This year, the Christmas rally came a month earlier, and Santa Claus has moved from the North Pole to Florida. During December, some of the “Trump trade” winners gave back part of the previous month gains. Economic fundamentals remain resilient but, a stickier than expected inflation print accompanied by a hawkish Federal Reserve stance triggered a market selloff close to the Christmas holidays. Although the American exceptionalism narrative is still in play, many investors were concerned by the impact of interest rates remaining higher for longer.

US small and medium equity indices lagged generating high single-digit negative returns. At the other end of the spectrum, technology-heavy Taiwanese equities outperformed, alongside Japanese equities which benefited from a falling Yen. At a sector level, cyclical sectors such as materials, energy or industrials lagged the market partially due to investors reducing exposure to crowded thematics. Consumer discretionary stocks outperformed during the month benefiting from, among other things, healthy spending in luxury items.

Fixed income yields for sovereign issues in the US and Europe widened between 20 to 40 basis points for maturities over 5 years. Corporate spreads for investment grade and high-yield borrowers have also widened during the month but remain close to all-time lows.

The HFRX Global Hedge Fund EUR returned-0.11% over the month.

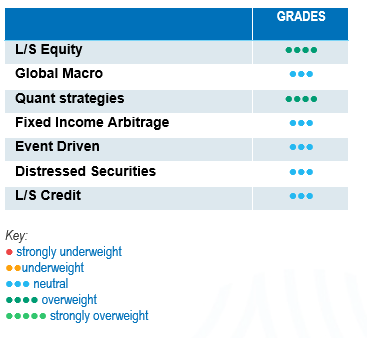

Long-Short Equity

For December, according to indices and Prime Brokers’ peer groups, average performances for Long-Short Equity strategies were negative. The outcome was magnified for managers investing in North America due to the effect of the “Trump trade” reversal. Strategies focusing on Europe and Asia managed to outperform their respective reference indices and even generate positive absolute returns. However, while Long-Short Equity managers finish the year on the tip of their toes, it was overall an excellent year for the category. On average, strategies generated a strong absolute performance benefiting from strong alpha on both sides of the book. It is true that technology stocks and AI-driven thematics remain at the centre of the stage for the equity market which can be a drag for alpha generation due to the low market breadth. While this effect hindered upside capture ratios for US focused strategies, this was less so in Europe and Asia where Long-Short Equity strategies were able to match or outperform their reference indices. The Long-Short Equity universe is very rich in terms of opportunities and diversified in terms of styles. In a world of sustained uncertainty and of diverging economic performance, Long-Short Equity strategies are well positioned to benefit from a broadening market opportunity set and increasing economic divergence.

Global Macro

Performances for Global Macro funds during the month were dispersed with a positive low single-digit average. Positive performance contributions from long dollar positions were offset by long equity investments. Full year performances for 2024 were decent, but also very dispersed. Performance drivers for the year were fairly even with positive contributions coming mainly from foreign exchange, equities and credit. Trading in rates was challenging due to the reversal of trends at the back-end of the curve. An average fairly diversified Global Macro strategy has provided for the year a positive return ranging from mid to high single-digit figures. This is well below a 50% upside capture ratio versus world equities but can be explained by cautious capital risk deployments in a very uncertain environment and an underweight positioning to large cap technology stocks. Currently, the economic decoupling across the major economic regional powerhouses offers interesting investment opportunities for Global Macro managers.

Quant strategies

December was strong for Quantitative strategies. Multi-Strategy Quantitative models outperformed once again Trend Followers, but on average, both strategies added value to portfolios generating positive mid-single-digit returns. Gains made by Trend Following models in foreign exchange were negatively balanced by fixed income, equities and commodities during the month. Full year performances for Trend Followers have been modest with gains driven mainly by foreign exchange trading. Fixed income positions were the main performance detractors. Blue Chip Multi-Strategy Quant models did well generating double-digit positive returns for the year. Equity statistical arbitrage models were among the biggest performance contributors.

Fixed Income Arbitrage

After months of uncertainty surrounding inflation persistence and economic strength, central banks have moved toward a more dovish stance, acknowledging the need for rate cuts as inflation normalises downward. While the extent of these rate cuts is yet to be determined, this shift has created a variety of opportunities, with market movements differing significantly across regions. In the US, the bond market has trended higher, and the yield curve has steepened, as the number of rate cuts to be implemented remains highly dependent on inflation data. Meanwhile, the spreads between the 10-year European bond yield and both the US and UK 10-year yields have reached historically high levels, as ECB faces a very different economic environment: inflation trending down & economic slowdown. In Japan, the end of ultra-loose monetary policy offers both relative value (RV) and directional opportunities. This environment has been very supportive for the fixed-income space, both in terms of relative value and directional strategies, although some directional managers have faced challenges.

Risk arbitrage – Event-driven

Event-Driven strategy indices were modestly positive to end the year. Merger Arbitrage strategies benefited from the successful completion of a few deals such as the acquisition of Catalent by Novo Nordisk and an improved market sentiment towards the opportunity set going forward. However, 2024 was another year of disappointing returns, strong dispersion across the universe and performance generation below expectations. Strategies focusing on Special Situations have outperformed during the month and since the start of the year. Good strategies were able to benefit from idiosyncratic situations. The opportunity set for Merger Arbitrage during 2025 is expected to improve with a much more business-friendly Administration. However, deal selection will remain an important focus of attention. The confrontational style of the new US president might be a source of concern for cross-border deals.

Another source of concern for increasing the number of deals announced is the stability of the interest rate trajectory.

Distressed

Default rates have started to tick upwards recently but, overall, defaults remain concentrated in specific sectors such as office real estate or logistics companies that levered up during the COVID crisis to meet rising demand in e-commerce. Most corporations were able to refinance opportunistically their outstanding debt at lower rates during the 2020-2021 period. Distressed specialists remain focused on idiosyncratic opportunities, remain cautious about high-yield issues as spreads are close to all-time lows and have identified cracks in specific areas of the loan market. Stressed debt strategies were able to source interesting opportunities in balance sheet restructuring and liquidity provision to specific market participants.

Long short credit

Base interest rates remain wide offering to investors in credit decent yields. However, corporate spreads are close to all-time lows. One can wonder if investors are being appropriately remunerated for the risk taken. Managers have concentrated their portfolio into their highest fundamental convictions, increased the level of hedges and lowered strategy directionality. On the other side, such a rich market generates numerous opportunities for alpha shorts. Although rates are initiating a cut cycle, they remain at high levels which favours alpha generation both on long and short positions as fundamental research becomes more important in portfolio construction. Absolute return or hedged investment approaches have gained more relevance with the increase of idiosyncratic risks and geopolitical uncertainty. Risk diversification is important and should be an integral part of the investment allocation process.