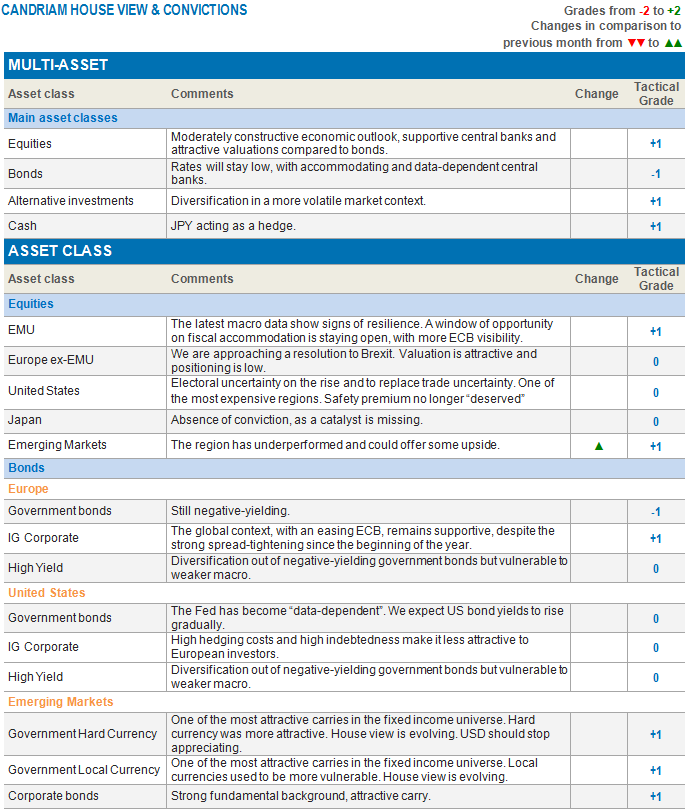

We enter 2020 as the US and China have just signed a partial trade deal. What a difference a year makes!? The trade war that raged through 2019 bringing emerging markets equities down and geopolitical tensions up is finally taking a backseat to electoral uncertainty in the US. Elections that are going to be unique for a lot of reasons. Let’s see how Candriam is preparing for the year ahead and the latest changes to our cross-asset strategy.

Equities vs. bonds

We are just leaving 2019 behind. It was a very special year as all asset classes performed positively, the exact opposite of what happened in 2018. US equities finished first, followed by euro zone equities, oil, emerging markets equities, gold and emerging market debt just to name a few. The 2019 optimal combination of asset classes reflects the past need 1) to be invested in the safer US region, protected by the Trump put and the Fed put throughout the year, 2) to diversify out of low-yielding government bonds and 3) the necessity to hedge in case of severe market corrections via precious metals, such as gold.

Today, based on our fundamental, quantitative, technical analyses and our expected returns, our central economic scenario is a mildly optimistic scenario with positive - yet more modest - expected returns.

Our preference still goes to equities over bonds and we are comfortable with a slight overweight.

Equities still have room to grow. They still have potential to exploit. There is no euphoria. There is no excess optimism among investors. So where to go? Where do valuation and equity risk premium offer the most potential to investors?

Equities

US: from trade to electoral uncertainty

The country is facing an extremely polarized election year. The 2020 election is on track to be one of the most divisive and contested in the US history. The Republicans and the progressive Democrats, such as Warren and Sanders, are at opposite of the spectrum on 8 major topics, including corporate/personal taxes, regulation, trade, energy, health, finance and technology. Enough to trigger volatility and sectorial rotations.

Our positioning on US equities is currently neutral. The region has become the most expensive and while they deserved the safety premium in 2019, the elections will reshuffle the cards in a lot of areas.

The Iowa Democratic caucuses will take place early February (3/02/2020). It will be the first nominating contest in the Democratic Party presidential primaries for the 2020 presidential election.

Meanwhile the trade war has expectedly taken a backseat. Trade deal phase 1 has been successfully negotiated and signed mid-month. Phase 2 is said to start immediately but US President Trump has already managed the market’s expectations: a deal will likely not be signed before the presidential election on November 3rd.

The absence of further escalation should give breathing space to corporates and benefit equity markets outside of the US and that is one of the keys to our current allocation.

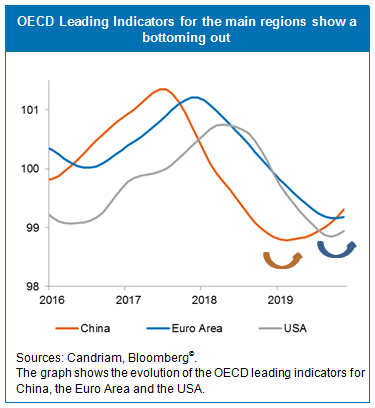

Europe: better news flow consistent with the bottoming out

In Europe, like in the US and China, manufacturing PMIs are still contracting but some leading indicators confirm that the lowest point may be behind us. The bottoming out is also consistent with the improving news flow, witness the improving economic surprises.

Valuation for both the euro zone and the UK are in line - or below historical levels.

Our positioning is overweight euro zone equities and we have let the overweight drift higher without much concern. The region finally benefit from the lower perceived political risk as a hard Brexit is barely an option now. Some good news has already been priced in. Much more upside will be conditioned by tangible signs of improving growth level in the GDP and earnings growth for instance but for now, it is enough to justify our stance.

We stay neutral UK equities. We had stayed underweight for a long period between the referendum on Brexit and Q3 2019 when a Brexit deal seemed increasingly likely. We now mark a pause. The UK is an attractive region in terms of equities investment:

- the relative valuations discount is appealing

- investors are currently under-allocated

- some short-term volatility in the currency and UK assets is likely but on a medium-term perspective, a lower GBP and a struggling equity market should not persist

Mark Carney, the current Governor of the Bank of England, leaves at the end of January 2020. The odds of an interest cut while he is still in office are increasingly high (next decision will be known on 30 January). Besides a looser monetary policy, some fiscal easing later this year could act as performance trigger.

Emerging markets: a better start

Emerging markets are off to a better start this year than last year. The trade war should dwindle down and have less impact. Leading indicators also show a bottoming out in the cycle.

China recently reiterated that the country would implement proactive fiscal policy, prudent monetary policy and prioritize employment. They have proven their ability to support their economic growth in 2019 and have the means to keep it up in 2020.

The equities valuation is relatively attractive and emerging markets should outperform developed markets in terms of EPS growth.

For all those reasons, our positioning has recently become overweight emerging markets equities.

Bonds and currencies

Our underweight government bonds persist as we start a new year. Rates are low and shall remain low even if recession fears fade. Since the crisis, we are in a new world of lower growth expectations and lower inflation. In spite of this, the equity risk premium is now back to a top level, making equities more attractive than bonds.

We are overweight emerging markets debt, as it brings one of the highest carry in the fixed income universe.

We remain invested in investment grade bonds, especially emitted by EUR companies. The global context, with an easing ECB, remains supportive, despite the strong spread-tightening since the beginning of the year.

In the currency universe, we remain long Yen as a hedge.

We have exposure to gold, which remains an attractive hedge in a context of negative to low rates.