we have kept our +1 grade on Industrials (which continue to benefit from ongoing reshoring trends) and Healthcare unchanged (good earnings, attractive valuations, limited tariffs impact and historical 12-month performance following US presidential elections).

What about US technology?

We have been a tad more cautious on US Technology for a while now. The sector has been severely penalised during the recent market correction. Although Q4 earnings started strongly, the scale of the positive surprises was underwhelming, suggesting that earnings expectations are now more in line with reality—a notable contrast to the earlier part of last year. The market reaction to some earnings reports was surprisingly negative, even with everything AI-related continuing to see very strong end demand.

However, a significant factor in the current environment is investor positioning and profit-taking following the strong returns seen earlier. Despite falling long-term interest rates and good earnings, these factors are currently not providing enough support. Valuations have become more attractive for many companies in the technology sector. However, we remain on standby—waiting for a catalyst to upgrade the sector’s rating to +1.

Emerging equities: standout performance from China

Emerging markets booked the month at +0.4% (in USD), and outperformed developed markets (-0.8%), which were dragged down by a declining US market (-1.7%).

In US, the postponement of the 25% tariffs on Mexico and Canada fuelled a market rally at the beginning of the month. However, incremental tariff threats toward China and other countries reversed the trend by month-end. The Trump administration’s policy path remained highly uncertain.

China (+11.7%) was the standout performer in February, driven by AI optimism and following renewed investor interest in tech stocks. A key catalyst was President Xi’s engagement with top tech firms, signalling an attempt to revive private-sector confidence.

India (-8.1%) underperformed, weighed down by foreign investor outflows, tariff concerns and signs of slowing domestic growth. Latin America (-0.8%) saw mixed performances across the region, while Poland (+7.7%) gained on rising expectations of a potential Russia-Ukraine ceasefire.

In terms of commodities, crude oil fell by 4.7%, while gold (+1.9%) and copper (+5.5%) gained. US yields finished the month at 4.2%.

Outlook and drivers

As 2025 unfolds, geopolitics remains a pivotal force shaping emerging markets and the broader global landscape. The Trump administration’s shifting stance introduces fresh uncertainties, leading to increased market volatility. The potential scope and impact of new tariffs remain unpredictable, particularly for emerging markets economies with significant export exposure. Meanwhile, growing anticipation of a Russia-Ukraine ceasefire is influencing sentiment, especially in emerging Europe.

The Chinese market is on an uptrend, driven by a strong re-rating in the tech sector. The government is currently holding its “Two Sessions,” the country’s highest-level political gathering. The communiqué reflects a clear emphasis on economic development, with commitments to stimulating domestic demand and prioritising investment in high-tech fields such as AI and robotics. The GDP growth target for 2025 has been set at 5%, supported by fiscal stimulus measures (including an increase in the debt ceiling from 3% to 4%) and is aligned with market expectations.

Thematically, AI continues to fuel sectoral growth in emerging markets. The rise of DeepSeek underscores that AI investment opportunities in emerging markets are proving far more expansive than initially anticipated, extending beyond infrastructure to globally competitive AI software development. Additionally, Alibaba is enhancing its own AI model, surpassing DeepSeek R1 in cost efficiency.

Amid heightened market volatility, a reactive, selective and flexible investment approach is essential. The portfolio leverages its strengths to dynamically adjust risk exposure, capitalise on macroeconomic shifts, and position itself in high-conviction structural themes for the long term.

POSITIONING UPDATE

US slowdown and weaker USD can be key drivers for EM outperformance. This is advantageous for China, yet positioning remains light. Meanwhile, we observed that EM are not totally immune to the risk-off mood on the US.

Regions

In China, the Hong Kong market resisted well. India is facing growing pressure. Eastern Europe is in a strong uptrend.

We have upgraded LatAm. Brazil is improving. Mexico has room for negotiation with the US considering their economic ties.

China’s Hong Kong market has held up well despite global sell-offs, with strong southbound flows but limited foreign participation. The rally, concentrated in tech stocks like Alibaba, has narrowed the valuation gap with US counterparts. Expansion into sectors like EVs, robotics and banking remains to be seen. The policy focus on consumption and investment is evident, though the economic impact has yet to materialise. Trade tensions may rise ahead of a potential Trump-Xi summit in June, while China is cooperating on issues like immigration, fentanyl and Ukraine.

India has been among the worst-performing markets YTD, with retail investors pulling back. While a further sell-off is possible, India may hold up better than others. Many quality stocks are down 20-30%, presenting selective opportunities, but it may be too early for an upgrade. A market reset is underway following high expectations.

Emerging Europe: the region has seen a strong re-rating, with high beta exposure to European markets. Poland, Hungary and Czechia are leading, particularly in banking.

LatAm upgraded to OW

Latin America’s story revolves around political change. Argentina’s market doubled last year on hopes of fiscal reforms under Milei. Colombia and Chile are in strong uptrends, while Brazil’s shift is still developing.

- Brazil upgraded to OW: the economy remains stable but is slowing. Inflation remains a concern, and Lula’s low popularity could drive fiscal spending, adding short-term volatility. Valuations are attractive, but with elections in 2026, timing is key. Despite short-term risks, confidence remains strong over the next 12-18 months.

- Mexico upgraded to OW: the country’s economy is closely tied to the US, with exports making up a third of GDP. Nearshoring remains a key theme. The market corrected last April after a leftist election win, but has since stabilised. Mexico is cooperating with the US on trade and border issues, making a deep economic downturn unlikely.

Sectors

Information Technology: The Technology sell-off appears to be caused by positioning rather than fundamentals. TSMC exemplifies strong demand and profitability despite concerns over US investments. Historically, stock prices peak after earnings revisions, which are still rising. AI remains a major driver, with Alibaba committing $50 billion. The correction seems more like a technical adjustment than a fundamental shift.