Last Week in a Nutshell

- The US job report for December confirmed the path towards full employment as the unemployment rate fell another 30bp to 3.9% and wages remained elevated at 4.7% YoY.

- Bond yields rose sharply as the minutes of the last FOMC sent a clear signal in the Fed’s readiness to dial back its balance sheet expansion. The Fed already surprised investors mid-December by pencilling in 3 hikes in its funds rate.

- In the euro zone’s December PMI, services showed the softest expansion in 8 months, mainly due to the spreading of the Omicron variant. Manufacturing activity expanded despite supply-related disruptions.

- Euro zone preliminary inflation data for December showed an all-time high of 5.0% YoY, likely marking the peak. A sharp decline in early 2022 is largely mechanical due to base effects.

What's Next?

- Inflation will remain the focus as the US and China will release inflation-related data. In the US, they may set new highs in this cycle, as seasonal rising demand and supply constraints had an impact.

- Inflation and monetary policy will further be scrutinized, as the nomination hearings for Fed Chair Powell’s second term and Governor Brainard’s nomination as Vice Chair will take place in the US Senate.

- The University of Michigan will release preliminary data on consumer sentiment, helping investors assess how consumers view their own and the economy’s prospects.

- On the geopolitical front, various meetings on Ukraine between the US, NATO allies and Russia will gain attention. In addition, clashes in Kazakhstan, sparked by a sharp increase in fuel prices, might be on the agenda.

Investment Convictions

Core scenario

- We continue to see upside and downside risks for risky assets, sparking volatility, but we are overall constructive for 2022.

- Our central scenario is that the economic recovery will continue, far from being at the end of the cycle (GDP +3.9% in the US and +4.3% in the euro zone in 2022, +4.9% in China). “TINA” will likely continue to prevail in the months to come and support equities.

- Beyond concerns about the Omicron variant, we believe that the medium-term context remains positive for equities, value stocks and assets and short duration on fixed income.

Risks

- First and foremost, the coronavirus infections, due to the Omicron variant, and lower temperatures in the northern hemisphere underline the risk of a stop-and-go in economic restrictions.

- Second, supply side constraints are numerous and will last longer than expected. A situation of extreme supply tension could also eventually impact not only economic growth but also corporate earnings’ growth.

- Third, a brutal, faster-than-anticipated rate tightening in US financial conditions - if inflationary pressures increase and/or persist - could jeopardize the recovery

Recent actions in the asset allocation strategy

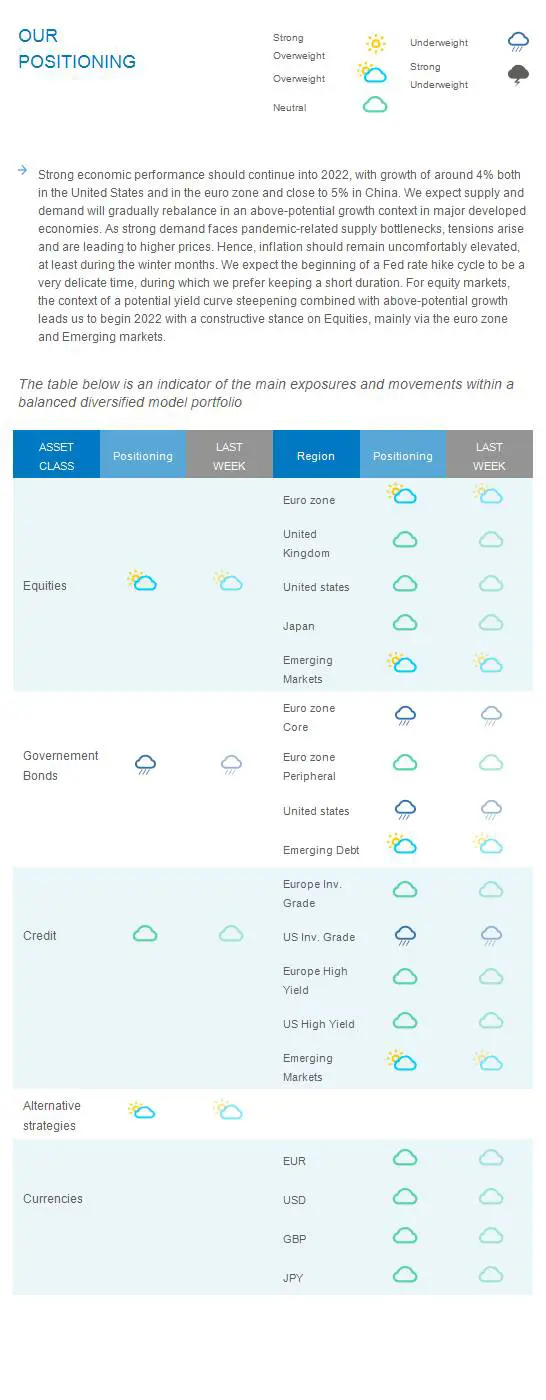

Strong economic performance should continue into 2022, with growth of around 4% both in the United States and in the euro zone and close to 5% in China. We expect supply and demand will gradually rebalance in an above-potential growth context in major developed economies. As strong demand faces pandemic-related supply bottlenecks, tensions arise and are leading to higher prices. Hence, inflation should remain uncomfortably elevated, at least during the winter months. We expect the beginning of a Fed rate hike cycle to be a very delicate time, during which we prefer keeping a short duration. For equity markets, the context of a potential yield curve steepening combined with above-potential growth leads us to begin 2022 with a constructive stance on Equities, mainly via the euro zone and Emerging markets.

Cross asset strategy

The shifts in economic and inflationary regimes will call for a dynamic equity allocation. As we enter Q1 2022, inflation should peak and bottlenecks start to ease. We will focus on value and risky assets until growth shows resilience and inflation decelerates. We recently increased our exposure to equities.

- We have exposure to assets related to the post-COVID rebound/recovery

Overweight equities, underweight bonds. Within equities, preference for European and Emerging Markets through China-A onshore stocks, then Japanese and US equities.

Underweight government bonds, keeping a short duration. We focus on the source of the highest carry, i.e. emerging debt. We stay neutral European investment grade credit, we downgrade US investment grade. We have a currency exposure to the NOK. - Positive stance on financials, materials and energy – assuming that Q1 2022 sees inflation peaking and bottlenecks easing.

- In our core long-term thematics: tech&innovation, healthcare and climate, as they reveal high growth potential.